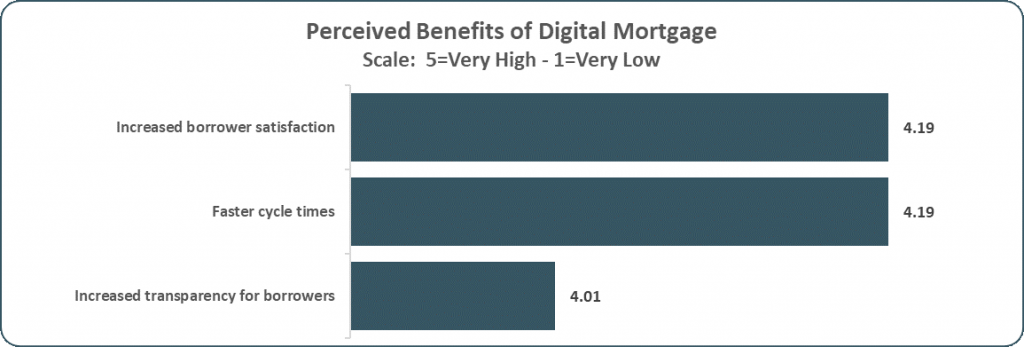

STRATMOR has just completed the Digital Innovations section of the 2019 Technology Insight® Study and for the third year in a row, lenders perceive “increased borrower satisfaction” as the top benefit of pursuing digital advancement with their loan processes. In fact, each of the top three benefits are tied to the borrower experience:

This is good news. The study data means that most lenders understand that the primary focus of digital technology is to provide a truly delightful borrower experience and that taking a customer-centric approach to lending drives revenue growth. But with this good news comes a question: why aren’t technology advancements happening faster?”

One possible reason is that the pursuit of borrower satisfaction is difficult to model as a revenue driver, making it difficult to justify as a budget expenditure. Lenders know its value but have a hard time writing checks for new, advanced technology.

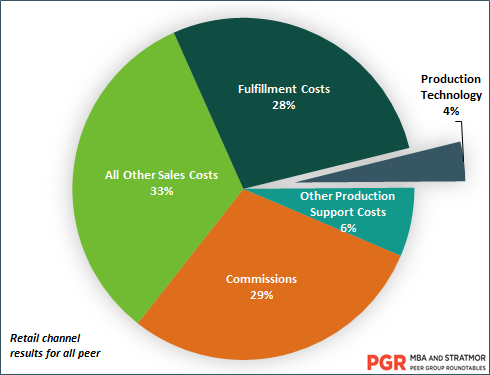

A recent Insights Report article “Creating a Best-in-Breed Technology Suite,” reported that technology costs currently represent just four percent of overall loan costs. As shown in the chart below, technology costs are a very small piece of the pie compared to originator compensation (29 percent) and fulfillment costs (28 percent). In other words, lenders should be investing more on technology to drive customer delight, and in turn create more repeat and referral business.

Ten years ago, if you wanted a cup of coffee at Starbucks you drove to one of their cafés and either went in and ordered or went through the drive-through lane. Their digital innovation — a phone app — has changed this customer’s behavior. While I can still walk in or drive into a café, I now order my drink on the app, just the way I want it, trusting that the order I place will be correct and ready when I go to pick it up. The technology gives me more control of the process and Starbucks has adapted their process to create a satisfied customer who returns to them regularly.

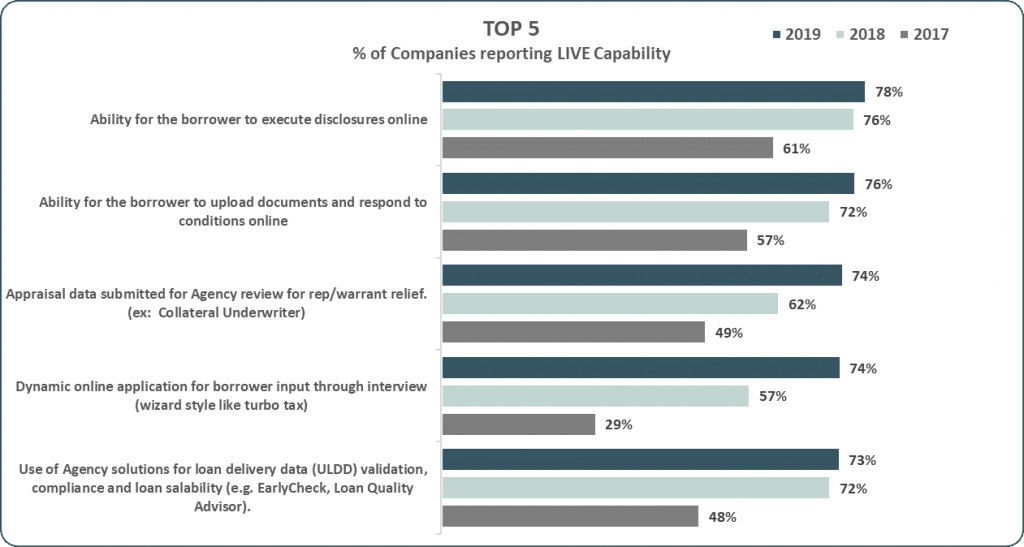

In recent years, the mortgage industry has been taking steps in this same direction, not only modernizing technology offerings but doing so in a way that empowers borrowers. The chart below from STRATMOR’s 2019 Technology Insight® Study show lenders’ digital capabilities in use from 2017 to present:

Borrower-centric offerings — online disclosures, online upload of documents and response to conditions, offering a dynamic online application—are in the Top 5 capabilities. Additionally, more than 70 percent of lenders report some level of live digital capabilities.

One of the most noteworthy changes that truly reflects a borrower-centric response is in the capability of dynamic online application — in 2017 less than 30 percent of lenders offered it. Today, 74 percent do — this is a capability that lenders adopt because the borrower wants and expects it. What a leap in just two years!

The move to offering an online application is paying off for lenders, who are seeing improved borrower behavior scores on post-close surveys. One MortgageSAT client who implemented a dynamic online application in late 2018 saw the following score increases in a before-and-after analysis:

Wow! This is a big jump in the Net Promoter Score and a great way to justify additional technology spend toward improving the borrower experience. The uptick in NPS means that more borrowers are now willing to recommend based on their experience. Also, noteworthy, these digital capabilities are activities that require the borrower to do work vs. the lender’s staff, activities like borrowers executing online disclosures instead of the lender opening mail packages and entering info into the system. Or, having the borrower upload documents instead of sending in the documents to a processor to organize and upload.

While these are time and cost savings steps for the lender, these capabilities benefit the borrower, too, by providing an empowering experience that puts greater control of the loan process into the borrower’s hands — and the borrower likes and wants this.

In addition to empowering borrowers with customer-facing technology, lenders should also consider measuring the sensitive points in each borrower’s loan journey that end up making or breaking their delightful experience, and thus their willingness to refer business. STRATMOR’s MortgageSAT program measures the borrower process from application through closing for more than 100,000 borrowers annually and specifically keys in on missteps on certain loan processes. These loan processes, which we call the Seven Commandments of Achieving Borrower Satisfaction, directly impact the Net Promoter Score (NPS), which indicates a borrower’s willingness to recommend a lender to friends and family.

According to data from MortgageSAT, technological improvements can have a major impact on Net Promoter Scores, which measure the likelihood of customers to recommend and are therefore a reliable representation of potential future revenue. For example, a 30-point change in NPS for a company doing 8,000 loans annually (with a Net Production Margin of $1574 per loan) is worth approximately $1.8 million to the bottom line. Technology improvements — like the addition of an online application — hold the potential for big leaps in future revenue. (For more calculations like this, visit the MortgageSAT webpage.)

Digital technology has changed the mortgage business for lenders and borrowers alike. Here are three suggestions for putting digital capabilities to work for you and your customers:

Find out more about STRATMOR Group’s CX services and how transparency into the loan process can help your company. Contact Mike Seminari at mike.seminari@stratmorgroup.com.

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.