Did you know that goats have rectangular pupils, which give them 340-degree vision? Or that they don’t like stepping into or standing in water? Or that they sneeze to communicate with each other? OK, before we get started here, I need to clarify that I’m not hanging up my career in this industry in favor of becoming the shepherdess of a herd of goats. But when I recently tested out an Agentic AI voice agent and it asked the reason I wanted a cash-out refinance… for some odd reason, I spontaneously told the AI agent I wanted to buy a herd of goats. (Welcome to the weird mind of Sue Woodard.)

But honestly, I couldn’t wait to hear how it responded. Crazy enough — it responded perfectly. It literally said that goats sounded like an interesting project, and how many goats did I want to obtain for my herd? I was blown away. And I’ve heard the same AI agents successfully blow through objections that would stop most MLOs in their tracks. Not to mention they are available 24/7, never take vacation, and have exactly zero problems with their coworkers or managers. If you think the AI experience can’t possibly compete… think again.

Let’s start with a reality check. We all know that AI adoption is no longer a future-state conversation for the mortgage industry — it is happening right now, across every generation of borrower, every tier of competitor, and every corner of our business operations. The question lenders and technology vendors need to answer now is not whether to embrace AI, but how to do it in a way that amplifies what makes mortgage professionals irreplaceable: the human connection.

Research shows that over 60% of U.S. adults between the ages of 18 and 79 are already using AI in some form, and 20% have made it a daily habit. Perhaps more striking for our industry: Realtor.com data shows that 61.9% of homebuyers consider AI a “positive use of time” in their home search, ranking it second only to their real estate agents.

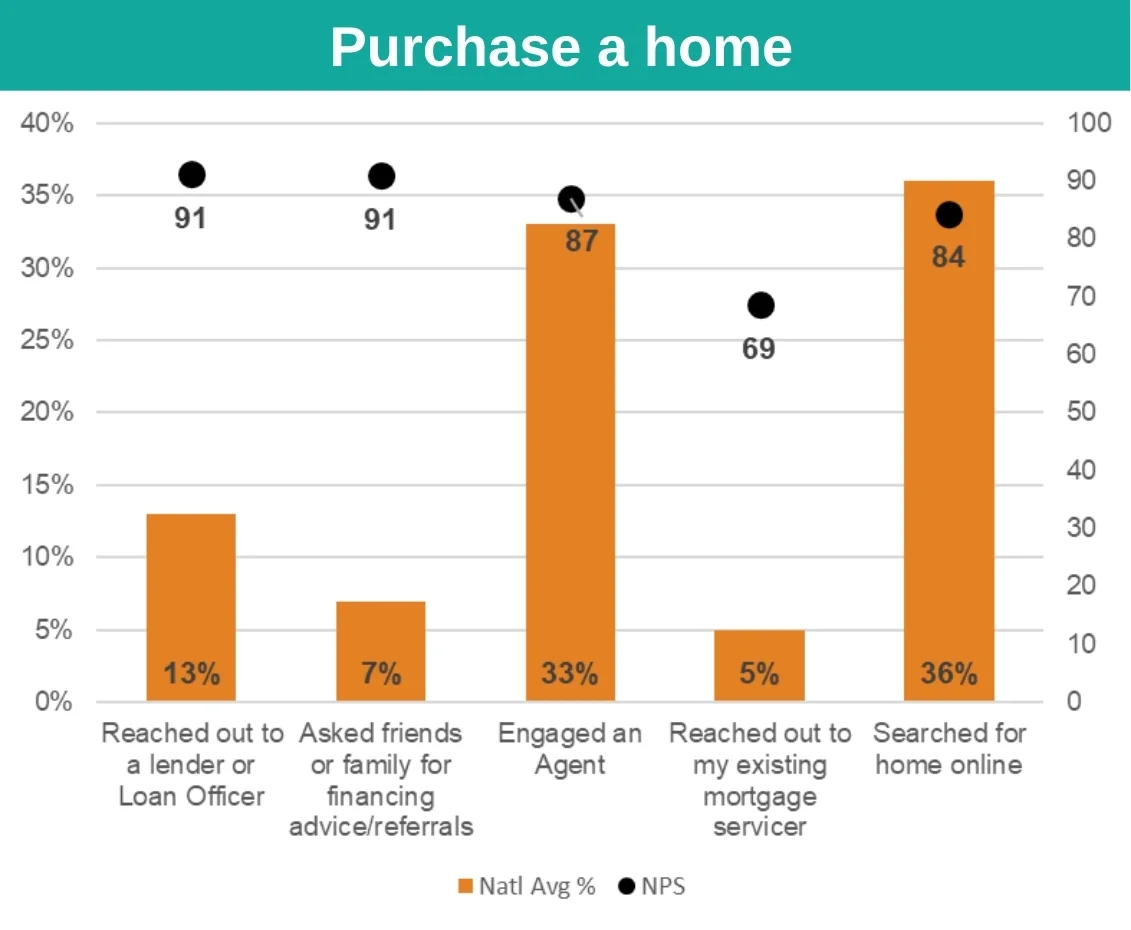

STRATMOR’s MortgageCX data further confirms this, revealing that 36% of borrowers say their first course of action when looking to purchase a new home is to search for a home online, where open AI-driven interfaces are helping prospective borrowers gather more information than ever before they even think about contacting a live human. Your borrowers are not waiting for you to catch up to them. They are already there.

Source: STRATMOR Group 2025 MortgageCX Survey Results

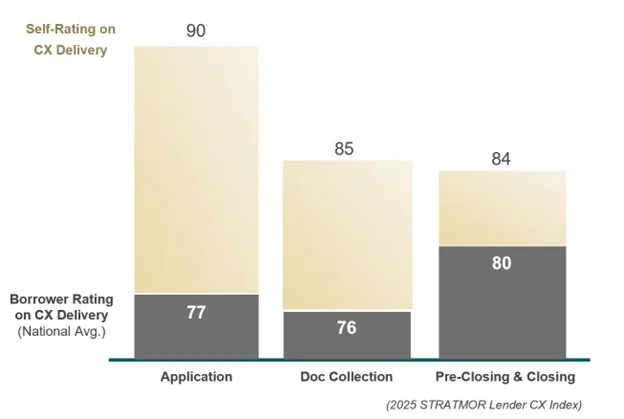

At the same time, there is up to a 23-point NPS gap between what executives believe about customer loyalty and what customers actually report, according to STRATMOR’s 2025 research. Executives overwhelmingly believe their customers are more loyal than ever. Customers tell a very different story. STRATMOR Director of Customer Experience Mike Seminari refers to this as the “CX Perception Gap.”

Adding to this, STRATMOR’s MortgageCX data shows that despite lenders seeing high satisfaction scores, many borrowers still don’t refer or return. In fact, while most companies believe they are customer-obsessed, only a small fraction of customers agree. In a market as competitive as mortgage, loyalty cannot be assumed. It must be earned, repeatedly, through meaningful human engagement enhanced by intelligent technology.

“Fads fade and cycle, but the human desire to be taken care of never goes away.”

— Will Guidara, “Unreasonable Hospitality”

That insight from hospitality leader Will Guidara captures the thesis of what I call the New Mortgage Dream Team: not AI totally replacing humans, but AI and humans working together, each doing what they do best. The technology handles scale, speed, and data intelligence. The human brings judgment, empathy, and the trusted relationships that actually close loans and generate referrals. Getting this balance right is the defining strategic challenge today for mortgage lenders.

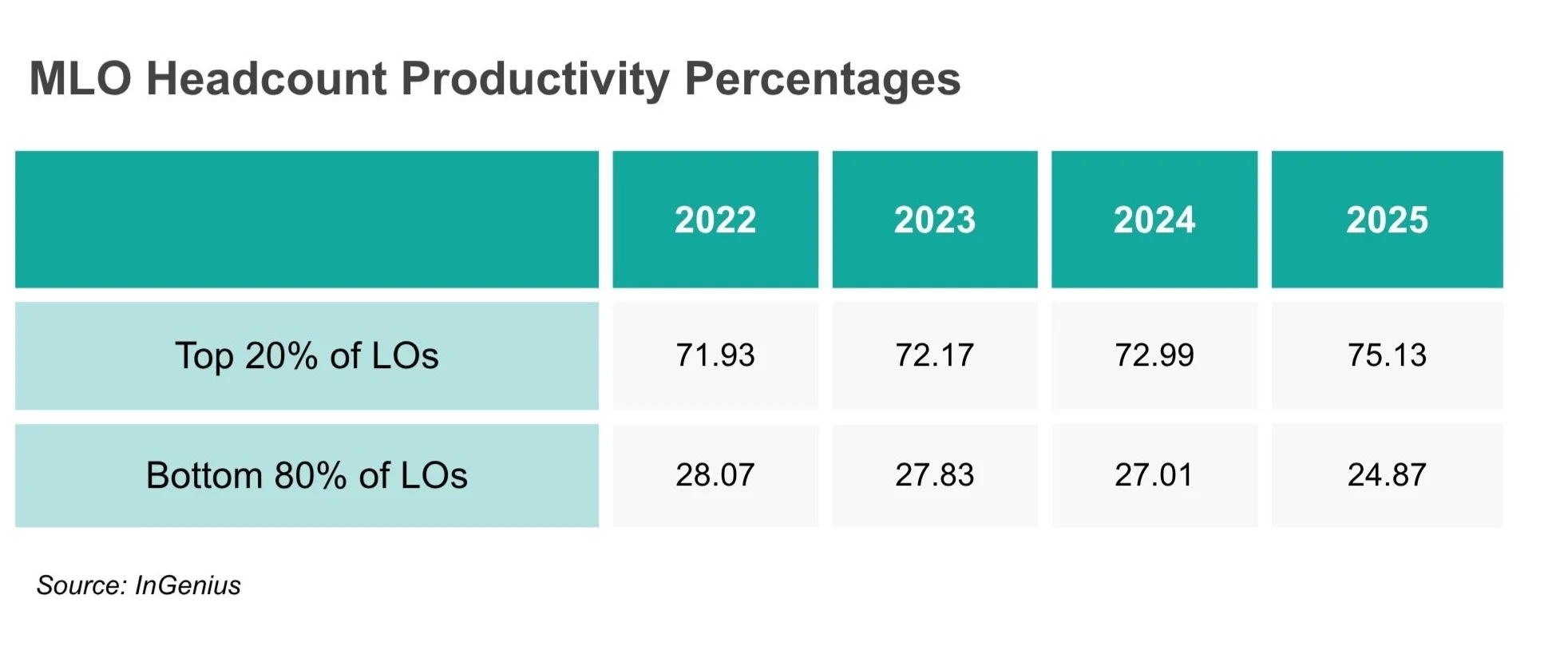

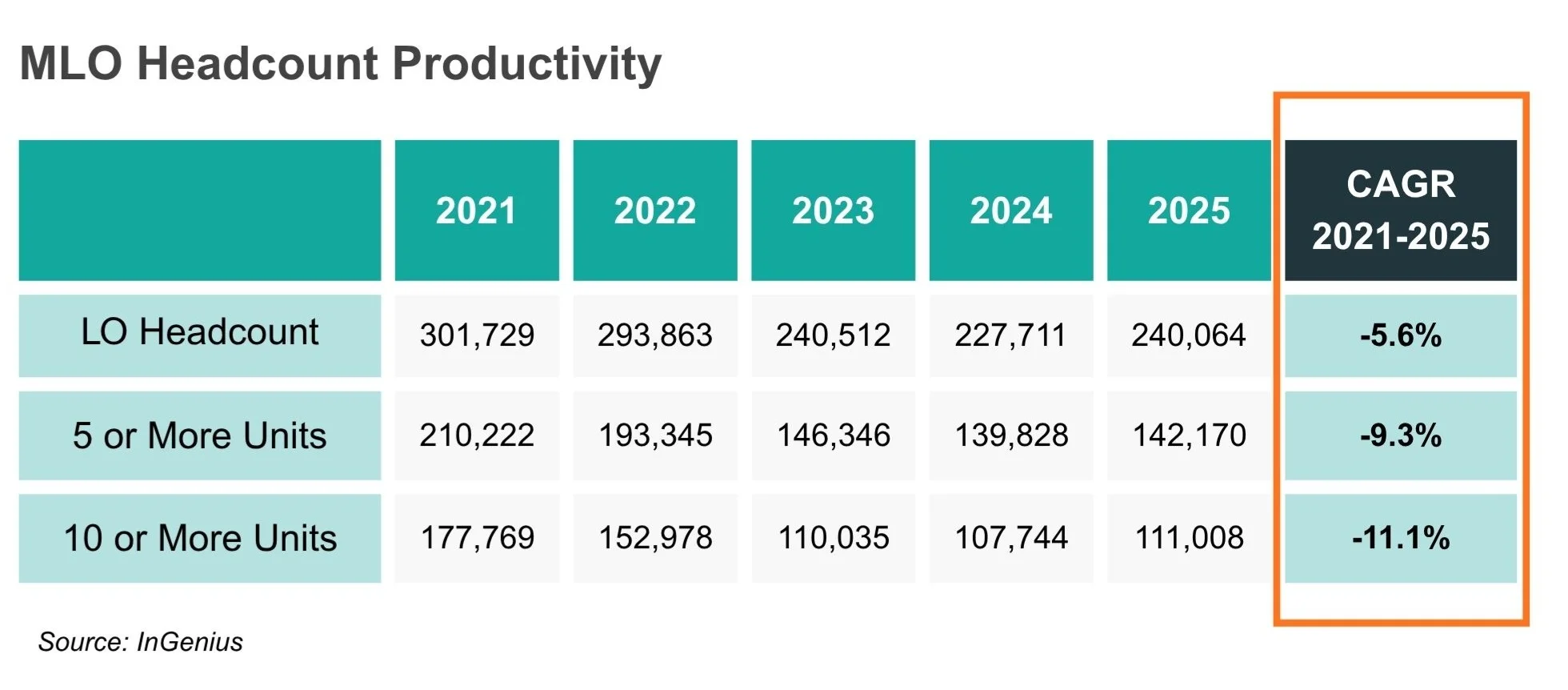

Consider what is happening at the workforce level. MLO headcount has declined from a peak of more than 300,000 in 2021 to approximately 240,000 in 2025 (counting all active MLOs, regardless of production). But more telling is the productivity data: the top 20% of loan officers consistently close more than 70% of the volume. And the gap between high performers and everyone else is not narrowing — it’s widening.

Meanwhile, the age gap between mortgage professionals and the buyers they serve is growing, with more than a decade separating the two in many cases. The average first-time homebuyer today is 32 years old, and the top 20% of loan officers’ average age is well above 50. These are not just demographic statistics. They represent a real and widening gap in communication style, technology expectations, and pace of interaction. Your first time borrowers grew up with smartphones. They expect digital responsiveness, not business-hours-only availability. AI can bridge that gap, but only if it is deployed thoughtfully and paired with genuine human expertise.

Based on current market research, conversations with leading lenders, and STRATMOR’s ongoing advisory work across the industry, here are five actionable best practices for lenders and technology vendors building out their AI capabilities.

AI implementation that happens to people rather than with people will fail. Before rolling out any AI tool, assemble a cross-functional task force that includes representatives from every major team: operations, sales, compliance, marketing, and technology. Appoint a lead champion, but ensure the group broadly represents your organization.

This team serves two critical functions. First, they become internal champions who can translate AI’s capabilities into language their colleagues understand, reducing the anxiety that inevitably accompanies any significant technology change. Second, they serve as your “human in the loop,” the oversight layer that tests AI outputs, flags hallucinations, catches compliance risks, and evaluates whether the actual customer experience matches the intended one.

One pitfall to avoid: handing AI governance entirely to your technology team or getting so caught up in rules that you slow progress to a crawl. We believe strongly that governance matters, but it’s important to remember the consumer isn’t operating under the same constraints.

While you’re debating policies, your borrower may already be running a pricing scenario through ChatGPT for a second opinion or turning to Claude or Microsoft Copilot for guidance on their next loan.

AI isn’t just a technology issue. It’s a business transformation that touches every function. The people most affected by it need a seat at the table from day one, and that includes recognizing that consumers may adopt these tools far faster than you expect.

The temptation in any AI initiative is to try to do everything at once. Resist it. Instead, identify the two or three use cases that will deliver immediate, measurable impact for your team and your customers — with the lowest regulatory and operational risk.

High-value, lower-risk starting points include:

The unifying principle: AI should handle the repetitive, high-volume and high-velocity tasks that consume your team members time, so they can focus on the high-value human activities — building relationships, providing financial guidance, and converting warm opportunities into closed loans.

AI is only as good as the data it runs on. If your CRM is incomplete, your systems are siloed, or your contact records are riddled with gaps, any AI layer you add on top could amplify those problems rather than solve them.

Before investing in AI solutions, conduct an honest assessment of your data infrastructure.

The industry production data is also instructive here. By all counts, there are still currently somewhere around 240,000 licensed loan officers, but less than half of that population closed 10 or more units during all of 2025. That gap represents an enormous population of underperforming producers, and, for many lenders, it is a significant blind spot — or an opportunity. AI-driven analytics can illuminate those gaps and help managers coach to them. AI tools can help more of those underperforming loan officers become more productive. Or frankly, AI solutions may help managers make difficult, but data-informed and necessary staffing changes.

There’s no doubt that the pace of AI innovation and transformation is moving extremely fast — and getting ever faster. Perplexity AI CEO Aravind Srinivas told a group at Harvard Business School that his longest-range plans are only 90 days out, because with AI moving so quickly, it’s simply pointless to do longer term planning. Wow.

And sure, humans are adapting technology faster than back in the day. It took the telephone 50 years to reach half of American households, whereas ChatGPT reached 100 million users in just 60 days. But still, we mere mortals are not going to be able to keep up with the pace of AI, and that gap is where most AI initiatives stall.

Effective AI change management requires addressing three distinct audiences simultaneously.

The age dynamics noted earlier matter here, too. A 60-year-old real estate agent partner or a 50-year-old loan officer may have a fundamentally different relationship with AI tools than the 30-something first-time homebuyer they serve. Effective change management acknowledges this and creates differentiated training, support structures, and adoption pathways.

The biggest mistake lenders make with AI is treating it as a one-time transformation project with a defined end state. AI is not a project. It is a continuous capability that will evolve faster than any implementation roadmap you write today.

Start with proof of concept, not proof of immediate profit. Your first AI deployment should demonstrate that the technology works in your environment, that your team can operate it, and that the desired outcome has been met – not necessarily that it generates a calculable ROI in the first quarter. Those metrics will come in time but demanding them too quickly creates incentives to deploy prematurely or measure narrowly.

Be equally cautious about “ROI” that moves in the opposite direction, or what STRATMOR Group Senior Partner Garth Graham not-so-affectionately calls the deadly duo of “Resistance of Innovation” and “Risk of Investment.” The lenders who will win in the AI era are likely neither early adopters who moved recklessly fast nor the skeptics who waited until competitive pressure forced their hand. They are the ones who pursued deliberate, staged evolution: learn, test, iterate, scale.

Finally, celebrate and share your AI + Human wins internally and externally. Real stories of loan officers who closed more business because AI cleared the administrative fog, or borrowers who got faster answers and a more personalized experience, do more to drive adoption than any training deck ever will.

The mortgage industry’s future is not about AI replacing all the humans, being forced off to pursue new careers in goat management. It is about AI-empowered staff members who can do more, know more, and serve more at the moment that matters most to a family navigating the single largest financial transaction of their lives.

The data is unambiguous: consumers of all ages are using AI, homebuyers trust it nearly as much as their agents, and lenders who ignore it will find themselves competing from a structural disadvantage they cannot overcome with talent or pricing alone. But technology without human strategy is just spending. The New Mortgage Dream Team – AI paired with skilled, relationship-driven mortgage professionals – is where the real competitive edge lives.

The question isn’t whether you’ll deploy AI. You will. Or whether the consumer will. They ARE. It’s whether you’ll do it with intention: clear on what humans do best, disciplined about where AI adds value, and wise enough to know the difference.

At STRATMOR Group, we work with lenders and technology partners at every stage of this journey, from AI readiness assessments and use case prioritization to change management frameworks and performance analytics. If you are ready to take your mortgage dream team to the next level and want an experienced guide in your corner, we would welcome the conversation. Sue Woodard

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.