“Objects remain at rest or stay in motion unless acted upon by an outside force.”

—Newton’s First Law of Motion.

Inertia affects us all, in work and in life, at some point. Right now, in the mortgage industry, inertia or the resistance to change, is a challenge many companies face and need to overcome.

We’ve written in the past about the decision mortgage business owners are facing: invest for growth, maintain, sell the business or shut it down. We work with lenders traversing each of these paths. In most cases, our work doesn’t begin until a decision has been made.

And that’s a problem because too many lenders are avoiding this crucial decision. And they’re running out of time.

Setting a strategy in an uncertain environment is one of the most challenging things a business owner or CEO can do. Making the wrong decisions carries significant risk. However, making no decision and waiting to see what will happen next may be the riskiest path of all. Hope, after all, is not a strategy.

Inertia is one of the fundamental forces of physics, describing an object’s resistance to a change in motion. But it also applies fittingly to business.

Company leaders can struggle to overcome inaction and initiate change within their organizations. Just as physical objects resist disturbances to their stationary state, businesses are often anchored in their old ways until an external force compels them to transform. Understanding this concept helps to explain why organizations get stuck and how executives can kick-start change.

Newton’s First Law tells us that objects remain at rest until an outside force acts on them. Massive objects require substantial energy to overcome their inertia and accelerate them into motion.

Likewise, large organizations have high business inertia rooted in past successes, established processes, legacy systems, and institutional mindsets resistant to change initiatives. Altering direction requires executives to apply determined leadership and strategic pressure. And to make a decision now, rather than defer.

Two major factors contribute to high organizational inertia: sunk costs and culture. Businesses accumulate enormous sunk costs in the form of systems, equipment, and employee skill sets optimized for existing operations. Pivoting strategies often require new investments that make previous expenditures obsolete.

Additionally, corporate culture breeds inertia when employee mindsets remain fixed in the status quo. Shifting embedded perspectives and behaviors necessitates substantial momentum from leadership. And here’s a perfect example of this.

For more than two years it has been evident that the industry has more capacity, in terms of human resources, than it needs to deal with current loan volumes. Empathy was a reason many mortgage executives held on to staff longer than necessary. While this may be a wonderful reflection of the compassion and respect that lives within our industry, the need to reduce costs and related staff remains clear.

We’ve seen multiple companies with staffing way out of balance, not because they chose that but because they refused to make a decision. They let inertia carry them. As a result, today’s lender productivity numbers are historically low.

Inertia exists to maintain stability, but when conditions demand responsiveness, organizations must actively counteract it. This is one of those times.

While hunkering down and waiting for the market to improve may seem like a strategy, it’s just business inertia. Nothing can change until an outside force acts on our home finance system. It’s time for leaders to be that external force, to take an active role in setting their strategy.

Because the real estate market certainly won’t be that force.

Most experienced mortgage executives have seen both rising and falling markets. Few, if any, have seen a real estate market like the one we’re in now.

Interest rates are above 7% and home affordability and inventory are both at historic lows. Despite that, the Mortgage Bankers Association (MBA) still expects to see about $1.7 trillion (4.5 million units) in new loan business, mostly purchase money mortgages, originated by year’s end.

Lenders know all of this. What they don’t know is when it will end. Without more housing stock or affordable homes for buyers to move up into, the real estate market is likely to remain volatile, regardless of what happens with interest rates.

The economy isn’t helping. Instead, it’s sending all kinds of mixed signals. While some may argue that we will see some improvements next year, we need to consider the fact that 2024 is an election year, when uncertainty will be at its highest. It is quite possible that the mortgage business will not show any improvements until 2025.

Can lenders afford to hold on to their large teams for that long? Even though many of today’s industry leaders come from a sales background, top company leaders are not going to be able to sell their way out of this problem. And even if sales improve, profitability is far from guaranteed.

We’ve focused in the past on expense savings from fulfillment staff cuts, and most lenders have already made those cuts. Now lenders need to address corporate administration, non-production support and sales productivity and compensation. A lower revenue and margin / lower cost operating model is the environment today and is likely to remain for some time.

Which means, the strategy, principles and assumptions that got you here will not get you there.

No, the market will not come to the rescue, not in time. It’s time for lenders to make a decision and manage from logic and reason (and valid data) not fear.

The greater the inertia, the more energy must be exerted to set change in motion. Still, every moment industry leaders let their companies operate on autopilot, the risk of failure grows.

Executives must break inertia by applying concentrated strategic force in new directions. This starts with clear, consistent communication of the vision and rationale for change.

Next, targeted investments in transformative technologies and upskilling talent provide the capability to align and accelerate operations.

Finally, incentive structures keep momentum going through ongoing measurement and reinforcement of change-ready metrics.

Like a rocket overcoming gravity to launch skyward, companies require concentrated leadership and strategic thrusts to fuel transformations that keep pace with evolving markets. Executives who proactively ignite momentum in the face of inertia will direct their business into the future, instead of being left behind.

But how does one do that, exactly?

It requires an in-depth analysis of current company strengths, weaknesses, opportunities and threats. There are four key questions to ask to get this information:

Note: use validated data in your analysis. Do not let hopeful, wishful, competitive thoughts influence your models and the related decisions. This article from fs (Farnam Street Media) illustrates this concept: Confirmation Bias And the Power of Disconfirming Evidence.

Few company executives can see their own companies from the inside clearly enough to complete this analysis on their own. And the insights from a comprehensive benchmarking evaluation are very helpful — I know all lenders are struggling, BUT are you struggling more or less than others? This is why our advisors have been meeting with lenders across the industry on a near constant basis for the past three quarters.

Making a decision before the leader has all the required information is incredibly difficult, as we mentioned in our introduction. But much of the data the leader needs to make an informed decision exists inside the company.

Often, an in-depth financial analysis of the company will reveal a path forward. The lender’s commitment to pursue it is the force required to break free of inertia and begin the work of preparing for the company’s next chapter, whatever that happens to be.

When we sit down with leaders and their managers, we usually start with an examination of fixed versus variable costs. They often confuse the two. For instance, a company with multiple branches may consider the cost of a professional processor, underwriter, or closer in each branch a fixed cost that cannot be avoided.

Those expenses can be considered variable, if the lender centralizes those functions or gets small branches to share resources. Once the decision is made, that expense becomes fixed again, but it will likely be lower overall.

The second place we often assess is the company’s compensation plan. For more information on that, check out my recent article, “Sales Compensation: Do You Get What You Pay For?”

Once you know where you sit financially, it is time to find out what costs you can still cut.

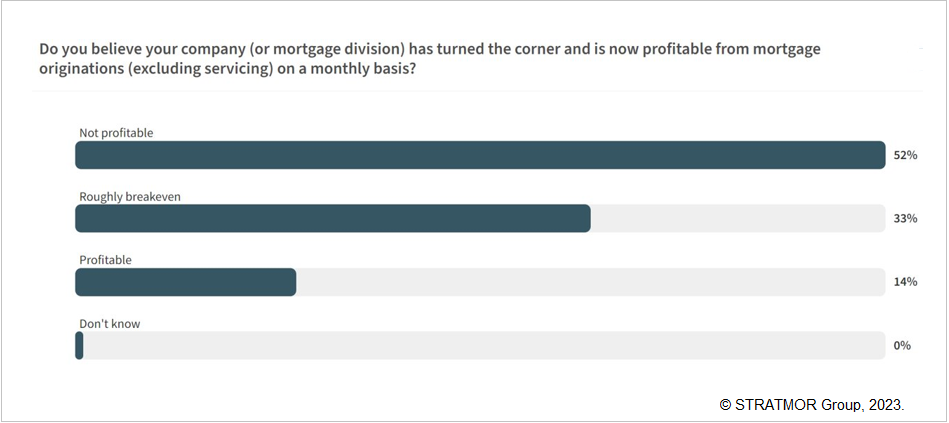

The work of lowering costs is critically important. We could talk about a cost to originate which is in excess of $13,000 or note historically low lender profitability, but the truth is every reader of this report knows how important this is to monitor and address. It came out loud and clear at our recent Operations Workshop.

When asked, only 14% of operations executives believed they were currently profitable from their current loan production.

Chart 1

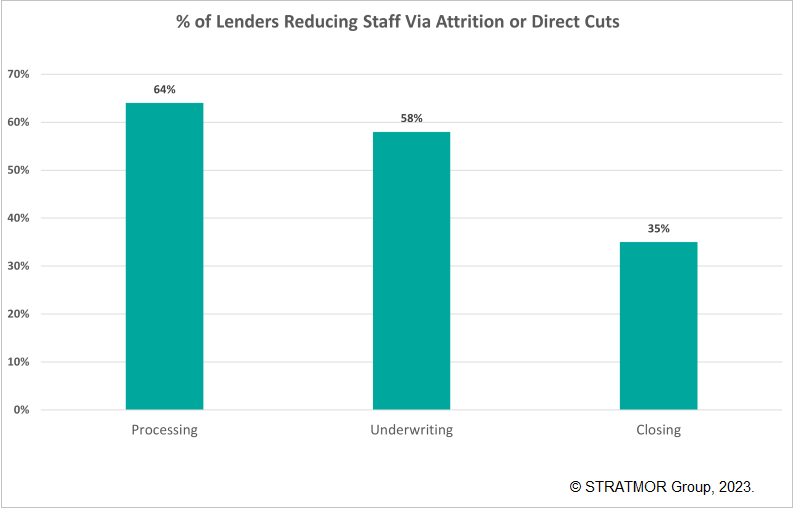

The first response to this should be cost cutting and lenders have been doing this for some time. They have begun outsourcing parts of the process, including loan setup, document indexing and final documents. They have laid off staff. Yet they need to cut more expenses.

When asked where they were still cutting, this is what they told us.

Vendors have been telling lenders for years that moving to an electronic, or at least hybrid, eClosing process will save them both time and money. Unfortunately, only 46% of lenders in our operations workshop admitted to using hybrid or full eClosings.

The challenge for lenders is not cutting so deeply that loan quality or compliance suffers. This requires the lender to rationalize staffing and maintain a span of control in remote environments that keeps them from losing control of their business.

Again, these are hard problems to solve from the inside. Lenders may benefit from outside counsel.

Cost cutting goes well beyond the basics we have covered here, and every lender should take the time to fully understand all the areas in which they can save. We have discussed many of the following ideas with lenders.

STRATMOR has a cost matrix to guide these conversations that can be used to ensure that no opportunities are left unconsidered.

Once the lender’s costs have been reduced as far as possible, it can be very helpful to analyze all current marketing and sales initiatives to find out where additional loan volume can be found.

This is problematic for many lenders who tend to fall back on their loan officer’s historic production levels to forecast the future. That won’t work in this market.

STRATMOR data show that more than 40% of the professional loan officers who were in the business in 2020 are no longer working in the industry. That’s not necessarily a problem as those were likely the lower achievers and have now washed out of the business.

It’s the top 40% that the lender needs to empower to find and close more loans. But of those, only the very best will get new business from the industry’s traditional purchase money business referral partners, the real estate agents.

Of the one million Realtors®, the bulk of the business will be won by the top 200,000 real estate salespeople. Together, they will sell about three million properties that require financing. With 100,000 loan officers still in the business, you can see how stiff the competition will be.

STRATMOR recommends that every lender produce three separate fiscal year sales forecasts: one that is aggressive, one that is conservative and one in the middle that should be more realistic than either of the other two. We are often called upon to help with these projections.

Many industry observers will act like the decision lenders are called to make today is a simple one. It is not. Making the right decision will significantly impact the outcome. Having the most possible information is the safest way to make this decision.

This is made more difficult by the fact that our industry does not often allow executives to step back from the spinning loan origination machine to think strategically. The nature of the business and the various stakeholders that every lender must answer to practically demands that they take a reactive approach to the business. That won’t work here.

Ultimately, lenders face a choice: fight on, sell or wind down. We support lenders on each of these paths, but we prefer to be involved earlier in the process, during data collection and analysis.

The reason is that company owners have been under significant stress for at least a year. Not collecting all the required information or considering their options will lead to a less than optimal decision and, ultimately, outcome.

And a decision must be made now. You cannot wait and hope that inertia will carry you through to a better market. Neither can you follow what you hope to be the wisdom of the crowd.

Deciding not to sell because very few mergers and acquisition transactions hit the press is a good example. Selling is a strategic option several lenders have and are considering now, but for every deal that is announced, there are typically three more that happen under the radar that are not divulged.

In fact, STRATMOR tries to avoid announcements of deals until well after the deal closes. So, the number of M&A deals always lags, and therefore, more companies are sold than the media will announce.

But for every M&A deal that gets done there are many more companies doing the little things that can add up to big changes in their business and keep their companies alive.

What’s the right move for your company now? We’d like to sit down with you and help you figure that out. We have deep insight into the commonalities of the environment all companies are living in right now.

But we should talk soon. Now, in fact, before it’s too late and some other force acts on your business to remove the inertia and takes away your ability to act.

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.