For the past few years, mortgage lenders have spent a great deal of time adjusting to a purchase-driven market. Refinance opportunities remain are still limited, margins are tight, and growth increasingly depends on attracting and retaining customers rather than just waiting for the next rate cycle.

I’ve said it before and I’ll say it again (because it’s THAT important to lender success): today’s mortgage environment has shifted borrower retention from a secondary consideration to a strategic priority. What is becoming clearer, however, is that retention is not primarily a marketing challenge. It is a relationship challenge, and that relationship is heavily shaped in servicing.

In STRATMOR’s MortgageCX servicing data, we consistently see the same pattern: lenders believe they’re losing borrowers to rate, product, or competition, but borrowers tell a different story. The decision to come back (or not) is often shaped long before the need for a new loan ever arises. It’s built gradually through day-to-day servicing interactions that either reinforce trust or, more commonly, erode it. Yet despite its importance, servicing often remains outside the core leadership conversation, treated primarily as an operational function with a focus on cost reduction rather than as a strategic asset.

In this article, we explore why servicing deserves leadership attention, where borrower experience is most at risk, and what executives can do to strengthen servicing as a customer and recapture advantage.

Borrowers typically interact with a lender for about 45 days during origination. After closing, that relationship can extend for five to ten years before the next loan is pursued.

Earlier this year at the MBA Servicing Solutions Conference, STRATMOR Customer Experience Director Mike Seminari made a simple observation: when borrowers describe their mortgage experience months or years later, they almost always describe something that happened during servicing — not origination.

MortgageCX data reinforces this. Fewer than 1 in 5 borrowers return to their original lender for their next loan, and often not because they were unhappy at closing. It’s because the relationship faded, or friction crept in, during servicing.

Mike’s point is worth underscoring: borrowers don’t compartmentalize “origination” and “servicing.” They remember the moments that created reassurance, or frustration, when they needed help. In STRATMOR’s experience, the servicing interactions that create the strongest (and most durable) impressions tend to fall into a few predictable categories:

These aren’t just operational touchpoints. They’re emotional moments, and borrowers remember them that way. None of this diminishes the importance of origination. But it does highlight where the long-term borrower relationship is actually formed.

Servicing should be treated as part of the enterprise customer experience strategy, not just the operational tail end of production.

Organizations that take this approach expand measurement beyond origination and into the life of the loan. This often includes:

These insights provide a much clearer picture of how the relationship evolves after closing and they allow leadership teams to connect servicing performance to borrower loyalty, recapture potential, and brand perception.

“What do we know about our borrowers’ experience one year after closing, and how confident are we that they’d choose us again?”

If the answer is unclear, servicing likely hasn’t yet been fully integrated into the organization’s customer experience strategy.

That gap becomes particularly important when borrowers return to the market. Recapture is now a central strategic focus in today’s purchase-driven environment. But it doesn’t begin with marketing campaigns or predictive analytics. It begins with the servicing relationship.

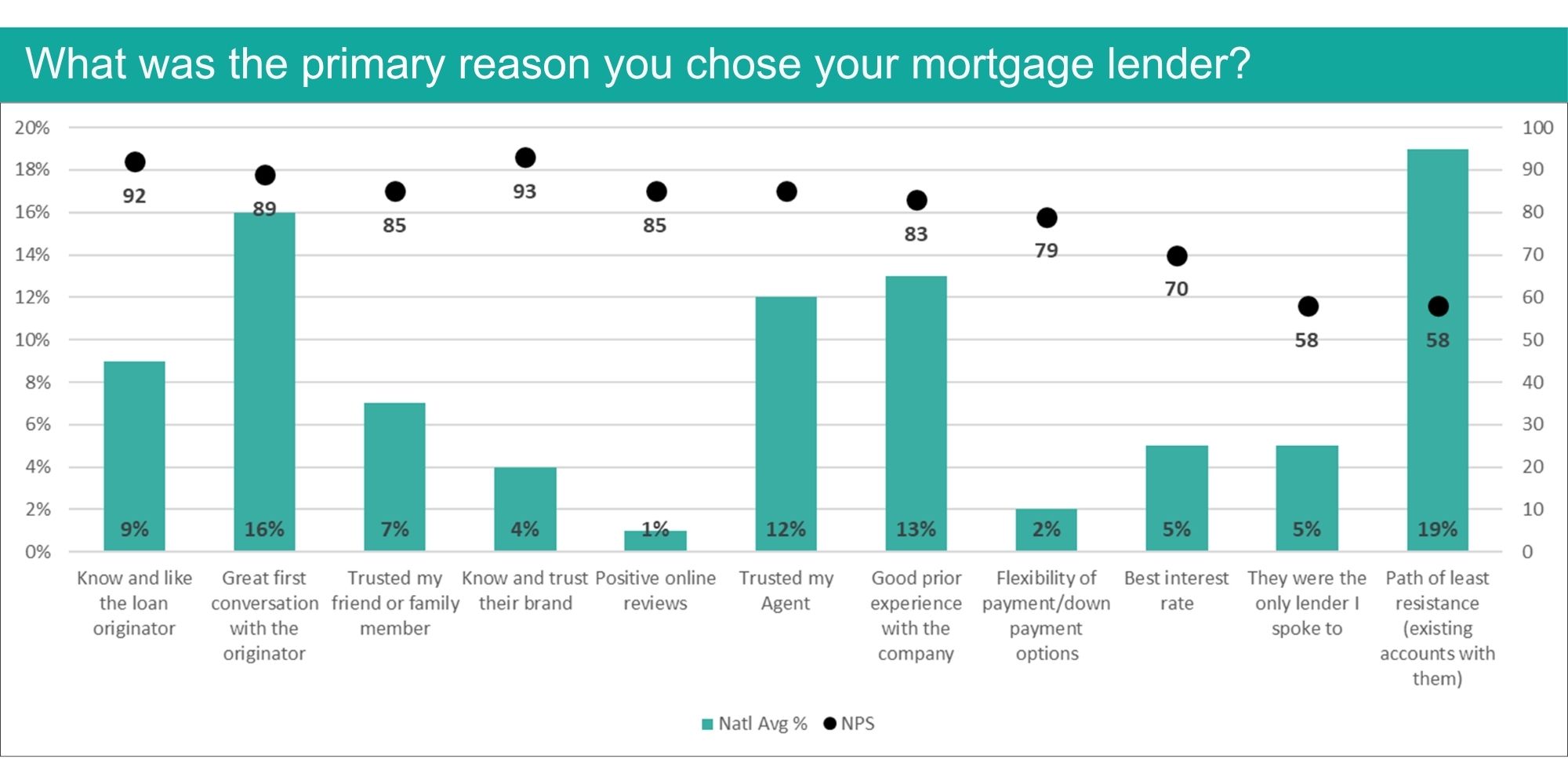

Borrowers who feel supported during servicing are far more likely to return to the same lender for their next financing need. MortgageCX data shows a consistent pattern: borrowers don’t shop first, they remember first. And who they remember is largely determined by how they were treated after closing. Borrowers who encounter friction often begin the search elsewhere.

Source: STRATMOR 2025 MortgageCX Survey Results

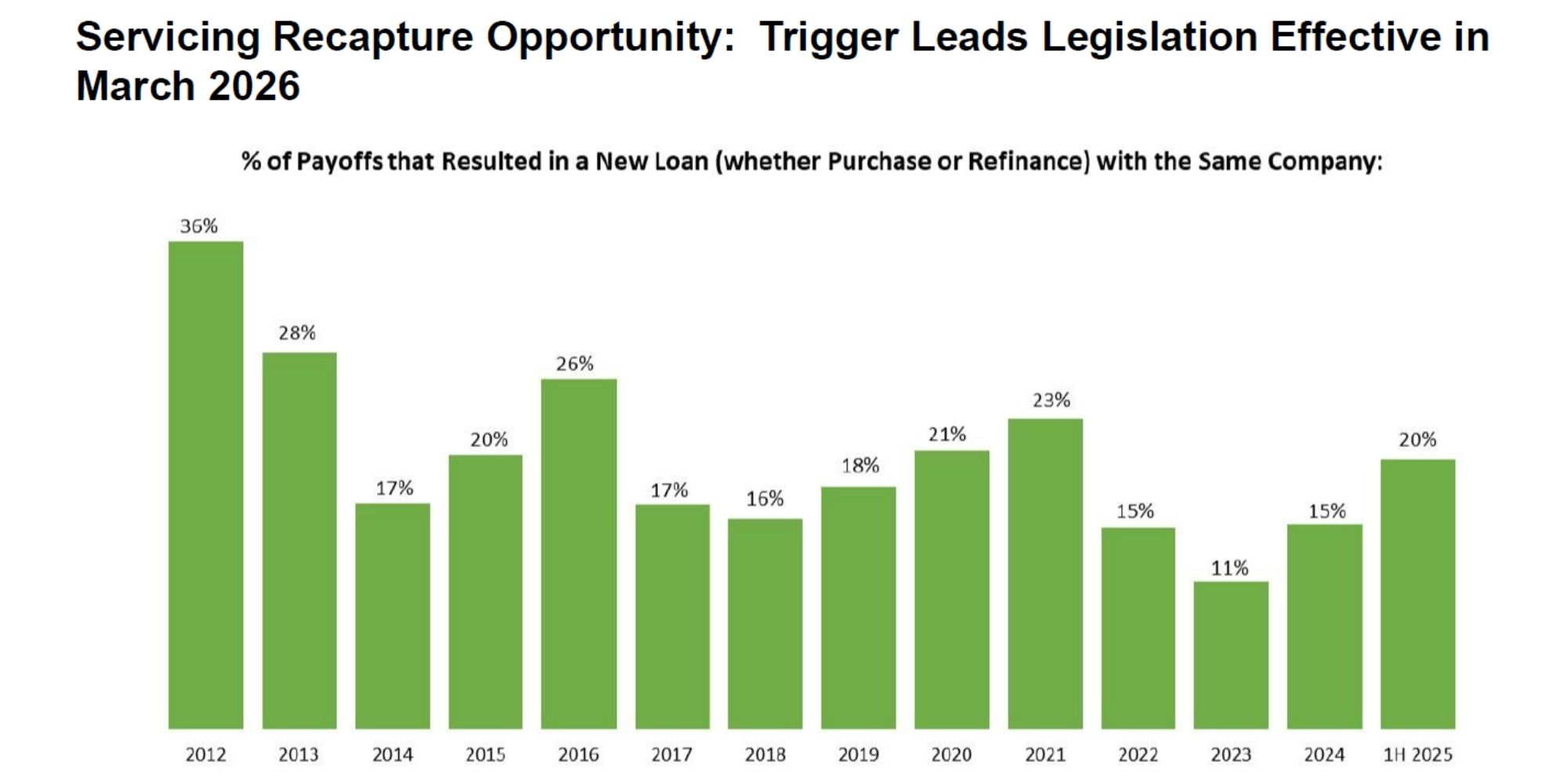

Industry data highlights this challenge. Over the past five years, servicing retention has averaged less than 20%, meaning the vast majority of borrowers ultimately choose a different lender when purchasing a home or refinancing their mortgage.

Source: MBA’s Servicing Operations Study and Forum; www.mba.org/sosf; 1H 2025 Only: PGR Program

Servicing interactions — monthly statements, escrow communications, payment assistance, and service calls — gradually shape borrower perception. When borrowers re-enter the market, those accumulated experiences heavily influence who they contact first.

Recent regulatory changes will likely reinforce that dynamic. The Homebuyers Privacy Protection Act, which went into effect earlier this month, restricts the use of trigger-leads, reducing lenders’ ability to reach borrowers after a credit pull. As lenders lose the ability to purchase immediate access to borrowers entering the market, competitive advantage will shift toward organizations with established borrower relationships.

In this environment, servicing becomes more than a cost center. It becomes a strategic lever for protecting portfolio value and supporting future originations. Yet many lenders continue to invest heavily in CRM platforms and predictive marketing models while paying comparatively little attention to the servicing experience that shapes borrower perception. If the servicing relationship is weak, marketing technology alone will not rebuild it.

Forward-thinking lenders are strengthening the connection between servicing and marketing by:

The servicing portfolio remains one of the most valuable growth assets lenders have. Realizing that value, however, depends on delivering a consistently strong borrower experience and maintaining the relationship long before the borrower returns to the market.

Many lenders rely on subservicers to manage operational complexity. These partnerships can provide scale, specialized technology, and regulatory expertise that are difficult to replicate internally. But borrowers don’t distinguish between lender and subservicer. They simply associate the experience with the lender whose name is on their loan. From a borrower’s perspective, there is no such thing as a “subservicer experience.” There is only your brand.

Across the industry, subservicing decisions are typically evaluated based on cost, compliance, and service levels. What is less common is consistent executive-level oversight of borrower experience outcomes. Without that oversight, lenders often discover issues only after complaints, negative reviews, or declining satisfaction scores begin to surface.

The question is not whether lenders should use subservicers. Many successful organizations do. The question is whether lenders actively govern the borrower experience their partners deliver. Organizations that treat subservicers as strategic partners tend to broaden oversight beyond operational service level agreements (SLAs). Borrower satisfaction metrics, review of customer interactions, and incentives tied to experience outcomes all become part of the management framework.

Treat subservicing relationships like strategic partnerships, not just operational vendors.

That means:

Some lenders are also establishing joint CX scorecards with their subservicers, ensuring both organizations are accountable for the borrower experience.

STRATMOR’s MortgageCX program shows that servicing satisfaction is highly sensitive to a small number of high-frequency interactions and a handful of high-emotion moments.

Satisfaction improves with clear communication about escrow adjustments, reliable digital payment tools, and service teams that resolve questions quickly without repeated transfers. When these moments are handled well, satisfaction compounds into trust, advocacy, and future opportunity. When they’re mishandled, borrowers disengage, often long before the lender realizes it.

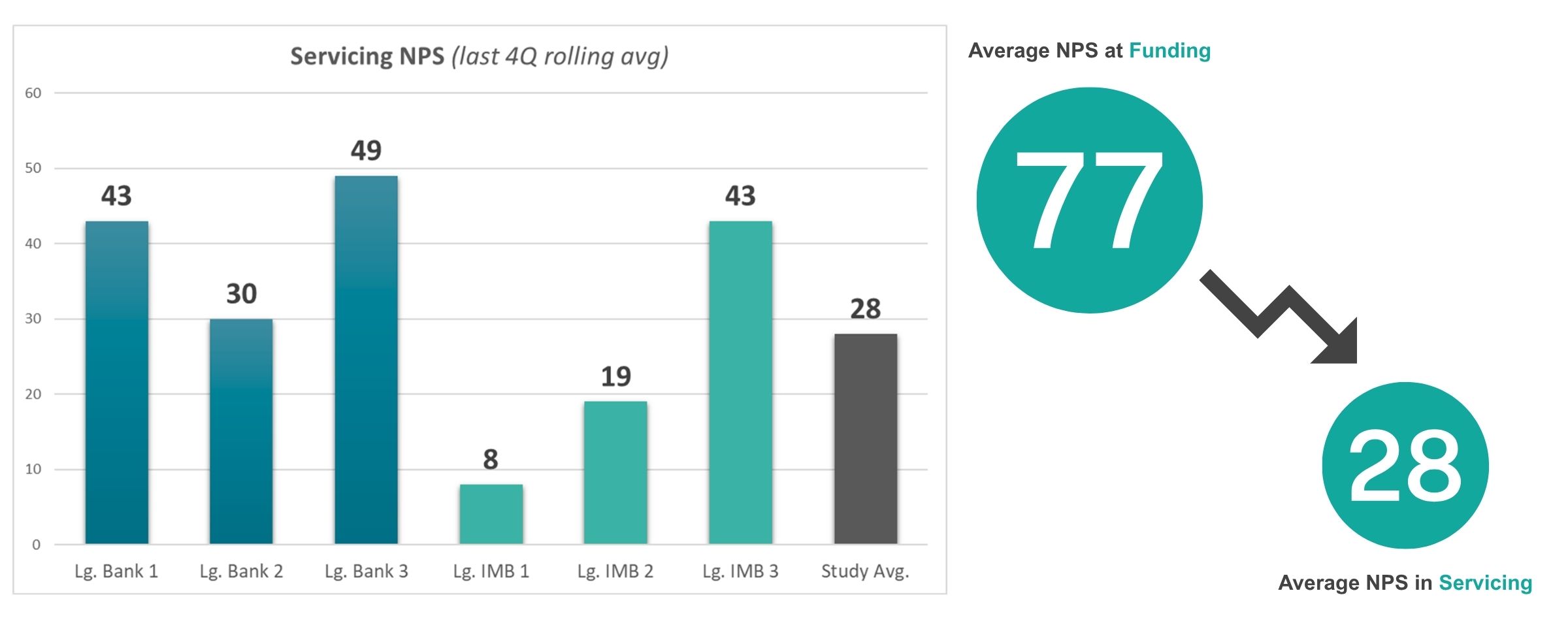

MortgageCX data shows that NPS drops significantly between origination and servicing.

Source: STRATMOR 2024-2025 MortgageCX Servicing Panel Survey

Dissatisfaction spikes around escrow “surprises,” inconsistent answers across channels, or multiple handoffs while trying to resolve an issue. Perhaps most importantly, many of these breakdowns are invisible to leadership, as borrowers rarely complain loudly. Instead, they simply choose a different lender next time.

Organizations that consistently score well in servicing typically focus on three areas:

Small improvements in these areas often produce outsized gains in satisfaction—and reduce avoidable call volume and escalations.

Technology is rapidly reshaping servicing but it doesn’t replace the need for human connection. Borrowers value automation for simple tasks. AI-powered chat bots, automated payment processing, and predictive analytics can streamline routine interactions and reduce borrower effort.

But when borrowers face complex or stressful situations, they still want human interaction.

Successful lenders are applying technology selectively by:

Technology should make servicing easier — not less personal.

As mortgage leaders evaluate strategy for the coming year, servicing deserves a place on the executive agenda.

Consider focusing on five areas:

As a parting gift, here’s a slogan you’re welcome to borrow and put on your mouse pads and coffee cups: “We’re not in the mortgage SERVICING business … we’re in the mortgage MEMORY business.”

For lenders that sell or transfer servicing, you’re not off the hook, you just have a different job. The borrower still needs to remember you when they’re back in the market. That comes down to how cleanly the transfer goes, how clearly you explain what’s happening, what contact you keep after closing, and how you reconnect at the right time. We’ll lay out a practical playbook for non-servicers in a future article.

Fo those who retain or outsource servicing, the limiting factor isn’t knowing what to improve, it’s sustained sponsorship from the top of the house. When executives prioritize servicing, align teams, and measure experience metrics with the same discipline as production results, performance follows. In a market where retention and recapture drive franchise value, leadership’s role is simple: set the expectation, fund the roadmap, and hold the organization and its partners accountable for the borrower experience.

STRATMOR helps lenders turn leadership intent into measurable results. Through our benchmarking and advisory work — including MortgageCX measurement, borrower journey diagnostics, and operating model and governance design — we enable leadership teams to pinpoint the servicing moments that matter most, quantify performance gaps, and align internal teams and subservicing partners around a shared goal: stronger borrower relationships and higher recapture rates. Garth Graham

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.