In February, I had the privilege of facilitating two “deep dive” Operations Workshops with a total of 120 operations executives representing 49 different mortgage lenders. These sessions are part of STRATMOR Group’s ongoing quarterly workshop program that also includes workshops focused on the Customer Experience and the Consumer Direct channel. Because things change fast in the mortgage industry, these meetings are a great way for participants to stay up to date on the latest trends, challenges and pain points.

There were few surprises in these two workshop sessions, mostly a confirmation and quantification of the key issues and challenges we see executives facing in today’s market. Participants openly shared their experiences and talked about how we transition to a “new normal.” In this article, I share my observations on the seven key takeaways from these great sessions.

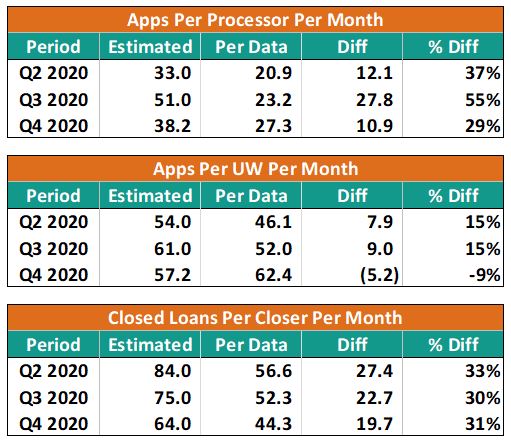

We asked COOs and other senior fulfillment executives what they thought their productivity was for key positions, such as processors, underwriters and closers. In addition, we collected average FTE numbers for these positions as well as application and closed loan data by quarter, which enabled us to calculate the actual productivity based on the actual data. The following tables summarize our findings.

© Copyright STRATMOR Group, 2021.

© Copyright STRATMOR Group, 2021.For Q2, Q3 and Q4 2020, with only one exception, executives believed that processor, underwriter, and closer productivity was much higher than the data would indicate, especially in the processor and closer categories.

So why the disconnect? Why would COOs, as well as heads of operations and fulfillment, think their productivity was so much higher than our findings indicated? First, and let me be clear on this, I believe these executives know what they are doing. Based on our workshop poll, their average experience in the business is 20-30 years and, in general, they have a great feel for their numbers and the key issues impacting their operation.

I believe the reason for this disconnect has to do with the definition of processor, underwriter and closer and the roles that are included under each functional area.

At STRATMOR, our view of productivity is “all inclusive,” meaning that we need to consider all roles in and around each major function. For example, the processing function may include roles described as set up, disclosure desk, loan coordinator, opener, validator, transaction coordinator, etc. This is in addition to the more traditional roles of processor, junior processor and senior processor. Similarly, in underwriting, besides the traditional underwriter position, we need to consider other roles such as appraisal reviewer / appraisal desk, condo underwriter, scenario desk, pre-closing appraisal reviewer, etc. The same holds true in closing. In addition to the traditional closer role, there are other roles in and around closing such as funders, doc drawers, closing disclosures preparer, pre-funding reviewer, etc.

With volumes at historic highs in 2020, lenders of all sizes faced acute shortages of experienced fulfillment staff. The cost of labor increased dramatically (more on that later), and this assumes that lenders were even able to hire the staff they needed. One of the primary ways that operations executives addressed this staffing shortage was to “peel off” certain tasks and activities and assign them to less experienced staff who are easier to hire. This kept experienced processors, underwriters and closers focused on higher value activities requiring more experience, and kept the loans flowing through the pipeline by delegating lower level tasks to less experienced staff. All that makes good business sense, but it also adds additional bodies into the mortgage fulfillment factory, and all staff must be accounted for to arrive at true productivity metrics.

To the point: operations executives tend to forget about the additional employees added into the fulfillment process when quoting or thinking about productivity metrics, and that, in our view, is the reason for the disconnect between their view of productivity versus the actual calculated metrics.

One way to ensure that all FTEs are accounted for is to view productivity at a more summarized level. At STRATMOR, we tend to focus on loans per non-producing direct FTE, which includes ALL employees from the point of sale through closing but excludes actual originators in Retail and Consumer Direct or account executives in the Wholesale and Correspondent channels. Lenders certainly know who their originators are, and so all non-originators from the point of sale to closing in the manufacturing chain are considered in this metric. This is a rock-solid metric and a great way to calculate trends and compare with other lenders.

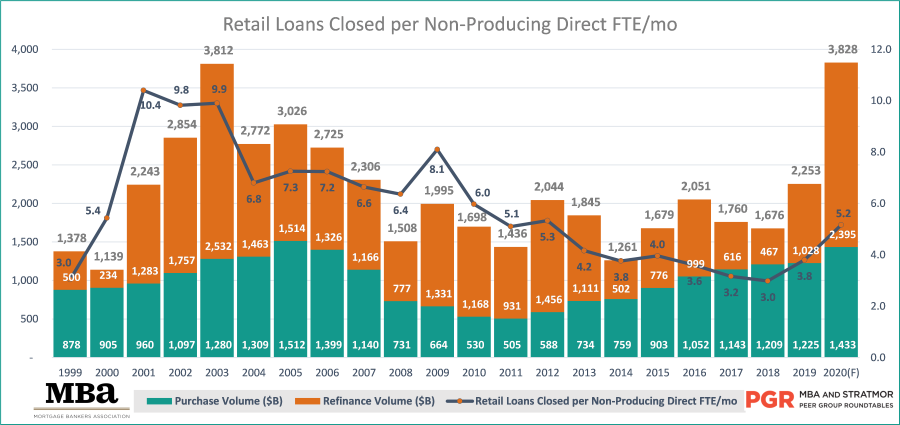

The following chart summarizes Loans Closed Per Non-Producing Direct FTE per month from 1999 to estimated 2020 levels.

Chart 2

Source: MBA and STRATMOR Peer Group Roundtables (PGR) program. For more information visit the MBA website

Source: MBA and STRATMOR Peer Group Roundtables (PGR) program. For more information visit the MBA website

The production data comes from the Mortgage Bankers Association’s (MBA) Research and Economics department and the productivity data was compiled from PGR: the MBA and STRATMOR Peer Group Roundtables program. STRATMOR has partnered with the MBA on the PGR program since 1998 and it currently includes 108 participating companies divided into peer groups based on size and operating model (Bank vs Independent).

Chart 2 shows the steady decline in productivity from 2001 to 2018, with a nice rebound in 2019 and 2020. I say nice rebound, but the estimated 2020 productivity only increased to 2015 levels and was a far cry from levels seen from 2001 to 2010.

But what is really happening here? The question is, how much of the increase in productivity in 2019 and 2020 is due to overtime being worked, versus increased efficiency in executing operations and fulfillment-related tasks? In other words, is productivity really increasing, or are we just working more hours? One thing is for sure, the large amount of overtime being worked is certainly muddying the water.

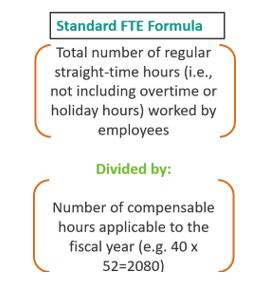

Since lenders know beyond a shadow of a doubt how many loans they close, the key variable is how FTEs are calculated. The classic FTE formula is as follows:

Source: © Copyright STRATMOR Group, 2021.

Source: © Copyright STRATMOR Group, 2021.In this standard formula, since overtime is excluded from the numerator, this results in an accurate number of full-time equivalent employees for HR purposes. While the FTE and compensation per FTE are more accurate using the standard formula, it overstates productivity to the extent that material amounts of overtime are being worked. If overtime is included in the numerator of the FTE calculation, this overstates FTE in terms of the actual number of bodies in the organization, but the productivity metrics would be more accurate.

So how are lenders addressing this issue? Based on discussions with the workshop attendees, most operations executives prepare separate calculations to normalize productivity metrics for overtime worked. The calculations boil down to this: how many closed loans (or applications, etc.) can be done in an 8-hour day or 40-hour week? These calculations factor out overtime, holidays, and PTO. By looking at productivity in this manner, operations executives can focus squarely on true productivity measures, without the “noise” created by the large amounts of overtime being worked in today’s environment.

Of course, overtime is not the only factor to consider when measuring productivity. Seasoned executives calculate more refined productivity metrics utilizing key factors such as purchase versus refinance mix, product mix including jumbo, government, and streamlines. While true productivity likely increased in 2020, it could have been much higher but for the large number of new hires added, including ramp up time, training, and churn/fallout.

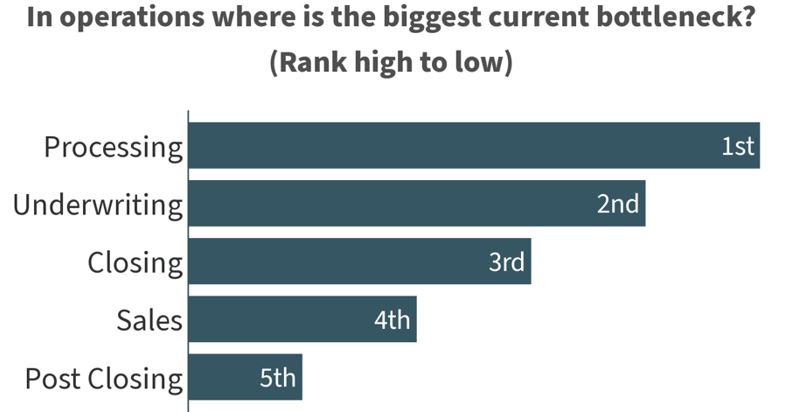

In our recent workshop sessions, we asked operations executives what their biggest bottlenecks were. Here is what they told us.

© Copyright STRATMOR Group, 2021.

© Copyright STRATMOR Group, 2021.Processing was ranked as the biggest bottleneck for a variety of reasons. Before we get into those details, it is important to consider some industry context.

As industry veterans know, there has been a huge amount of energy, interest and investment focused on Point of Sale (POS) systems in the mortgage business. Fintech firms such as Blend and Roostify have raised large amounts of capital and Loan Origination System (LOS) providers such as Encompass have made significant investments in their POS features and functionality. Much of the investment has focused on a user-friendly interface, creating a self-service, digital experience for customers.

This tremendous investment in the front end of the mortgage process enabled a record number of applications to flow through sales much more efficiently than say, 10 years ago. Sales staffing was relatively stable in 2020, with high productivity, high compensation, and low turnover. The sales side of the business has handled the volume better than fulfillment, and thus ranked fourth in terms of bottleneck areas behind processing, underwriting and closing.

But as loans flowed through sales with incredible velocity, the workflow often got bogged down in the processing area. What were the primary factors contributing to this bottleneck?

First, it is generally easier to hire and train new staff in processing, while underwriters and closers are harder to source and more likely to get promoted from within. Also, new processing staff may be assigned portions of the workflow such as loan set up or asked to focus on certain discrete tasks like ordering appraisal, credit, or other verifications. This “task-based” processing model is helpful as it enables operations management to add capacity, but it does add an additional layer of complexity and requires coordination across a larger number of staff. More than any other fulfillment function, the processing area is burdened with onboarding and training a higher percentage of new staff, who are also likely new to the mortgage industry.

In addition to having more new staff in the department, experienced processors are asked to execute certain tasks traditionally performed by underwriters. For example, in many companies, certain experienced processors functioned as junior underwriters, focusing on conventional, high FICO, W-2 borrowers often with appraisal waivers from the agencies. Experienced processors are either promoted to junior underwriters or stay in the processing group and serve double duty as processors and underwriters. So, experienced processors must train new staff AND interact with more staff responsible for certain tasks AND process more loans AND serve as junior underwriter on “easier” loans.

Finally, many lenders cite the use of multiple disparate systems as a prime cause of inefficiency. And who is at the center of that storm? You guessed it, processors. If there is not a tight, seamless two-way integration between the CRM, POS, Lead Management system and the LOS, the issues often come home to roost in the processing area, where the goal is to provide high quality applications with verifiable information to underwriters so they can make quality, timely decisions.

During our 2020 Q2, Q3 and Q4 operations workshops, we asked executives about staffing levels and hiring plans. The overwhelming sentiment was the dire need to hire staff in all fulfillment areas. There were simply too many loans and not enough staff to fulfill them. But for the first time in nine months, executives in our most recent workshop sessions in February indicated that, while still going strong, hiring has slowed down for some. Here is a sampling of what we heard:

Given our discussions at the February workshop sessions and the recent increase in mortgage rates, we can safely say that hiring for mortgage operations positions has crested. Also, most forecasts indicate an increase in rates and a drop in refinance volume in the second half of 2021. While pipelines are very strong, which portends a strong “last gasp” Q2 performance, most now believe that the second half of 2021 will be marked by declining volumes. Of course, with rates increasing and refinance application volumes slowing, margins, while still strong by historical standards, have begun to compress. If lenders believe that this compression marks the beginning of a market down cycle, it will make it harder to justify adding new operations staff.

Given the hiring frenzy of the past year, operations compensation has increased dramatically. According to operations executives, staff total cash compensation (excluding overtime) increased by approximately 15-20 percent from 2019 to 2020. The good news is that industry revenues have increased by far more than that, resulting in record industry profits in 2020.

Coming off our record 2020, the key questions for the industry are:

When STRATMOR’s Compensation Connection® Study results are released this spring, we will have a clear idea of the breakdown between base salaries and incentives/variable pay for the major mortgage banking positions. We believe that a large portion of the year-over-year increase in compensation will be in the variable pay/incentive category. We will no doubt see a spike in incentives in the 2020 data, driven by a large increase in retention bonuses, discretionary bonuses, “spot” bonuses to recognize the achievement of specific short-term objectives, and of course, signing bonuses (more on that below). While we expect the lion’s share of the increase in 2020 compensation will be in the variable/incentive pay category, there has been an increase in base salaries as well. Employees receiving large increases in base salary run the risk of facing a salary reduction down the road as the market turns.

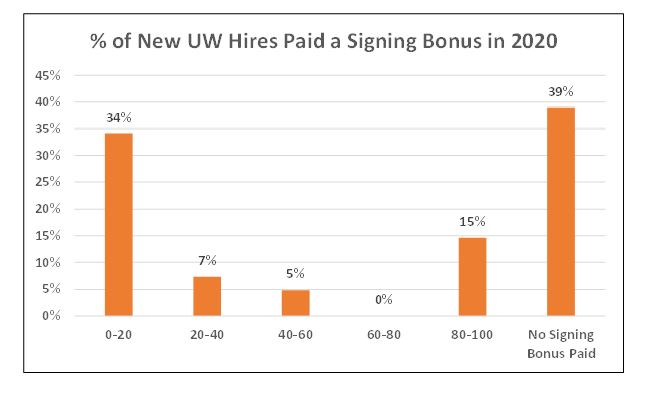

In the white-hot labor market of 2020, signing bonuses were a major topic of discussion. Everyone seems to have a story about the payment of large signing bonuses to attract experienced operations staff, especially underwriters and to a lesser extent, processors. We asked operations executives the percentage of time that new underwriting hires were paid a signing bonus in 2020 and the results are shown below.

Chart 5

© Copyright STRATMOR Group, 2021.

© Copyright STRATMOR Group, 2021.Based on a sample of 41 lenders, 61 percent paid signing bonuses to new underwriters, while 39 percent paid no signing bonus at all. The data seems to suggest that lenders either pay signing bonuses or they don’t, and our workshop discussions reinforced this notion.

For lenders that paid signing bonuses, their rationale included the following key elements:

Of the 39 percent that did not pay signing bonuses, these are the key factors cited:

While lenders were split on the topic of paying signing bonuses, there is no right or wrong answer. It is more a reflection of the lender’s philosophy and culture, which emanates from the owner(s) and is reinforced by the senior management team.

What is a virtual meeting these days without a discussion of Work from Home (WFH) trends? In our workshop sessions, operations executives discussed where they are on WFH trends and how they see the industry evolving into a “new normal” post pandemic. Most agreed that the new normal will include a higher percentage of remote workers across every major job category — it is just a question of degree.

Based on discussions with operations executives and recent discussions with other industry experts, we believe that the long-term implications of WFH will include the following key components:

Our industry won’t turn on a dime, but as WFH takes hold, we will evolve into a “new normal” of lower compensation costs, less volatile labor costs in normal markets and higher employee turnover.

The team at STRATMOR looks forward to meeting with the industry’s best and brightest executives at our various recurring workshops to discuss strategies and tactics to manage through the current environment. As we think about these sessions in the coming quarters, our industry will likely exchange its existing problems for a new set of challenges. We will trade a labor shortage, WFH issues, compensation escalation, capacity management and fulfillment bottlenecks for margin compression, managing excess capacity, cost management, industry consolidation, WFH re-entry and a more intense focus on automated processes and tasks. Whether in a boom or bust market, when you face uncertainty, call upon the STRATMOR Group to help you make sense of the data and make better decisions for a more successful future in this crazy and challenging business we call the mortgage industry.

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.