There’s no doubt that the mortgage industry is feeling the effects of the COVID-19 coronavirus. Even as the Fed cut its benchmark interest rate by half a percent on March 3 and sent lenders into a scramble to manage borrower expectations and margins, businesses in Washington and California were encouraging employees to stay home if they were ill and to work from home, if possible.

By the time the Fed cut the rate to zero percent on March 15, the virus reached pandemic status. The U.S. declared a national emergency and gatherings of more than 50 people were canceled. “Stay home if you’re sick, work from home if you can” became the national refrain as life in the U.S. changed in a matter of days.

Businesses are managing, hour-by-hour, edicts from federal, state and local authorities that impact their operations. Mortgage lenders are no exception. Lenders have the added stress of managing the expectations of investors and borrowers through the maelstrom of impacts to the loan process compounded by massive changes in capital markets, MSRs, working conditions and technology needs. It’s all hands on deck just to keep the ship on course, and in this article, we examine what lenders are dealing with as the COVID-19 waves continue to swell.

Managing capital markets in mortgage banking entails a little bit of art and a lot of science. The goal is to optimize revenue and profits, managing liquidity and mitigating interest rate risk along the way. This is a difficult and challenging job in normal circumstances. Throw in a world-wide pandemic in which financial markets are massively disrupted and world economies literally hit the “pause button,” and capital markets executives have an unprecedented and monumental challenge. At the risk of losing relevancy by the time this goes to print, our goal here is to summarize the key issues and concerns faced by capital markets executives in today’s rapidly changing environment.

Here is STRATMOR’s take on the key concerns and risk areas:

Managing capital markets in mortgage banking is a tough job, and in today’s market, the challenges are almost frightening with so much uncertainty and so many unknowns. High performing capital markets executives are monitoring markets closely, making mid-course adjustments daily, and above all, keeping an eye on cash.

The COVID-19 virus is having a significant impact on owners of Mortgage Servicing Rights (MSRs). MSR owners must take a holistic approach in this highly volatile market, taking into consideration many factors impacting cash flows that seem to be changing every day. Here are the critical factors that MSR owners should consider in today’s market:

While this may seem like a risky near-term strategy, entities that are able to retain servicing today will build a potential annuity stream of servicing income which will strengthen their financial position once this refinance wave is over. Projecting the cash flow demands of the origination and servicing business in a truly stressed environment is critical. Owners of MSRs need to be hyper vigilant in order to optimize cash flows and mitigate their financial risk.

As the virus began to break in the U.S., Microsoft, Google, Amazon and Twitter all recommended that as many of their employees as possible work from home to help minimize the spread of the virus. Even before President Trump called for older Americans to stay home and for everyone to avoid groups larger than 10 for 15 days to try to slow the spread of the virus on March 16, many more companies were sending staff home to work remotely. For many sectors of the financial services industry, including mortgage banking, remote workers have been in place for some time.

Across commerce, remote workers have become increasingly common. According to Global Workplace Analytics in the March 2020 update to their telecommuting trends report, regular work-at-home among non-self-employed people has grown by 173 percent since 2005, 11 percent faster than the rest of the workforce (which grew 15 percent) and an estimated 43 percent of employees work remotely with some frequency. The report notes that 62 percent of employees say they could work from home (Citrix 2019 poll).

As the spread of COVID-19 drives operational decisions and government directives mandate, more lenders are turning to a remote model to maintain operations and work surging pipelines. STRATMOR encourages lenders to be flexible — give as many roles as possible the opportunity to go remote.

The trend of underwriters working remotely has grown out of necessity through the last few years as volumes grew and lenders were not able to find talent in their local markets. According to data from STRATMOR Group’s Compensation Connection® Study, the percent of underwriters reported as fully remote grew from 20 percent in 2014 to more than 39 percent in 2018. Before the coronavirus crisis, 62 percent of lenders reported they currently allow for remote work in at least one fulfillment position (processors, underwriters, closers).

“The roles associated with closing loans are the ones lenders should look into making remote right now,” says STRATMOR Senior Partner Nicole Yung. “These are the roles that will be buried in work in the coming weeks under the high volumes we’re experiencing. With the recommendations for people to work from home, and because these fulfillment roles are critical to continue to keep the loans moving through the pipeline, lenders would do well to focus on converting in-house closing work to remote as soon as possible.”

Outsourcing is another option that enables lenders to pick up workloads left incomplete by staff who are decommissioned due to the coronavirus or for work that just cannot be completed due to the surge in volume. Under the best circumstances, executing an outsource strategy is a complex undertaking that cannot be implemented quickly, and as of this writing, a multitude of offshore providers in India, the Philippines and elsewhere have sent their workers home. This has left many industries, including mortgage, scrambling to take over functions previously outsourced. Domestic outsourcing may be the best option with offshore arrangements in short-term crisis.

In the eyes of regulators and investors, the lender is responsible for any function that the vendor does, or fails to do, so even if the lender has strong representations and warranties with the vendor, the lender is responsible for output and outcomes regardless of who performs the work. The lender must be comfortable with how the vendor performs the work, trains and manages their team and that the services rendered will be of more value than the risk the lender incurs by having another entity perform the actual work.

There are two types of outsourcing:

End-to-end outsourcing is a long-term solution and is most likely not a viable option for dealing with the immediate needs we’re experiencing. End-to-end requires significant advance preparation, over and beyond the contract negotiations. The lender and vendor must agree to the processes that the vendor prescribes, or the vendor must clone the lender in terms of methodology. Decisions must be made as to the technology that is to be used and the reporting and communications standards between the vendor’s and the lender’s staff and with the borrowers.

Component outsourcing is a viable option for lenders as it focuses on specific tasks, such as file set up, ordering services, scanning and/or indexing incoming documentation, preliminary reviews of documentation, post-closing reviews, shipping loans, obtaining trailing docs, and the like. While these tasks are critical, it is less subjective work and none of the tasks require borrower contact, and it takes much less time to get the vendor’s staff up and running and effective.

Typically, each of these tasks are assigned to specific teams — the team only needs to learn and be proficient at one part of the process. Many large lenders utilize component outsourcing to minimize the amount of work that is performed by their staff, so that they can be freed up to do the more complicated work and to communicate more frequently with the borrowers.

An important consideration during this pandemic is the physical location of the vendor’s staff. Are they in a coronavirus hot spot where they will be subject to the same issues that we currently face? Can their staffs work remotely — and if so, what are the implications for the security and privacy of your borrower’s data? There are advantages to vendors that can orchestrate round-the-clock support, but if security and privacy are compromised, the lender is placed at risk.

Another consideration: is the vendor currently providing the same services for other lenders? If so, you have an advantage in that the vendor doesn’t have to create a new process to support your work. If you agree with their methodologies and processes, then the implementation time should be faster. And, if they can mix experienced staff with new hires for your team, the ramp-up time to get their team fully functioning will be reduced.

The overarching factor in outsourcing is that the lender is held responsible for anything that the outsourcing vendor does or doesn’t do. Regardless of the representations and warranties that are negotiated with the vendor, the lender’s reputation and ability to do business could be at risk, so careful vetting and due diligence of the vendor is needed prior to embarking on a relationship, and then careful management and attention to performance is required after the service is implemented.

Other considerations:

In a typical market environment, a borrower’s journey through the loan process can move quickly from delightful to dismal based on how communications are handled. In this time of market volatility and interest rate uncertainty, lenders must keep up and even improve communications with borrowers or risk serious damage to their reputations.

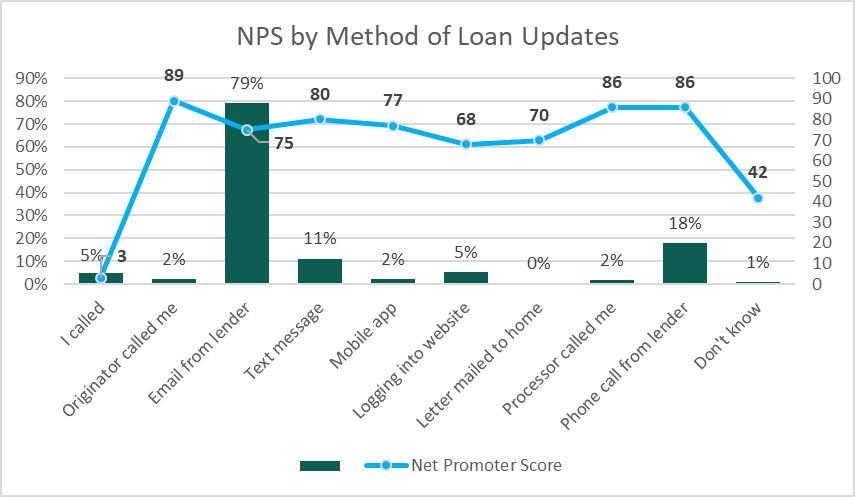

“We live in a world where information about borrowers’ experiences with their lenders is readily accessible to other potential borrowers — and is increasingly important as they narrow down their choice of a lender,” says Mike Seminari, director of STRATMOR’s MortgageSAT Borrower Satisfaction Program. “The data we have from surveying more than 130,000 borrowers annually shows how borrowers expect and prefer to be updated, and even more importantly, how update methods correlate to the difference between borrowers who will recommend the lender and those who will not.” The fact that 79 percent of borrowers receive updates via email — with a corresponding 75 Net Promoter Score (NPS), and just two percent receive updates by personal phone call — with a corresponding 89 NPS, presents a huge opportunity for lenders to differentiate themselves from the competition and garner referral business. “Trust me,” says Seminari, “you’ll need it once this refinance craze runs its course.”

Seminari recommends:

“The lenders that come out of 2020 with reputations intact will be the ones who are able to anticipate the things that could go wrong and create and adhere to a plan to address problems for the borrower quickly,” says Seminari. “This means, more than anything else, encourage originators and processors to ramp up communication throughout the loan process.”

On March 16, McKinsey & Company released a timely, insightful report about the COVID-19 evolution and implications for businesses. STRATMOR recommends reading this report which we believe does a great job framing current scenarios, economic impact, supply chain challenges and, most importantly, implications for businesses and how companies should respond to this pandemic.

McKinsey recommends seven actions businesses can implement now — STRATMOR suggests lenders consider these steps for your business:

We hope this article provides value to STRATMOR clients and our industry. Contact us for additional information and assistance.

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.