for these free STRATMOR

online publications

The other night, I was helping my youngest daughter look for a stuffed animal she absolutely could not sleep without. It was one of those parenting moments where the stakes feel wildly disproportionate to the object in question. We searched everywhere — under beds, behind couches, inside toy bins, even in the freezer (don’t ask).

After about twenty minutes of tearing the house apart, I said, “Maybe, if we can’t find him, we can just get a new one…?” That was the wrong thing to say, and tears ensued. Logically, it made sense. There are thousands of identical stuffed animals in the world. Amazon could have delivered a new one by morning. But that wasn’t really the point. She didn’t want a different stuffed animal. She wanted hers. The one that had been with her every night. The one that had history. The one she trusted.

And it struck me later, as I reflected on the MBA Servicing Solutions Conference in Dallas, that our industry is having a very similar conversation right now. There was tremendous excitement around AI related to predictive analytics, intent data, identifying borrowers who are “in the money,” surfacing refinance and purchase opportunities before competitors do. The tools are impressive. The models are getting sharper by the month.

But it left me wondering whether we’re confusing the ability to surface an opportunity with the ability to convert it. Because just like with my daughter, the “opportunity” isn’t worth much if the relationship hasn’t already been built.

Our question this month: Which will lead the recapture charge — AI modeling or customer experience?

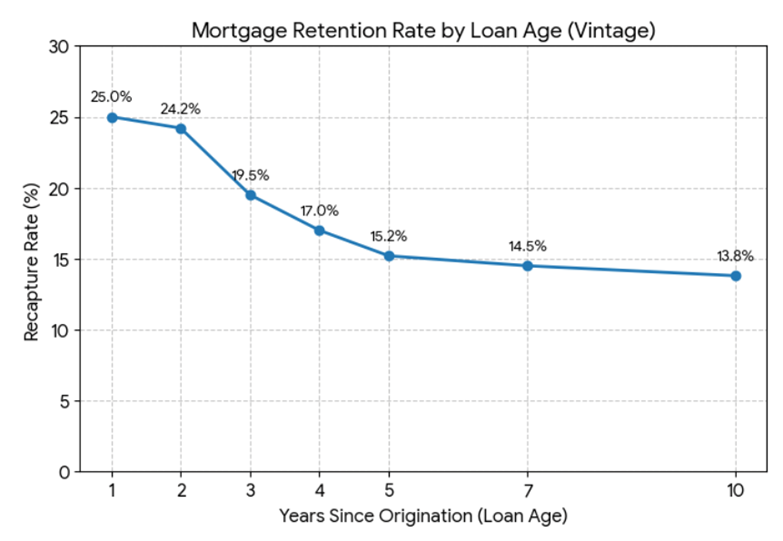

STRATMOR data has consistently shown that only about 18% of borrowers return to their prior lender or servicer for their next transaction. That number declines over time, starting around 24% for year one and two, then settling closer to 15% percent by year five. In other words, most borrowers do not come back.

(Source: Mortgage Bankers Association, 2015-2025 Servicing Retention by Vintage)

And it’s rarely because another institution had some revolutionary pricing advantage. More often, it’s because the relationship faded. The lender became out of sight and out of mind. The borrower felt neutral.

Neutrality is dangerous. Borrowers do not need to dislike you to leave you. They simply need to feel nothing.

As servicing portfolios become increasingly data-rich, it’s tempting to believe that identifying rate sensitivity and intent signals will solve retention. But if borrowers have felt invisible for three years, a perfectly timed refinance call feels opportunistic. If they have felt understood, guided, and valued, that same call feels helpful. The surfaced opportunity is identical. The response is not.

At the conference, much of the energy centered around identifying the precise moment a borrower becomes refinance eligible. Who is browsing? Who requested a payoff? Who’s in a rate band that now makes sense? All of that is smart strategy, but it assumes that timing is the primary driver of conversion.

The deeper issue is relational equity.

Whether a loan enters your portfolio through origination, a bulk MSR purchase, or a subservicing relationship, the first six to twelve months after onboarding begin determining future behavior. That is when borrowers decide whether they understand your statements, whether communication is clear, whether they feel like an account number or a person.

Most servicing organizations treat onboarding as operational. From the borrower’s perspective, it is emotional. It sets tone and expectation. If the early experience feels transactional, the relationship never deepens. And when opportunity surfaces years later, there is no attachment to draw from.

AI can tell you when someone is ready, but it cannot make them loyal. And loyalty is built long before the moment of opportunity.

If we accept that surfaced opportunity without relational equity is hollow, then the strategic focus shifts.

Final Thought: What my daughter was so upset about was the loss of the relationship, not the object. You can surface a thousand identical stuffed animals. None of them carry history.

In the same way, we can surface refinance opportunities with increasing precision. The data will only get better. The alerts will only get faster. But if the borrower does not already feel connected to you, that surfaced opportunity has very little power.

To find more Customer Experience Tips, click here.

MortgageCX is now integrated with Encompass®!

Start receiving monthly Customer Experience Tips

Feel free to reach out with any questions or needs we might be able to help with.