There is no version of the future that doesn’t include Artificial Intelligence — AI. That genie is out of the bottle, and the only thing that will determine whether it will be for good or ill will be the wishes we make.

We know what fraudsters will wish for and the power AI will likely give to them, which unfortunately will make them much more effective. But what wishes should mortgage lenders be making now and how likely is it that AI will be able to deliver?

To find out how AI is apt to change the mortgage industry, we surveyed STRATMOR experts, all industry veterans with decades of experience. Then we asked them to comment on the answers we received when we posed the very same questions to the current poster child for AI, ChatGPT.

In some cases, their answers aligned quite well while diverging in others. What emerged offers a glimpse into what may be our best-case scenario for how we will share the future with these powerful new technologies.

In some cases, their answers aligned quite well while diverging in others. What emerged offers a glimpse into what may be our best-case scenario for how we will share the future with these powerful new technologies.

At the risk of telling you something you’ve heard a few million times now ChatGPT is a “language model trained to produce text” that helps the user compose content, from emails to essays, in response to questions you ask it.

This AI is a result of OpenAI, a nonprofit organization funded by some of the wealthiest technology companies and leaders in the world, including Elon Musk and Microsoft. Together, they have spent billions on their digital child.

Their investments paid off, resulting in the fastest growing consumer app in history. Today, users everywhere are using it for everything from creating complete software apps to authoring complete novels and screenplays to writing breakup letters.

But what can it do for our industry? We asked it. Here is what it told us.

AI can significantly transform the mortgage industry in several major ways:

How do we interpret this response?

One of the first things we learned about large language models (LLMs) in the process of querying ChatGPT was that the quality of the result depended a great deal upon the prompt provided to the model.

This has become so important that many businesses have gone in search of people who can produce prompts that will result in better answers. A recent article by Time magazine points out that prompt engineers can command mid-six-figure salaries.

Ask a general question and you get a general answer. To really circle in on the information you need, you must be very good at asking the right questions.

Source: © Marketoonist, AI Tidal Wave. Used with permission.

Source: © Marketoonist, AI Tidal Wave. Used with permission. One of the benefits of human consultants is they have a history with their clients’ peers that lets them know, in advance, what questions their clients need answered. ChatGPT can’t do this, and so we received a very general response to our prompt. As you might expect, the STRATMOR consultants saw much more detail in our industry’s future.

“We talk about ‘automation’ and ‘AI’ as the same thing, which it is not,” says STRATMOR Principal Jennifer Fortier. “’Automation’ means taking the human out of routine repetitive tasks and ‘AI’ means simulating human thinking. So, when we talk about AI features, my mind goes to ‘what human-like thinking is it doing?’”

This may lead some, including ChatGPT given its answer above, to think AI is ready to start underwriting mortgage loans. It’s unlikely any industry compliance officer will authorize the flipping of that switch.

No one can say how long it will take AI to move into the underwriter’s office, but we know that’s not where it will start.

We know this because the AI takeover has already begun.

“Today, the most appealing feature AI is offering us is document and data point recognition — finding data and figuring out what it is,” says Fortier. “Once data is identified, the system can then run a series of automated comparison checks or rules. When the rules fail, there is an exception task routed to a human user.”

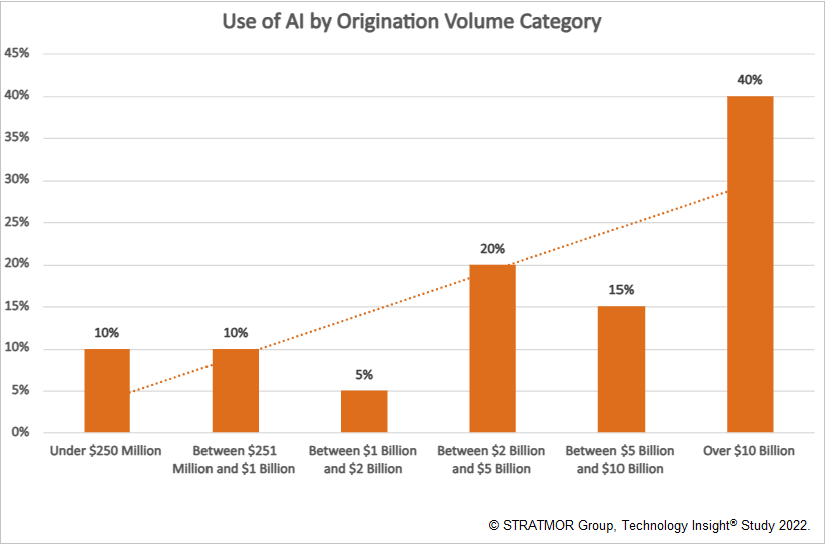

And that’s where we’re already seeing lenders make new investments in AI-powered technologies. According to data from STRATMOR’s 2022 Technology Insight® Study, 22 percent of responding lenders are already using AI. As you might expect, large lenders tend to invest in AI and machine learning tools to a greater extent than smaller lenders. This is not a big surprise, as our data on technology spending indicates that larger companies spend more on technology because they typically have the capital and the scale economies to do so.

Chart 1

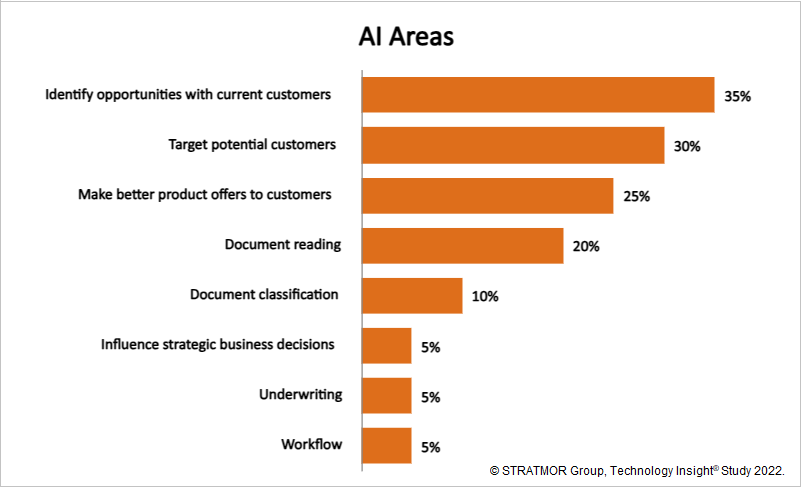

Chart 2 shows the ways responding lenders are using AI currently. Note that the top three uses of AI have to do with marketing to customers, followed by document reading and classification. In short, it appears that AI has gained more traction in marketing than in operations and fulfillment.

Chart 2

“We still need a human to do the thinking when the system cannot accommodate situations that are not a clean pass or fail,” says Fortier. “So, today, the most practical use of AI in the mortgage process is figuring out what the data is, which is a considerable benefit for efficiency, accuracy, and transaction speed.”

STRATMOR Senior Advisor Brett McCracken adds that AI could eliminate the dreaded “stare and compare” that, despite current automation efforts, still plagues the industry.

“AI can compare data fields across stored database values and information pulled from static documents uploaded from borrowers and third parties to run sophisticated rules from investor guidelines and internal overlays,” says McCracken. “AI should be powerful in the near-term at handling the most mundane tasks being assigned to lower cost resources inside of lending organizations especially for the work that follows a very predictable pattern.”

The question now is when more lenders will embrace it.

There are mountains to climb to implement AI in the mortgage industry. ChatGPT offered this shortlist:

Fortier points out two major challenges to implementing AI in the mortgage industry. First, we must transform our process, and not just layer on another technological solution. And then we have to get lenders to adopt it.

“Unfortunately, this is not as simple as installing the AI solution and seeing meaningful results,” she says. “The lender needs to take a hard look at how the workflow should be changed to fully optimize the benefit of the AI solution.”

Closely related to process transformation is the issue of user adoption.

“Every lender is familiar with old manual processes that just will not go away, despite deploying solutions to streamline the work. User trust and ‘old habits die hard’ factors are big obstacles and not easy to overcome, particularly in the absence of workflow redesign,” Fortier says.

STRATMOR Principal Jennifer Smith sees similar challenges. “The challenges I see for implementing AI in the mortgage industry are twofold: one, having leadership who not only understand what AI can and cannot do, but who have reasonable expectations of the results it will yield, and two, having someone in the lender’s shop who understands the AI being implemented and will monitor and manage it going forward,” she says.

Many lenders don’t have this level of understanding yet, nor the staff to manage the AI once it’s in place. And that’s just the beginning of the challenges.

“Cost, internal expertise, and specific use cases of where to start are still holding lenders back,” says McCracken. “There is also some concern that AI will spook existing employees who could view implementation of AI as the first step in replacing them, instead of seeing the technology as complementary to their skill set.”

He adds that some lenders are not convinced that the companies offering AI services for mortgages are offering the right solutions for their organization. In some cases, the lenders are likely correct.

McCracken suggests asking the following questions of any vendor promising to deliver an AI-powered solution:

That last question is very important, especially given the fact that about 40 percent of CEOs polled for a Yale CEO summit think AI could destroy humanity in five to 10 years.

No one on the STRATMOR team thought AI was going to burn the world down. Rather, they were unanimous in their regard for the new tools technologists are developing and excited about their present and future uses in the industry. However, there are some caveats.

Even ChatGPT admitted that it is “unlikely to replace all human interactions entirely. Human expertise, empathy, and the ability to handle complex scenarios remain crucial for providing personalized guidance, addressing specific borrower needs, and establishing trust in the mortgage lending industry.”

The most effective approach, according to ChatGPT, will be a combination of AI-driven automation and human interaction, leveraging the strengths of both to deliver an optimal customer experience.

Fortier accepted that answer: “I think AI can eventually replace most non-borrower facing tasks on the mortgage loan. When AI can do more to simulate human thinking and intelligently assess questions that are not as easy as ‘pass or fail,’ we will have reached a tipping point into AI.”

Fortier also thinks AI could get good enough to suggest the right products and scenarios for borrowers, reach intelligent loan analysis conclusions, make the transaction very simple, and provide timely and accurate information to the borrower upon request, all to a degree that the borrower does not need direct interaction with the lender.

“When that is possible, I can envision the ability (but maybe not the preference) to replace most of the human interaction. The question is, when will AI get good enough for that and what will it take for a lender to be willing to hand that over to machines?” she asks.

Jennifer Smith isn’t looking for this to happen anytime soon. “I do not see AI replacing all human interactions between the mortgage lender and the borrower,” she says. “Where AI cannot replace a loan officer, a place digital lending has also failed, is by providing a sounding board and voice of reason and reassurance to a borrower.”

She points out that if customer satisfaction is the goal, humans must be part of the solution. “When — heaven forbid! — a borrower is irate, they do not want to talk to a non-human. I can’t imagine AI trying to placate a borrower whose closing date has been moved or who has received a foreclosure notice,” Smith says.

But despite all of this, everyone we spoke to for this article agreed that AI would be an important tool for lenders in the future.

Change is never easy. It comes to every industry eventually and no one likes it. We’ve already mentioned the fear on the part of industry labor that they will be made obsolete by these new tools. Some of them will.

As that happens, the industry will grapple with some ethical considerations.

ChatGPT puts it succinctly: “The adoption of AI in the mortgage industry brings forth several ethical considerations that need to be addressed to ensure fair, transparent, and responsible use of AI technology.”

Here are several ethical issues the AI found:

“The ethical considerations for the mortgage industry are the same as for most industries — bias and disparate impact, privacy concerns and undetected systemic mistakes,” Fortier says. “Then there are the existential questions. AI will require us to make major pivots in how we are employed, how we create and brand our work and how we satisfy the need for human interactions. These may not technically be ethical questions, but they will certainly spawn a new set of ethical concerns.”

Smith agrees. “Bias is likely the most concerning ethical consideration for the mortgage industry. Like any technology or coding, AI only knows what it was taught and is exposed to unconscious and inherent biases that we know already exist in ChatGPT. AI is also something that can’t be left to its own devices. Left unchecked, AI used for underwriting, for example, may start to take on undesirable or unethical paths to approved or declined loans.”

As the mortgage industry seeks answers to these problems, many won’t like the answers we come up with. As STRATMOR Senior Partner Garth Graham notes: “If your mortgage company closes two loans per employee per month — and it’s probably a little less than that right now — how much more productive could you be if AI stripped out some of the trust issues our industry deals with each day? Could you be 25 percent more productive then? That means 25 percent of your people will likely be impacted.”

Along with the ethical issues come concerns over the darker side of the technology. For example, every safety check employed to trap email phishing can be eliminated with ChatGPT. Misspellings go away, poor grammar is cleaned up and spoofing addresses makes it look like the emails came from a legitimate source. Lenders have much to face as AI becomes commonplace.

ChatGPT’s confidence aside, there will definitely be more AI in the lending process in the near future. Here are some things Graham looks forward to it being able to do:

All these potential benefits to the industry spring from the same aspect of these advanced technologies, and it is not the ability to automate.

STRATMOR’s consultants identified a great many advantages that AI could potentially offer mortgage lenders, including all of those that ChatGPT provided. But, when the experts were polled something else came to light, something that goes beyond the standard measurable metrics the industry lives by.

Graham explains: “One of the biggest issues in mortgage banking is that the consumer shows up with a bunch of data and nobody believes them. There is no trust in the process.

“The lender asks the borrower for data, then they pay a third party to verify it, but not until after they have asked the borrower to give them the income, verify it with W2s and copies of their tax returns and then recent pay stubs to make sure the borrower has the ‘ability to pay.’ What a mess.

“We spend a ton of time and money trying to convert proof that’s typically provided in the form of images into data we can use,” Graham says. “We then hand that all off to the next person, who does not trust the data either.”

Ultimately, the lender packages up the loan to sell to an investor who doesn’t trust any of the data in the file, and the process starts all over again.

“We don’t trust anything provided by any party that touched the file before we did,” Graham says. “But if we had an AI that could confirm for all parties that the data was correct, we could change all of that. To me, the major opportunity AI offers is removing all the checking, and the checking of checkers that has created an environment where the cost to originate is over $10,000.”

ChatGPT would almost certainly tell us that it’s ready to hold this level of trust from us, but we’re not there just yet. That change, and it will likely occur, will happen very gradually over time. That has little to do with the incredible speed with which AI is taking over the minds of American executives and everything to do with the way our industry invests in technology.

“The industry change with AI will be significant, but it is going to take some time,” says Graham. “Everything in mortgage banking can be explained by two things: cyclicality and fragmentation. Cyclicality means it is very difficult to invest in technology when you’re making a lot of money, because you’re too busy. And in a downcycle you have the time but not the money. Fragmentation is because we have 300,000 people in our industry whose behaviors we are trying to change based on technology investments made — paired up with the three million consumers we are trying to help, and that being spread across 3,000 mortgage companies. That’s a lot of change management.”

While others may wait and see or wish some AI genie could make it easier to start using these new technologies now, there are lenders already in motion.

“In light of the state of AI in the mortgage industry today, lenders would do well to make sure they educate themselves to understand AI and its capabilities so they can have informed conversations with vendors who have chosen to implement AI in their technology,” says Principal Kris van Beever. “In that way, lenders can make better decisions on when and where to exploit this new technology for their benefit.”

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.