Yes, this article mentions AI. Before you scroll past it, stick with me. Because what the 2025 STRATMOR Technology Insight® Study (TIS) Digital Innovations results actually show is not just more AI hype. They show where AI adoption is accelerating and where AI is starting to matter most: in where lenders are deploying technology. And there’s a real shift that turns out to be pretty interesting.

Think of mortgage digital investment as an iceberg. For the better part of a decade, the tip, the visible, borrower-facing portion above the waterline, was where nearly all the energy went. Online applications. Mobile experiences. Status updates. Digital disclosures. And that work was necessary and right: borrowers demanded it, and the industry delivered.

But icebergs have a lot more going on beneath the surface (for my fellow data nerds: roughly 90% of an iceberg’s mass sits below the waterline, hidden from view). And based on what nearly 80 lenders — spanning banks, credit unions, and independent mortgage bankers — told us in the 2025 TIS Digital Innovations survey, the mass of digital opportunity has shifted. The submerged bulk of the iceberg, the processing, closing, and post-closing functions that borrowers never see, is where lenders are now directing their technology investments — and increasingly where AI is making automation newly practical. The iceberg hasn’t grown or shrunk. It has flipped.

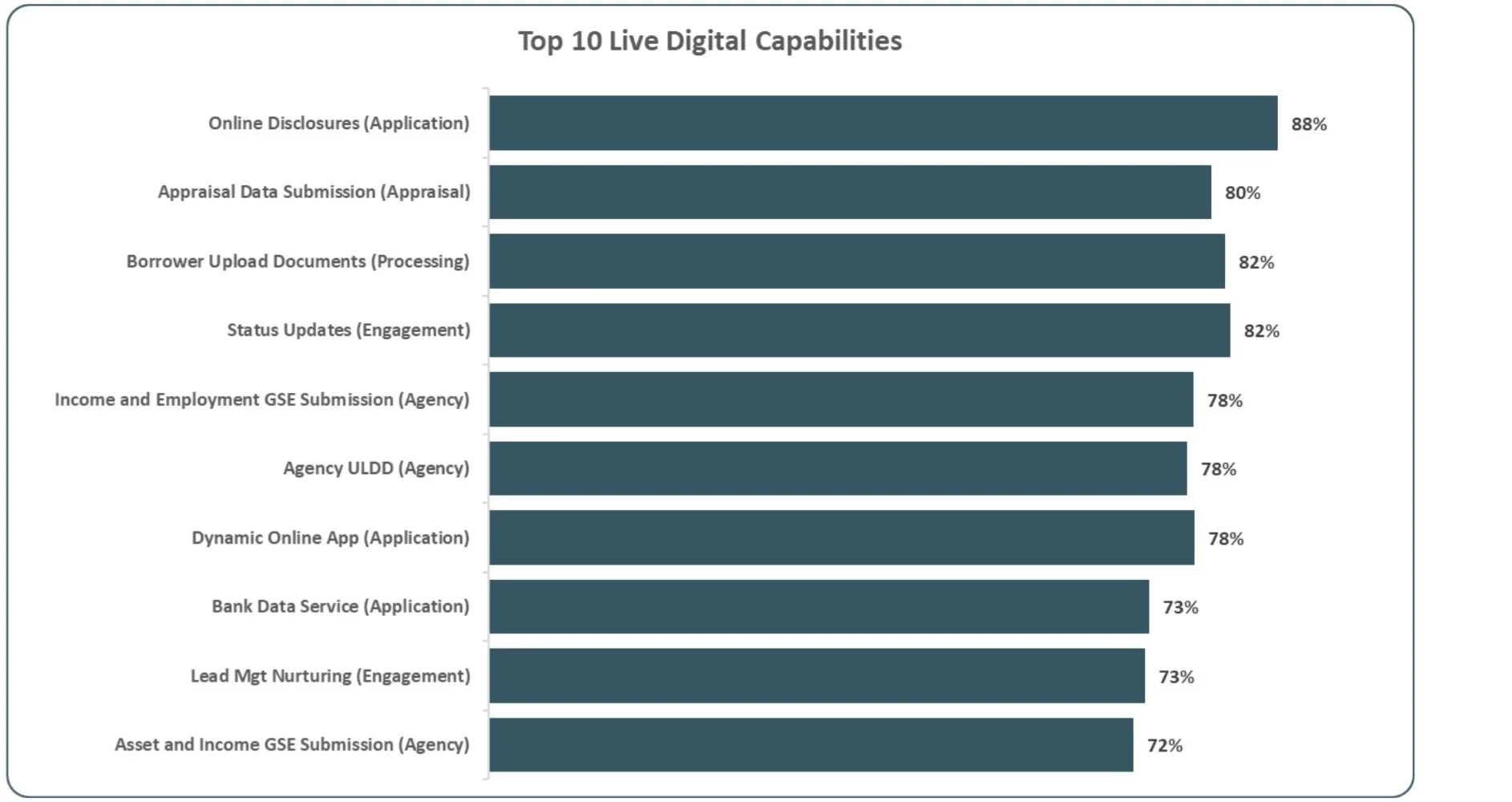

Not long ago, a dynamic online application, mobile-responsive experience, and automated status updates were considered differentiators. Today, they’re simply table stakes. Among this year’s top ten most widely deployed digital capabilities, the list reads like a who’s who of borrower-facing fundamentals: online disclosures, borrower document upload, status updates, and dynamic online applications.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

These aren’t exciting numbers anymore — and that’s the point. Lenders have done the hard work of building out the digital front door. Borrowers now expect a clean online experience, and the industry has largely delivered. The tip of the iceberg is largely above water.

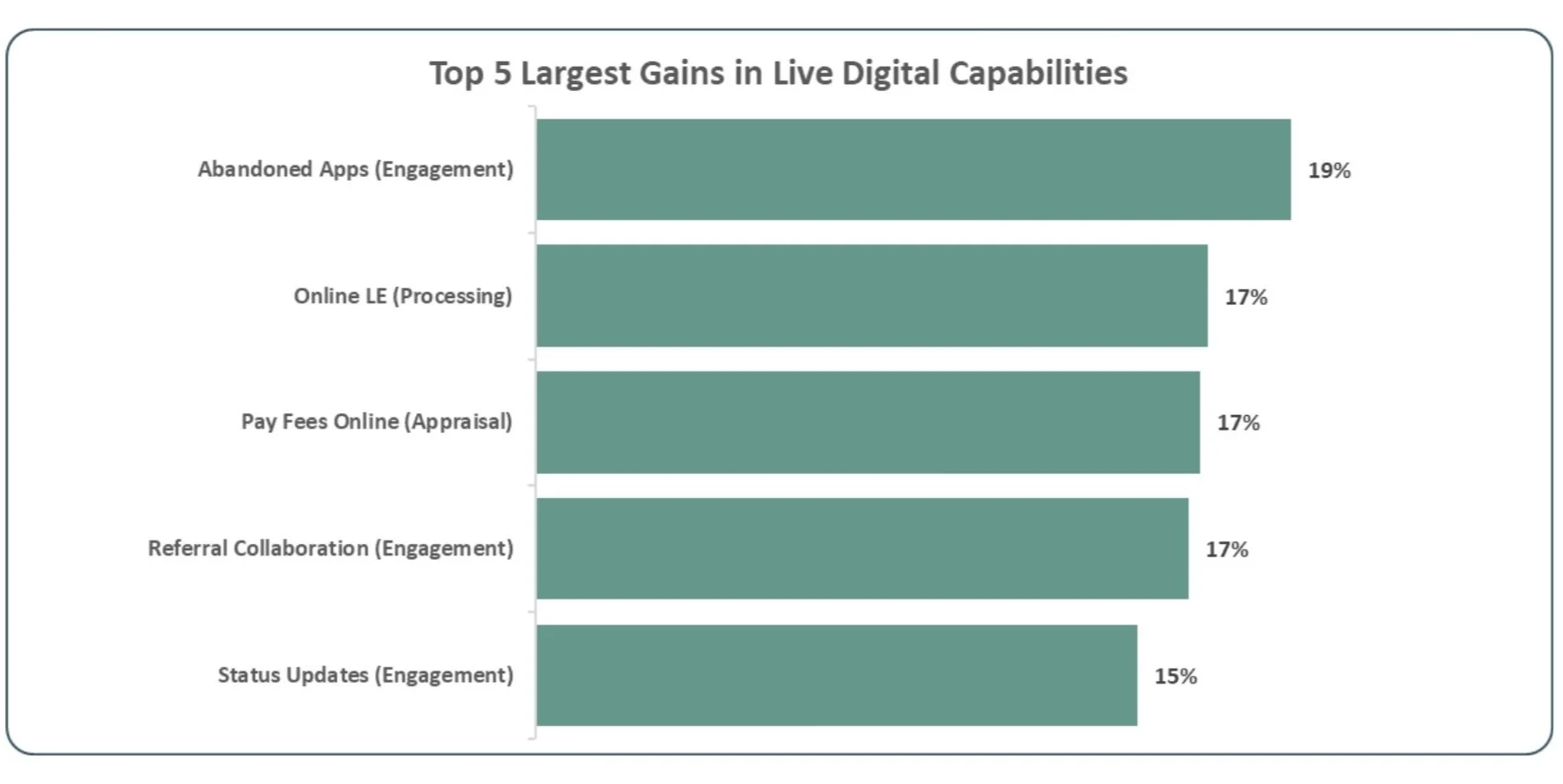

Even as fulfillment capabilities attract increasing investment, the biggest year-over-year adoption gains in 2025 were concentrated at the front end of the process.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

Abandoned application recovery (+19%), online loan estimates (+17%), online appraisal fee payment (+17%), and referral collaboration tools (+17%) topped the list. Lenders are still plugging gaps in the borrower journey, particularly around pull-through and engagement during the early stages of the application.

This isn’t a contradiction. It simply reflects that different lenders are at different stages. Those who have already built out the borrower experience are now looking toward the fulfillment side. Lenders still catching up on the front end made the most visible gains in 2025. The more revealing story for 2026 and beyond, though, is what lenders are putting on their roadmaps. And that’s where the narrative shifts.

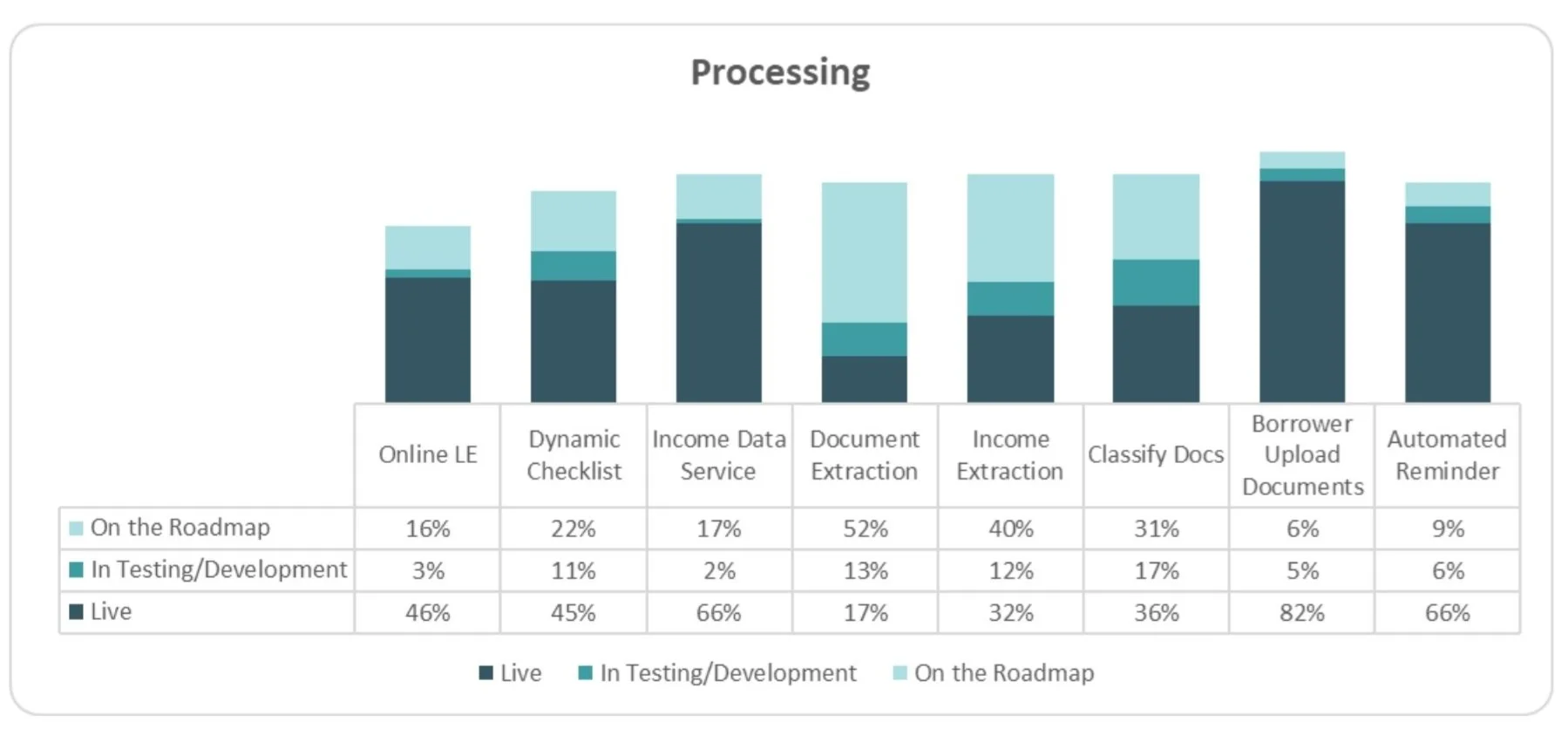

When we look at what lenders say is in testing or on the roadmap — not yet live, but coming — a distinct pattern emerges. The capabilities with the largest pipeline of planned investment are concentrated in processing, closing, and post-closing functions. These represent the submerged part of the iceberg: invisible to borrowers, but where the real mass of operational opportunity now sits, and where AI is beginning to move from concept to practical application.

In processing, document extraction (65%), income extraction (52%), and document classification (48%) top the list of planned investments. These have historically been labor-intensive and underserved by technology. A processor manually stacking and loading documents into a system is not yet a thing of the past. But that’s beginning to change.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

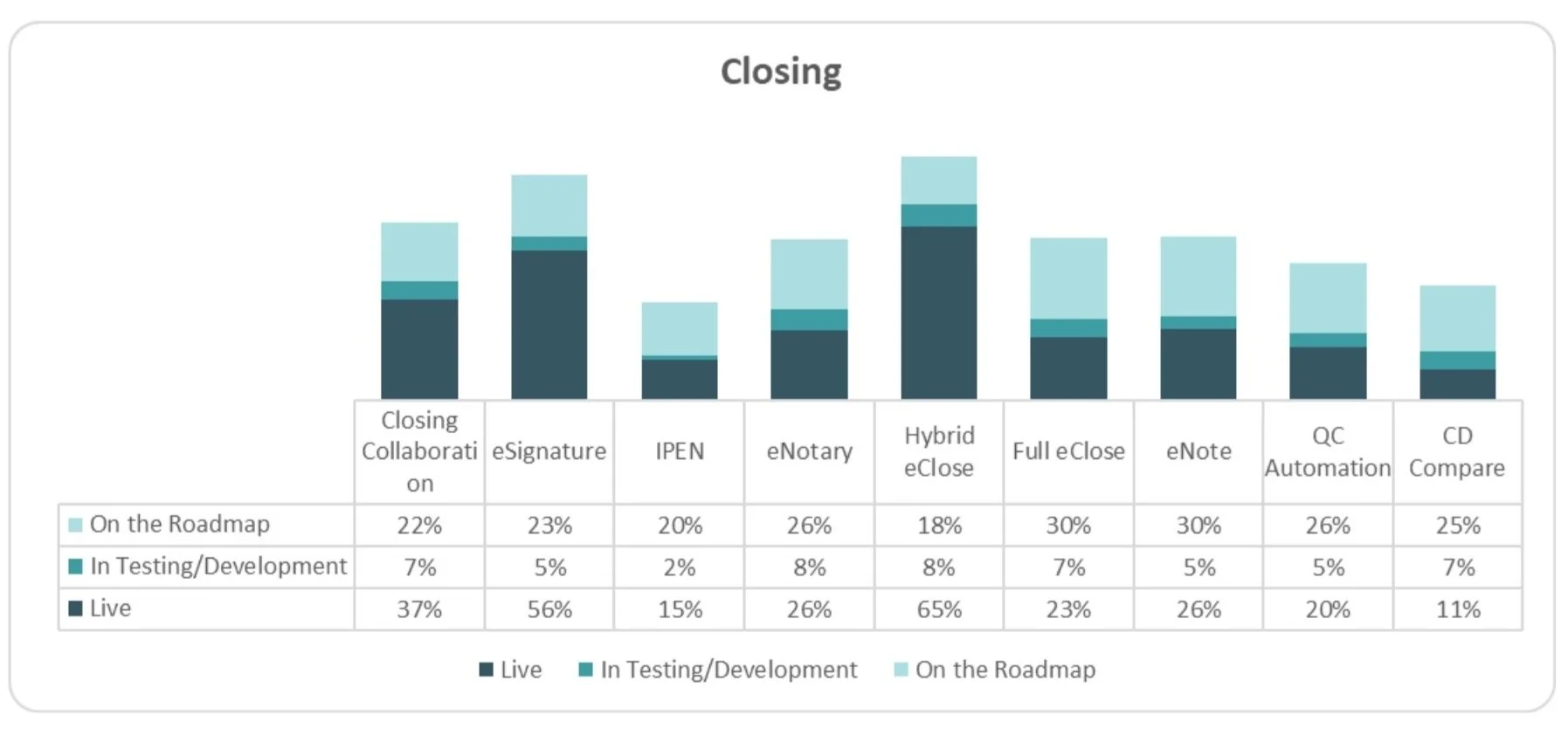

In Closing, full eClose and eNote each show roughly 36% of lenders with planned investment in the pipeline, while QC automation and CD Compare are on the roadmap for roughly a quarter of respondents. These are precisely the kinds of back-office, human-intensive tasks that AI is now making automatable.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

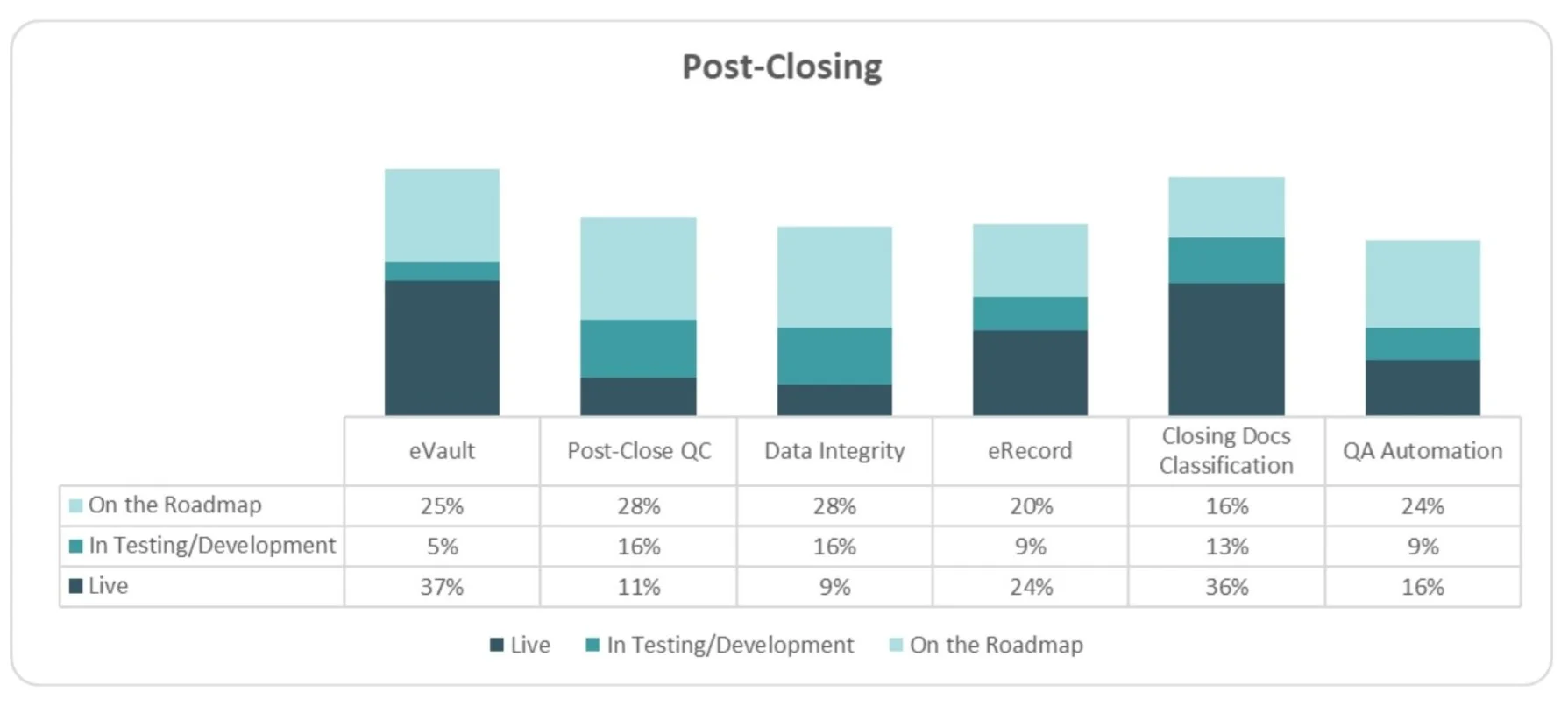

In post-closing, data integrity automation and post-close QC both have 44% of lenders either actively testing or on the roadmap, while only 9–11% are currently live. That gap between planned and deployed is telling. Lenders aren’t ignoring these capabilities; they’re preparing to build them.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

What makes this moment different from prior years when these same capabilities were discussed and largely deferred? The honest answer is AI. The capabilities that lenders are putting on their roadmaps are ones where machine learning has materially improved the feasibility of automated execution. Classifying a pay stub versus a tax return versus a gift letter accurately at scale was hard before. It’s much more achievable now.

For lenders evaluating which back-office capabilities to prioritize. Start with the capabilities that touch your highest-volume, highest-error-rate workflows. Document classification and automated QC tend to deliver the fastest measurable ROI because they reduce touches on every loan, not just edge cases. If your team is still manually sorting and indexing closing packages, that’s a strong first target. The technology is ready; the main variable is implementation discipline.

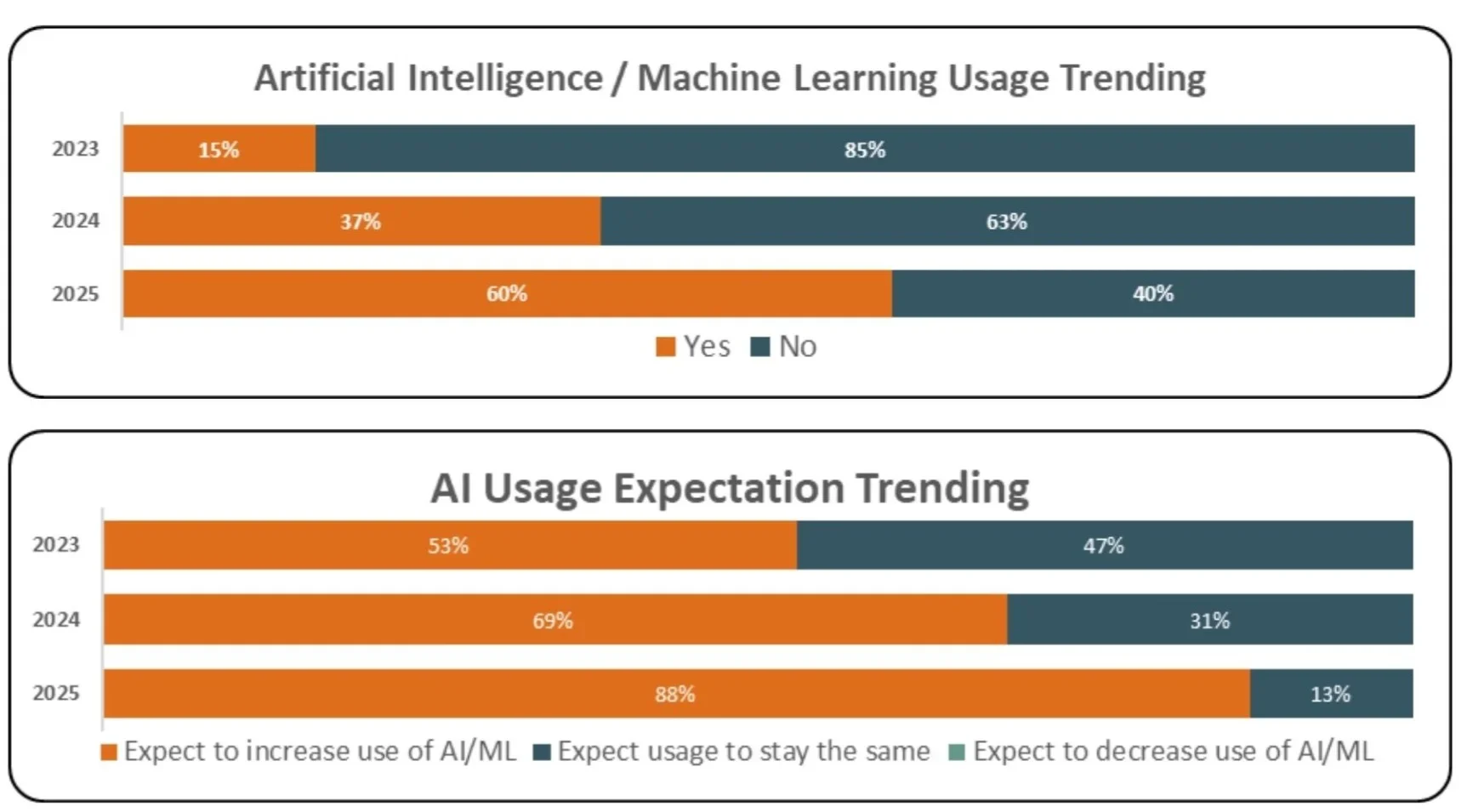

The acceleration in AI and machine learning usage among lenders is not a projection — it’s already showing up in the data. And 88% of current AI users expect to increase their use in the coming year, with precisely zero reporting interest in decreasing it. That’s more than momentum; it reflects conviction.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

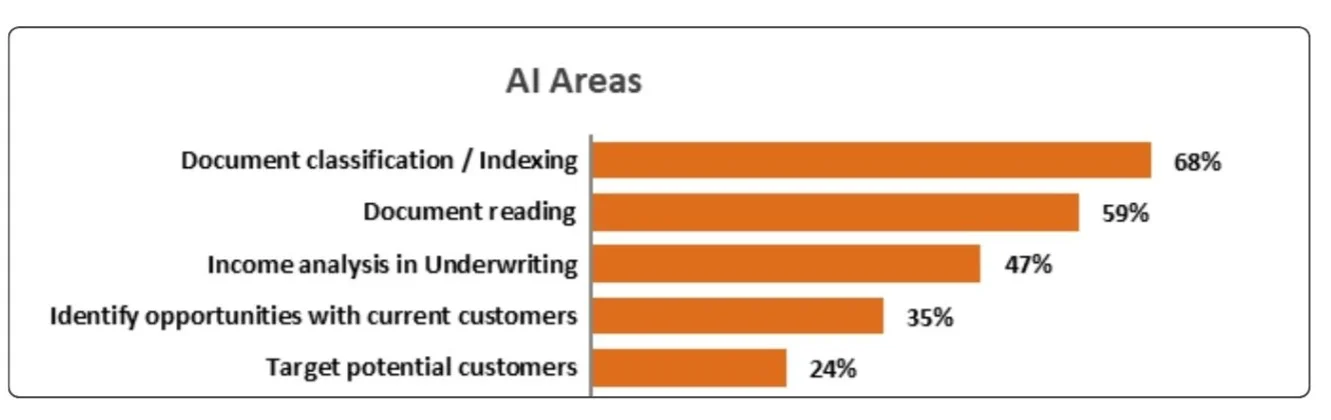

Where are lenders using AI today? Document classification and indexing (68%) and document reading (59%) are the clear leaders. These are back-office functions, not borrower-facing ones. Income analysis in underwriting comes in third at 47%. The front-end use cases are present but clearly secondary.

How lenders are sourcing their AI is also shifting. Early adoption leaned heavily on whatever capabilities were native to the LOS. That’s now down to just 6% of AI-using lenders. The majority, 53%, are going to third-party vendors for purpose-built AI solutions, while 41% are using open-source AI tools with internal resources. The implication: lenders aren’t waiting for their LOS provider to catch up. They’re sourcing AI capability independently, which means the LOS market will face increasing pressure to accelerate its own AI roadmap.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

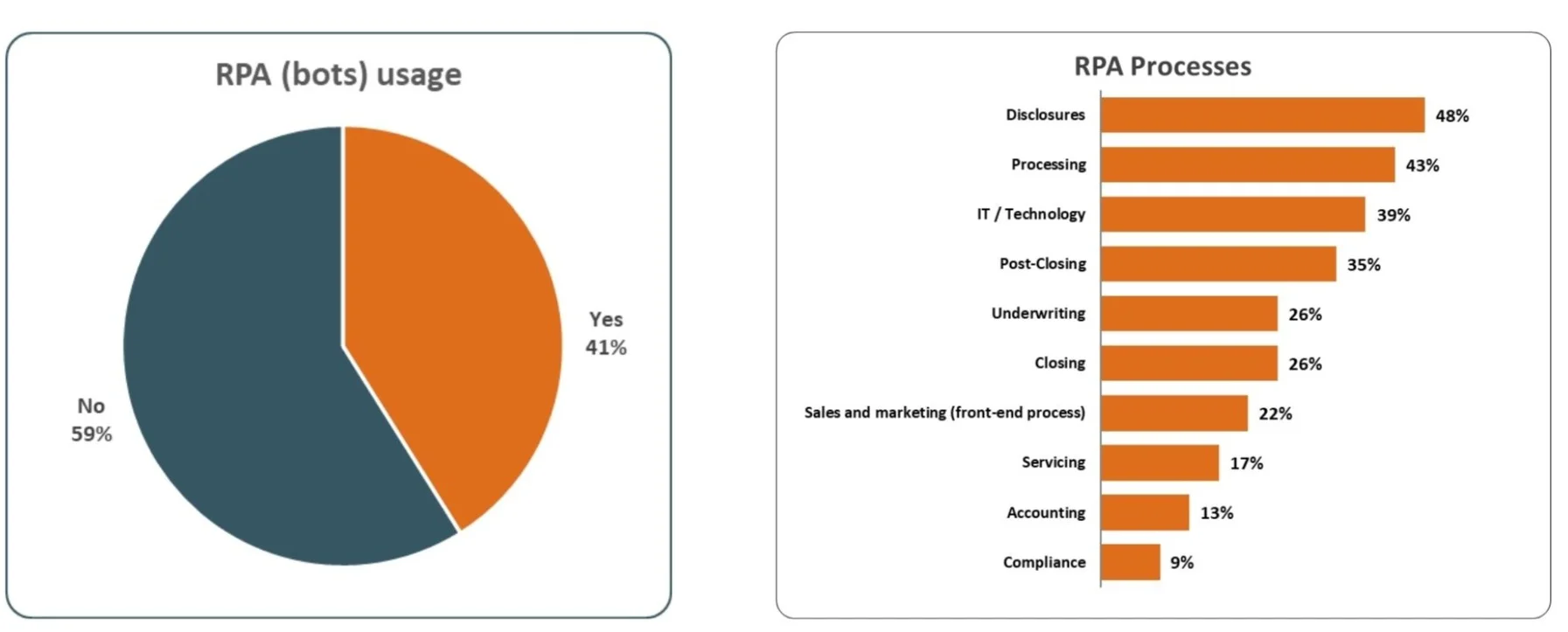

While AI use is growing, robotic process automation (RPA) — the script-based bots that automate defined, repetitive keystroke sequences — is holding steady at just over 40% of lenders using them. That’s roughly where it’s been for the past two years. Usage is concentrated in disclosures (48%), processing (43%), IT/technology functions (39%), and post-closing (35%).

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

Bots have been effective tools, but they come with real limitations. They’re brittle. A system update or interface change can break a bot’s functionality, requiring constant maintenance and rework. Unlike AI, bots don’t learn or adapt; they execute a fixed script. And increasingly, the LOS itself is absorbing some of what bots used to handle, leading a subset of lenders to reduce or discontinue their RPA programs. Among lenders planning to decrease bot usage, the top reason cited is that the LOS now offers native automations.

Bots represent an earlier generation of automation, one that served lenders well during a period when LOS platforms lacked many native capabilities they needed, but that is increasingly being supplanted by more intelligent, integrated alternatives. The progression from bots to LOS-native automation to AI reflects a maturing technology stack, not a failed experiment.

The case for focusing AI investment on back-office, non-borrower-facing functions is more nuanced than it might appear.

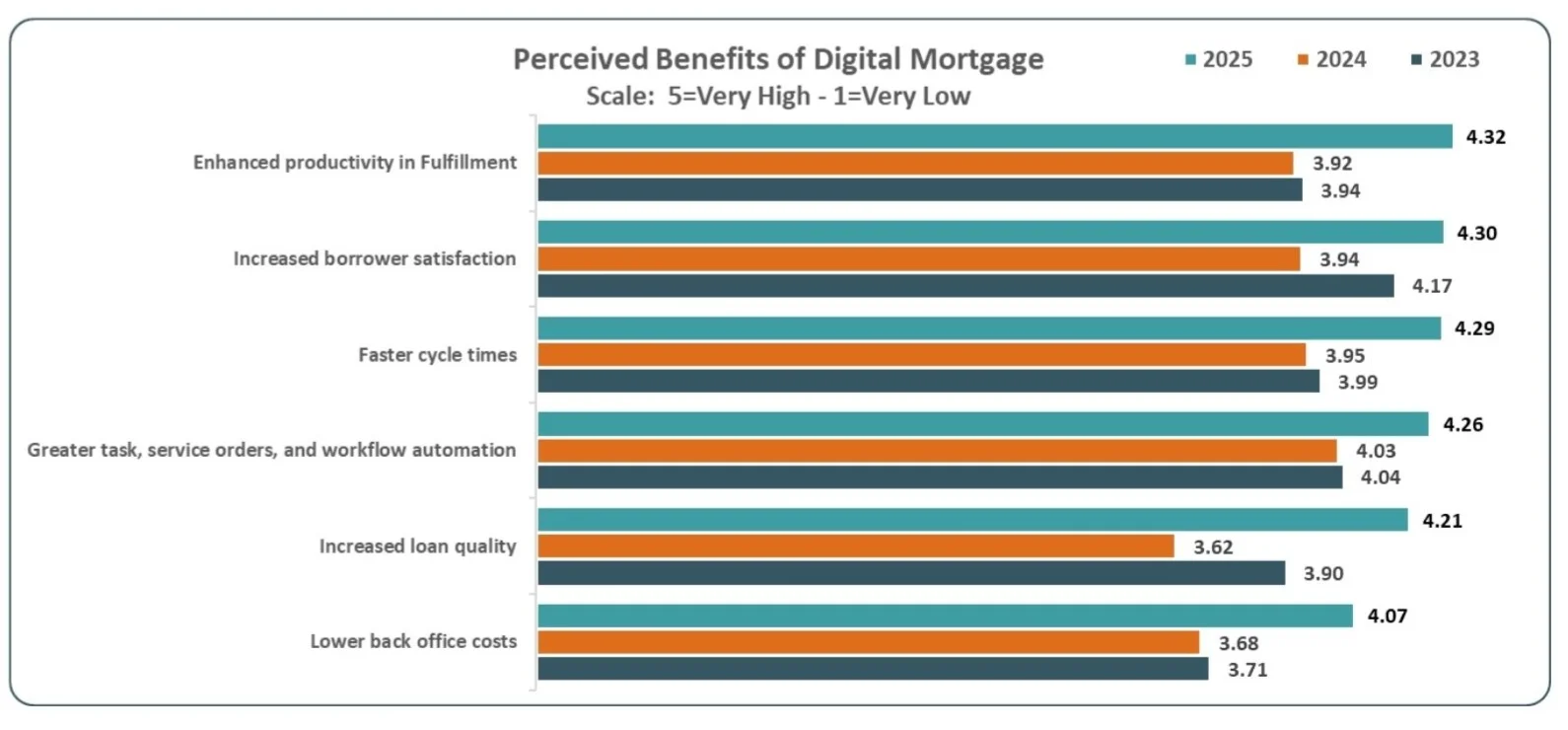

The benefits lenders perceive from digital investment have risen consistently over the past three years. Enhanced productivity in fulfillment now scores 4.32 out of 5, up from 3.94 in 2023. And notably, increased loan quality — a category that rarely cracked the top of this list in prior years — now scores 4.21. Lenders believe the new generation of AI-enabled QC and document tools is delivering more accurate files, fewer post-close exceptions, and fewer downstream issues with investors and agencies.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

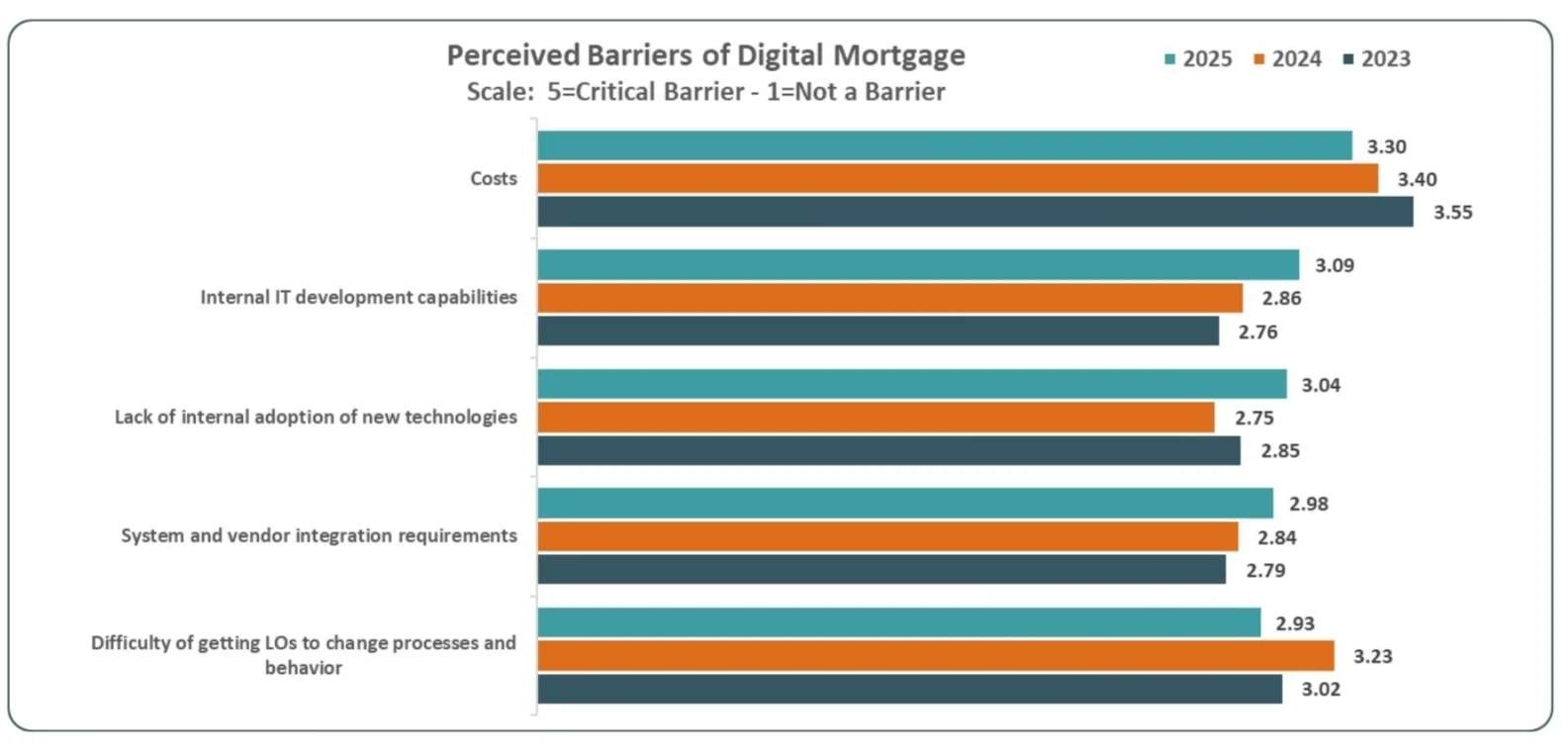

But cost remains the dominant barrier, rating 3.30 on a 5-point critical barrier scale. Internal IT development capabilities and lack of internal adoption of new technologies are close behind. The gap between what lenders believe digital can do and what they can afford to implement — and get their people to actually use — is real and persistent.

Source: STRATMOR 2025 Technology Insight® Study Digital Innovations Results

Adoption, in particular, deserves emphasis. Paying for an automated income analysis tool and then having underwriters re-underwrite the loan anyway is essentially paying twice for the same result. Getting people to genuinely trust AI-generated recommendations takes time, experience, and evidence. Capabilities that bypass that human trust-building hurdle have an inherent ROI advantage in the near term.

The cost barrier is real, but it’s worth reframing. The question isn’t whether back-office AI is expensive in absolute terms, but whether it’s more expensive than the status quo. Manual document review, post-close QC errors, and investor repurchase demands all carry their own costs. Lenders who have built the business case with that full picture in mind tend to find the ROI math considerably more compelling than those who are comparing technology spend to zero.

The 2025 STRATMOR TIS data tells the story of a maturing industry navigating a technology transition. The tip of the digital iceberg — the borrower-facing front end — has been substantially built. The gains now, in both productivity and loan quality, are more likely to come from what’s below the waterline: automating what happens after the application is submitted, in the parts of the process borrowers never see but lenders feel every day. And increasingly, AI is what makes that next wave of automation feasible.

Based on the data, the STRATMOR team is watching for the following in 2026:

Digital is no longer an innovation initiative. It’s foundational to how lenders operate. The question in 2026 isn’t whether to invest in digital, but where those investments will deliver the greatest operational and financial return.

The iceberg has flipped. The opportunity is underwater. Time to dive in.

For lenders, the challenge now is prioritization. Which workflows are mature enough for automation today? Which technologies are ready for enterprise-scale deployment? And where can AI deliver measurable gains in productivity, loan quality, and scalability without introducing unnecessary operational risk?

That’s where STRATMOR comes in. We work with lenders across the mortgage industry to assess digital readiness, evaluate technology investments, and build implementation roadmaps grounded in data — and we’re ready to help your team succeed.

Nicole Yung is a Senior Partner at STRATMOR Group specializing in mortgage technology research and advisory. The data in this article is drawn from the 2025 STRATMOR Technology Insight® Study, Digital Innovations module, which surveyed nearly 80 lenders across bank, credit union, and independent mortgage banker segments.

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.