Good planning and preparation are key components to success. Each enable us to act intentionally and in a timely manner when required. Looking back over our long history in the mortgage business, we see numerous examples of well-executed plans. 2022 was difficult, at best, for residential mortgage companies to prepare for and develop their annual plans. It is turning out far differently than most expected.

The questions many lenders face today:

In this article we will consider the last question and provide some strategic advice for lenders who are ready to learn more about the process or are ready to contemplate, evaluate or even pursue an exit strategy.

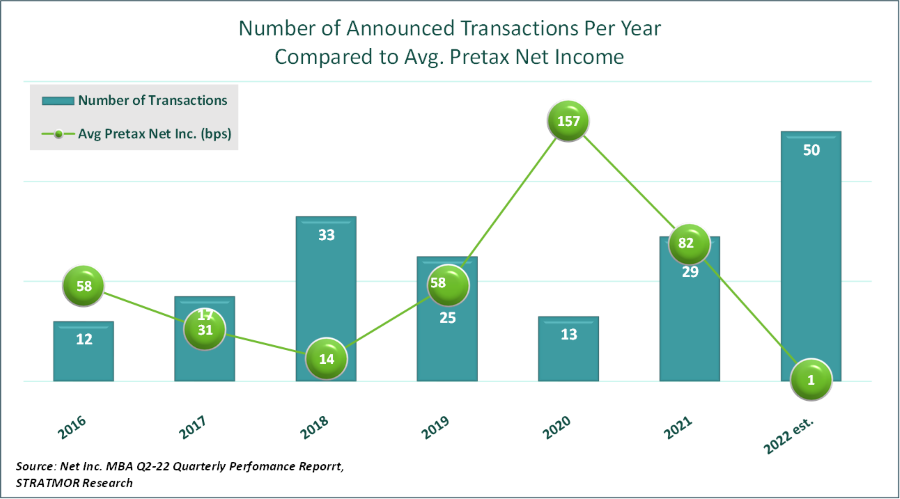

By the end of 2022, we anticipate that nearly 50 merger or acquisition (M&A) transactions will be announced or closed. That is 50% more transactions than 2018, the next highest year of lender consolidations in the past three decades. The increased M&A activity to-date has been fueled primarily by two factors: 1) pent-up demand for retirement by aged owners who achieved lifetime net worth objectives and 2) the current industry challenges with more storm clouds on the horizon. While 50 is a small fraction of the total number of residential lenders, these transactions have already had an impact on the industry. All signs are pointing toward a robust M&A market in 2023 as well, and our August Insights Report on strategies for lenders in the down cycle included M&A strategies that lenders can leverage in response.

Those who sold mortgage companies in the past decade benefitted from a lending environment that provided a decent amount of cushion relative to execution results. In the past, predicting post deal profitability was largely a matter of reviewing volume projections. If volume projections were close, most M&A deals made financial sense. Some level of mistakes relative to transaction assumptions, model matching or culture alignment were able to be absorbed without undermining the net benefits of the deal.

Those days are over. Today, there is little margin for error in these deals, which is prompting both buyers (and sellers) to be even more methodical. Today, with profits diminishing, sellers are having to work harder and smarter to attract the right buyers.

A sage general counsel from a previous employer once said to me: “If you want a transaction badly, that’s how you will get it: badly.” Today, a transaction must make financial sense, include well-matched parties, have meaningful synergies AND, must make life better for the sales staff, the operations staff and the corporate services staff that will remain. These deals exist, and if the buyer and seller don’t clearly view it as a “win-win” then there will likely not be a winner for either party.

While there are many examples of successful M&A transactions, skepticism among the parties remain. That is a good thing. Blind ambitions, wishful thinking and lax due diligence — from buyers or sellers — leads to failed transactions. At STRATMOR, we encourage buyers and sellers to clearly understand their objectives before entering the process, to share those objectives openly with each other and to remain disciplined.

A well aligned and matched (culture and model) transaction frequently results in transaction synergies that total 30 – 50 basis points (bps). Meaning, a lender that is operating at a 10 bps loss, has an opportunity to align with another firm and convert the bottom-line performance to a 20 – 40 bps profit. Well-matched relationships can and should result in a “one plus one equals three” transaction.

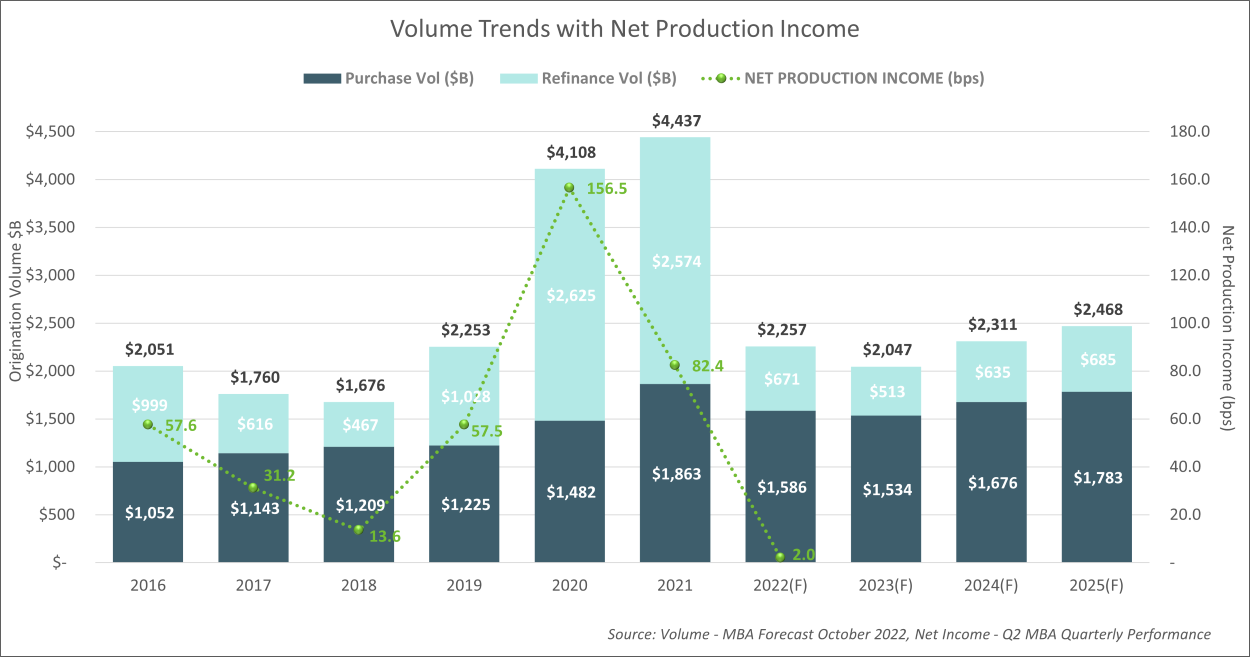

The data helps tell the story. According to the Mortgage Bankers Association’s full year financial forecast for 2022, Independent Mortgage Banker (IMB) average performance is breakeven, at best. Volume is predicted to be down 50 percent from 2021 levels and 2023 projections are down a bit more.

Net production income is trending towards its lowest point since 2018, as noted in the chart below. The expectation of continued margin compression in 2023 and 2024 has resulted in the onset of industry consolidation.

Chart 1

Also, according to the Bureau of Labor Statistics, our industry employed 427,000 employees in March of this year. Given the loan volume forecast details above, the number of companies and employees in the industry will no doubt look very different this time next year.

Despite this, buyers are active in today’s market and prepared to pay reasonable upfront premiums for well-matched opportunities.

STRATMOR has been pointing to increased M&A activity for over a year now and, in fact, that’s exactly what we are seeing in the market now.

Chart 2

The buyer motivations that we highlighted in September 2021 are still factors in today’s market, but none more important than transaction synergies. The difference, again, between today’s market and the M&A environment of prior ten years is that buyers know synergy is not a like-to-have. It’s a must have. They know that a deal that doesn’t include relevant and quantifiable synergies is not worth the risk. And change without tangible benefits for the seller’s employees is simply noise which inevitably causes employees to leave.

For more on the synergy aspect, listen in to this podcast interview with Senior Partner Garth Graham and Christine Stuart of the Mortgage News Network.

A sure way to drain value out of an M&A event is to combine two firms that do not match up culturally. Of all the things that can go wrong during one of these complex transactions, a cultural mismatch is the most damaging aspect to post-deal value.

STRATMOR has spoken in other Insights Reports about the specific steps lenders can take to prepare for an M&A event, whether buying or selling. Now that we are experiencing consolidation, it’s important that lenders know how to objectively define their corporate culture and how it differs from others. This is a helpful exercise even if a lender chooses not to contemplate an exit strategy

While every lending institution is unique, we have found that there are three broad corporate cultures into which mortgage lenders generally fall. Well-matched buyers and sellers are those that occupy the same “swim lanes” as outlined below.

Structuring deals between companies in the same swim lane is crucial for success. Combining firms that approach the business differently is a recipe for disaster.

Because cultural alignment is one of the most important ingredients relative to transaction success, you must not only understand which swim lane you occupy, but also the many related nuisances — good and bad — that make up your corporate culture.

STRATMOR works with both buyers and sellers to help them determine which industry players have the potential to make good partners. As part of that work, we have created a pre-meeting questionnaire that helps buyers and sellers know what they are bringing to the table. Specifically, it helps all parties involved understand:

The decision to sell is not easy. The firm represents an owner’s life work and frequently represents something more significant than just their financial net worth; it also represents how they assess their personal self-worth.

As such, selling is also an emotional decision. The decision will have an impact on the company owner, his / her family and each of the employees. The responsibility that an owner feels for others is normal and admirable. However, extending the decision “just a little longer,” could mean burning through assets that could have otherwise been retained or applied toward improving the transaction.

Thoughtful lenders will begin this deliberation by thinking clearly through their objectives. This will include a transparent review of the company’s strengths and weaknesses. We have never met an owner who did not feel like their own DNA was in the businesses they had built. They are sensitive and prideful, and with good reason. This makes them vulnerable.

The need for confidentiality also brings vulnerability to this process. Even the prospect of selling can have adverse consequences for their ongoing business. The circle of trusted advisors must be small.

This is exactly why STRATMOR conversations are conducted privately, under an NDA, in safe environments that allow us to guide owners through the process objectively. Our approach to M&A consulting is based on full confidentiality and the safe exchange of information. That has been the case for the 38 years we have been advising the mortgage industry.

It is a good idea for lenders to always be evaluating their options, and a good advisor can lead a lender through the process to ensure that everything important is taken into consideration. It is never too late to take a data-driven assessment of your company’s market position. Identifying levers that could improve your market value now, will serve you well regardless of your decision on if, or when, to exit.

Under the best of circumstances, M&A is a complex and risky endeavor. While it can result in great gains for all involved, even if everything does line up, there are a million ways it can go wrong. This market is very different from any market than we’ve seen before and leaning on your own past approaches and experiences may not be the best strategy. Instead, consider working with a consultant that knows the mortgage M&A business and understands that you want to do the right thing to support your staff and protect your hard-earned assets.

When you’re ready to start the conversation, look to STRATMOR. No other consulting firm in the mortgage industry has access to the level of industry data we possess or the relationships we enjoy in this space. Both of these invaluable assets help us define cultural alignment, model matches, and quantifiable synergies and deal terms. We can help you determine what your culture really says about your company and help you find a match that will lead to the best possible outcome for all parties involved.

Now is the time to entertain these considerations. With buyers lined up and looking for their next opportunity, this may be the best environment owners will see for years. Hrobon

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.