In today’s market, mortgage lenders are facing a challenge: they are not making enough money on originations to sustain their organizations. When your company is losing money on each loan you originate and the only revenue comes from the servicing rights, developing an effective servicing strategy becomes a mission critical priority.

This is the position many lenders find themselves in now, which is why they are calling STRATMOR Group for help in formulating a sustainable servicing strategy. Today, that strategy revolves around Mortgage Servicing Rights (MSRs).

The question lenders need to answer now is what to do with the servicing assets when they sell off their production. This involves two important decisions:

Each of these decisions comes with its own consequences, in terms of dollars spent, who owns the customer and borrower satisfaction. Determining which path makes the most sense can be difficult without objective data on the industry, the current value of the servicing assets and expected loan performance based on a review of peer data.

As a consultancy with a great deal of experience in the mortgage servicing business and access to the largest pool of servicing peer data in the industry, we are often called upon to help lenders work through this MSR decision-making process as well as the implementation of the chosen strategy.

In this article, we’ll consider these questions, our approach to solving them and discuss the complexities of effective servicing transfers.

The lender has several options available for the servicing of their loans, and the decision is not necessarily an easy one for the lender to make. We guide the lender through a discussion that touches on each of the following elements to prepare them for the decision:

When STRATMOR is called in to assist client executive teams, we use a fact-driven analysis, based on our experience in the market, as well as data from the PGR: MBA and STRATMOR Peer Group Roundtable program.

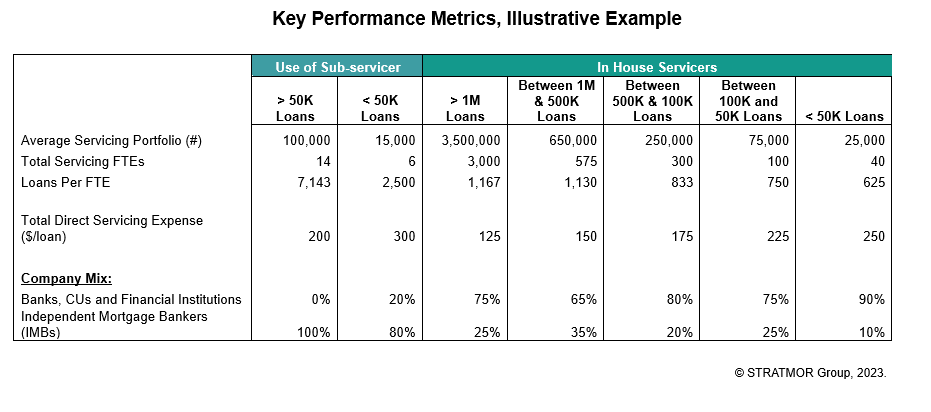

The table below uses illustrative data only and is intended to show a rough approximation of industry averages. Note that the data shows a continuum of key full-time-employee (FTE) and servicing cost metrics across servicing portfolio strata and summarizes the mix between banks and IMBs as an additional dimension.

Chart 1

Whether lenders use a sub-servicer or service in house, STRATMOR has actual Direct Servicing Expense and Loans per FTE data across various portfolio size strata. By leveraging this cost and productivity data, we can advise clients as to the likely cost to service and personnel needs as they scale up their portfolio. For example, let’s assume we have a lender with the following characteristics:

Based on the illustrative table above, we can show that in-house servicers with a portfolio size in the range of 50,000 to 100,000 loans average $225/loan. If this lender moved to an in-house model and STRATMOR worked with them to drive their cost down to the peer average of $225/loan, the savings would add up to $3 million a year.

While the decision to move servicing in house is often driven by the potential financial benefits, there are other important non-financial considerations such as customer experience and relationship deepening potential that are crucial to the decision.

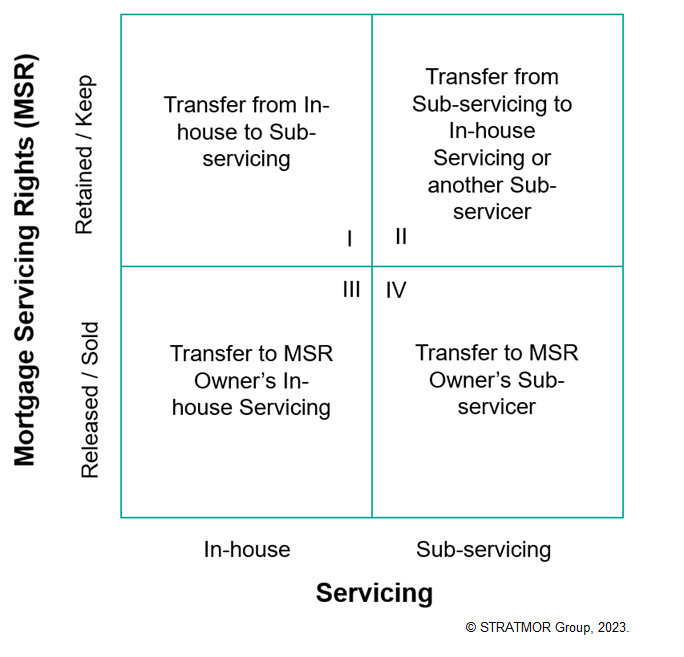

In addition to financial analysis, STRATMOR employs a servicing quadrant analysis model.

The quadrants in our model focus on the benefits and considerations inherent in each approach to the servicing asset, including risk mitigation, liquidity management, operational simplicity, and more.

The diagram below illustrates the model.

Chart 2

The result of this analysis will determine into which quadrant of our servicing transfer model the lender’s business currently falls and the benefits and disadvantages presented by the decision to move into another quadrant. For example, we can point to similar companies and use them as benchmarks to predict how a client might perform if they choose to operate within the same quadrant as their peers.

If the lender decides to shift its business into a new quadrant, STRATMOR assists with the financial, technical and operational analysis to give the lender the best opportunity to succeed. If the lender chooses to bring servicing in-house, we can help them staff up, choose the right technology and then launch their new in-house servicing operations.

Much of our work is in helping lenders accurately assess the tradeoffs between what they would earn pursuing different strategies. For one lender, it may well be worth investing millions in a new servicing operation to overcome a sub-servicer’s poor customer service, and the lost business that results from it. Another management team may opt to find a new sub-servicer rather than take on the increased cost of compliance and default servicing involved in bringing that work in-house.

In many cases, servicing will be transferred, either back in-house, to a sub-servicer or to a new MSR investor. This is a critical part of the process and one in which STRATMOR is well qualified to provide assistance.

In this section, we take a more detailed look at the various options for MSR ownership and the expected performance of the actual loan servicing under each of the four common approaches as noted in the quadrant illustration above.

On the y-axis, we consider the lender’s decision to retain servicing or release it by selling it off after originating the loan. The x-axis identifies whether loan servicing will be conducted in-house or is subcontracted to one of the companies providing specialized servicing capabilities.

Here, we only provide an overview of some of the advantages and costs/risks associated with each quadrant. Lenders are urged to perform a complete analysis of their current business, future goals and capabilities before switching to another quadrant. STRATMOR often assists clients in this analysis.

Quadrant I — MSR Retained / In-house Servicing

If the lender keeps the servicing in-house, they will take on the management of all aspects of loan servicing, rather than outsource it to a third-party sub-servicer. These tasks typically include collecting and remitting loan payments, managing escrow accounts for taxes and insurance, addressing delinquencies, and any other responsibilities stipulated in the mortgage agreement.

The primary advantage of keeping the servicing in-house is direct control over the quality of customer service and all customer interactions. This can be valuable for building and maintaining strong customer relationships, and it allows the institution to earn the servicing fees associated with the loan directly.

However, this strategy also means that the institution bears the full responsibility for regulatory compliance, operational management, and the associated costs and risks of servicing. This can be expensive.

Quadrant II — MSR Retained / Sub-servicing

Retaining the servicing rights through partnership with a sub-servicer means not selling the rights to service the mortgage after originating the loan, but also not servicing those loans in-house.

In this arrangement, the original institution retains ownership of the MSR and thus the broader relationship with the customer, but it delegates the day-to-day operational tasks of loan servicing to the sub-servicer. These tasks typically include collecting and remitting loan payments, managing escrow accounts for taxes and insurance, addressing delinquencies, and any other responsibilities stipulated in the mortgage agreement.

The primary advantage of retaining MSRs with sub-servicing is that the institution can capitalize on the specialized expertise and operational efficiencies of the sub-servicer while still benefiting from the value of the MSR.

This approach can be especially beneficial for entities that want to remain in the servicing space but lack the infrastructure, technology, or desire to manage daily servicing operations. However, it requires the lender to maintain effective oversight of the sub-servicer to ensure compliance, service quality, and adherence to the terms of their agreement.

While sub-servicing offers numerous benefits, institutions must conduct due diligence when selecting a sub-servicer. The quality of service, technological capabilities, financial stability, and reputation of the sub-servicer can significantly impact the benefits realized.

Quadrant III — MSR Released / In-house Servicing

This quadrant is for lenders who choose to sell or transfer the servicing rights to another entity. Once released, the selling entity no longer holds the rights to service the mortgage. When a lender opts for this “servicing released” approach, it means both the loan and the servicing rights are sold off, though they need not be sold to the same party.

The benefits of this strategy include immediate capital recovery, risk mitigation, operational simplicity, reduced overhead, regulatory and compliance relief, reduced delinquency concern, and flexibility in market participation. And there may be other benefits.

While there are clear benefits to the popular “servicing released” approach, this strategy means forgoing the long-term revenue stream associated with servicing fees.

Quadrant IV — MSR Released / Sub-servicing

If an institution buys MSR rights for loans it did not originate and then contracts with a sub-servicer to service those loans, it falls into this fourth quadrant.

In this scenario, the entity that purchases the MSR holds the rights to the financial benefits associated with servicing the loan. However, the day-to-day operational tasks related to the loan — such as collecting and remitting loan payments, managing escrow accounts for taxes and insurance, handling customer communications, and addressing delinquencies — are outsourced to the sub-servicer.

The advantage of this strategy for the MSR purchaser is the ability to capitalize on the revenue streams associated with the MSR without the operational burdens of daily servicing. This is particularly beneficial if the purchasing entity lacks the infrastructure or resources for in-house servicing.

However, as with any sub-servicing arrangement, it’s crucial for the MSR owner to maintain diligent oversight of the sub-servicer to ensure compliance, service quality, and alignment with the agreed-upon terms. The regulatory responsibility of a master servicer is not avoided by using a sub-servicer.

For the lender, this is not significantly different than quadrant three. The only difference is the party that receives the loan data from the originator.

Any change the lender makes in its business that involves the servicing asset is likely to involve servicing transfers, and this is where lenders are challenged in executing their new strategy. Understanding the cyclical nature of the mortgage industry is a crucial part of the intricate relationship between servicing transfers and broader mortgage market conditions. Without seasoned guidance, the transfer process can be more complex than many believe and can lead to significant operational and technology challenges.

It can be helpful to consider the following as an introduction to the complex process of servicing transfers.

In essence, acquiring MSR portfolios and managing the transfer of servicing is like performing a carefully choreographed dance involving financial, operational, and customer relationship management maneuvers. Each step must be executed with precision to ensure a seamless transition and to maintain trust in the mortgage ecosystem.

Imagine a passenger ship, steaming along in the night. Now imagine changing the crew of that ship without stopping the vessel or disturbing the passengers. That’s akin to the process of transitioning from one sub-servicer to another.

To effectively manage this complex dance of coordination, data management, and communication, STRATMOR’s Transfer of Servicing Methodology (process, procedures, tools, templates, etc.) helps lenders move through the following project phases.

Initial Consideration and Decision Phase

The journey often begins with the need to switch sub-servicers. The reasons to switch include cost concerns, service quality issues, technological deficiencies and strategic shifts, among others. Once the decision to switch is made, it is important to review the current contract with the existing sub-servicer to understand any stipulations, penalties, or timelines associated with ending the relationship.

Selection of the New Sub-servicer

Identifying and engaging a new sub-servicer should include a thorough sub-servicer assessment and due diligence to determine the prospective sub-servicer’s capabilities, technological infrastructure, service quality, and financial stability. When a suitable partner is identified, the contract negotiations to set the terms of the new relationship can begin.

Planning and Coordination

Transitioning between sub-servicers is a process that requires a clear roadmap and playbook documenting the steps taken to ensure continuity of servicing during a servicing transfer as required by CFPB. Both the current and the new sub-servicer must come together to draft a transition plan and detail how risks will be managed and what actions will be taken to mitigate customer impact. This plan will detail the data to be transferred, the format, timelines, and responsibilities.

Communication with Customers

One of the most critical aspects of the transition is managing customer communication. This communication needs to be clear, timely, repetitive, and reassuring to prevent any panic or confusion. Customer need to be informed about the change in sub-servicers and be told what it means for them and any actions they may need to take, such as updating payment details.

Data Transition

The data transfer is at the center of the change process. Moving vast amounts of sensitive information — payment histories, personal customer details, escrow data, and more — from one platform to another is a monumental task. This transfer must be secure, accurate, and swift to ensure continuity of servicing.

The servicing instructions should define the SLAs for transferor and transferee as well as the method for exchanging information (data & images), system set up, data mapping, and communication requirements.

Once data is transferred, the new sub-servicer begins the task of data validation, reconciliation, and integrating the portfolio into its operations. This may involve setting up new accounts, adjusting workflows, and ensuring that all relevant personnel are briefed and trained on the nuances of the newly acquired portfolio.

Quality Checks and Monitoring

After the transition, the work of monitoring the new process begins. Are the payment systems working correctly? Are payment patterns changing? Are there spikes in delinquency? Have in-flight loss mitigation loans accurately transferred? Is escrow being handled properly? Are customer inquiries being addressed? Are there any data mismatches or errors? Continuous monitoring and quality checks ensure that issues are quickly identified and corrected. The lender should establish a feedback loop with the new sub-servicer so that challenges faced by the customer are known and improvements and process adjustments are made.

Finalizing the Exit with the Previous Sub-Servicer

As the lender says “hello” to a new sub-servicer, there’s the task of formally ending the relationship with the previous provider. This involves settling any financial obligations, ensuring all data has been handed over, and, in some cases, decommissioning old systems or processes.

Changing from one sub-servicer to another is not a task to be taken lightly. It demands meticulous planning, flawless execution, and continuous communication.

While the process can be daunting, with the right partners and a clear strategy, it can lead to improved operational efficiency and service quality for the institution and its customers.

The realm of servicing transfers in the mortgage industry is complex and filled with both opportunities and challenges. The support and guidance you receive can make all the difference in building a stronger and more successful business. STRATMOR, with its deep knowledge and extensive industry expertise, can serve as a trusted advisor in helping you navigate the complex business of servicing transfers.

Through a combination of strategic insights, operational expertise, and a hands-on approach, we ensure that institutions execute these transfers efficiently, compliantly, and in a manner that upholds the trust of all stakeholders.

STRATMOR offers a comprehensive range of services to facilitate, optimize, and address the myriad activities and challenges tied to these transfers. These services include due diligence, operational audits, strategic advisory, data management and more.

To find out more contact us today. Michael Grad

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.