It’s March … again. This week marks one year since I filled out my first-ever 100 percent accurate NCAA Basketball Tournament bracket — I had COVID-19 winning every game. This year I might be returning to having a low number of correct picks, but at least it’ll be significantly more fun to watch. Speaking of which, the last couple minutes of those games are invariably thrilling. That’s because so much can happen. A single bad pass or a clutch shot can spell the difference between victory and defeat. The last days — or even hours — of a mortgage loan process can create that same anxious energy for borrowers.

In the borrower journey, there are many places where the road can diverge from a “happy path” to an “unhappy path.” It might be a confusing online application, the lack of a required documents list, or a poor hand-off from the originator to a processor. However, the part of the process most concentrated with off-ramps to unhappiness is at the very end — the loan closing. In the past year, we’ve seen problems skyrocket around the closing process.

Just like the end of a nail-biter NCAA tournament game, so much can happen in the last hours or days leading up to a loan closing. Suppose the closing itself (the actual appointment) doesn’t start on time or there’s a clerical error on the paperwork – or worse, an unexpected or misunderstood fee. While these miscues may not be enough to completely derail the closing of the loan, they could be enough to flip the borrower from a raving fan to someone who will badmouth you. Regardless of who is at fault, the blame for any miscues at a closing will often be passed along to the lender or originator, particularly when they are not physically or virtually represented.

Consider the extent to which Net Promoter Score (NPS) suffers when one of these three missteps occurs:

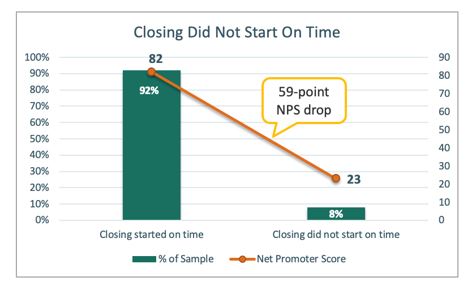

Closing Does Not Start on Time

When a closing fails to start on time, an already anxious borrower may start to feel panic as they imagine worst-case scenarios. It’s like the opposing team taking a time-out with ten seconds left on the clock. Nervousness drains delight and NPS falls 59 points.

Chart 1

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.

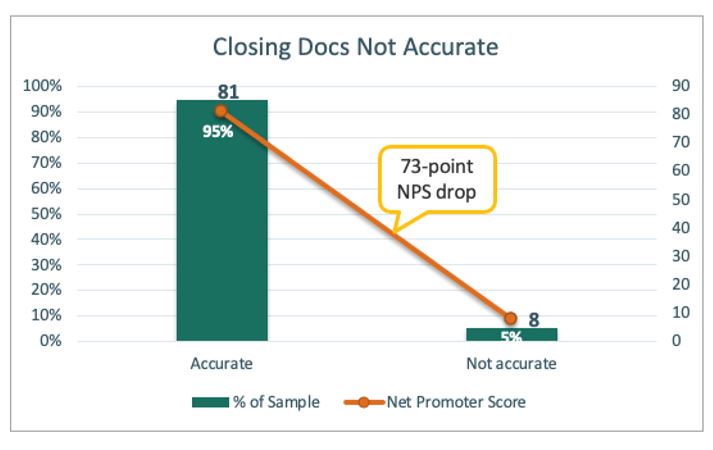

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.Closing Documents Are Not Accurate

When a borrower sees an error on their closing documents, oftentimes a clerical error like a misspelled name or street address, it erodes their confidence that the remainder of the closing package is accurate and NPS falls 73 points.

Chart 2

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.

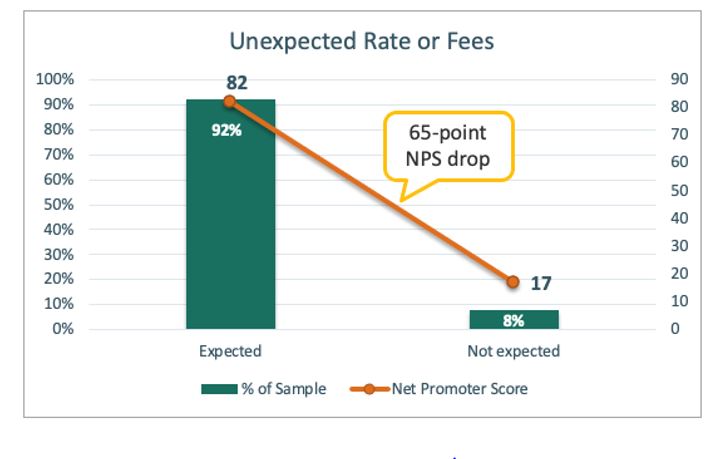

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.There Is an Unexpected Rate or Fee

When a borrower perceives unexpected rates or fees, they may wonder whether someone pulled a fast one on them. Even a hint of suspicion of hidden costs or a changed rate quickly forfeits the chances of a referral. NPS falls 65 points.

Chart 3

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.Here are three ways originators can minimize last-minute miscues and bring home the victory:

Contact STRATMOR Customer Experience Director Mike Seminari at mike.seminari@stratmorgroup.com.

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.