When it comes to residential mortgage lending, is it better to be a bank or a non-bank?

Like many things in life, it’s all a matter of perspective.

There are a variety of factors that may tilt the scales in favor of banks or non-banks. Key factors include the level of interest rates, the trend line for rates, the regulatory environment, capital requirements, and the mortgage servicing rights market, just to name a few. For example, refinance markets used to help banks, especially those with large servicing portfolios. Today, however, non-banks now have more servicing market share than banks, so that advantage has diminished. And, these days, non-banks are much better at retaining customers than banks are. On the other hand, industry consolidation is more likely to be focused on non-banks, via M&A or shutdown scenarios.

In today’s extremely challenging market, banks have an opportunity to regain some market share from non-banks by leveraging their liquidity and capital to offer products that non-banks are simply not able to offer. This article examines the products that create advantages for banks in the current market.

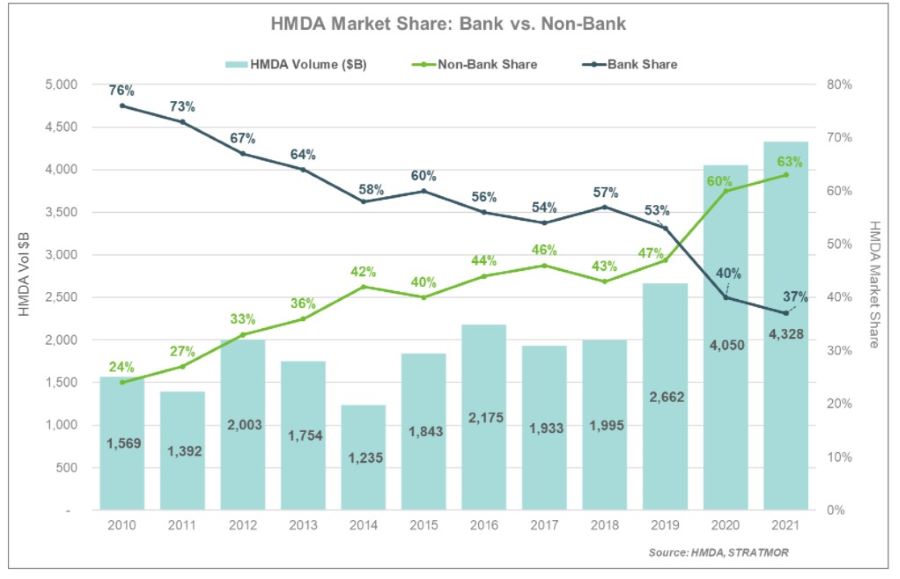

Looking in the rear-view mirror, non-banks have been gaining market share for quite some time now. Bank vs. non-bank market share is summarized in Chart 1:

Chart 1

Based on HMDA data, bank share has dropped from 76% in 2010 to 37% in 2021. In our experience, there are many reasons for the shift in share to non-banks. In general, banks have been slower to hire and fire through market cycles. While there are cultural and employee morale benefits to this, the risk is that banks lose market share as volumes increase because they do not staff quickly enough to handle the volume. When market volume rises, bank cycle times are much longer than non-banks, and this hurts their ability to be competitive, especially on purchase transactions.

Many banks have avoided FHA lending, as the seemingly random enforcement of the False Claims Act creates unquantifiable and therefore unacceptable risk for many financial institutions. This does not help banks when they are competing for their fair share of first-time homebuyer transactions.

Also, banks have all but abandoned the wholesale channel, with notable exceptions, as they are generally not comfortable that they can manage the risks. While that is perfectly understandable, it negatively impacts bank market share as the Wholesale share of the market has been trending up, driven by a handful of large non-bank lenders.

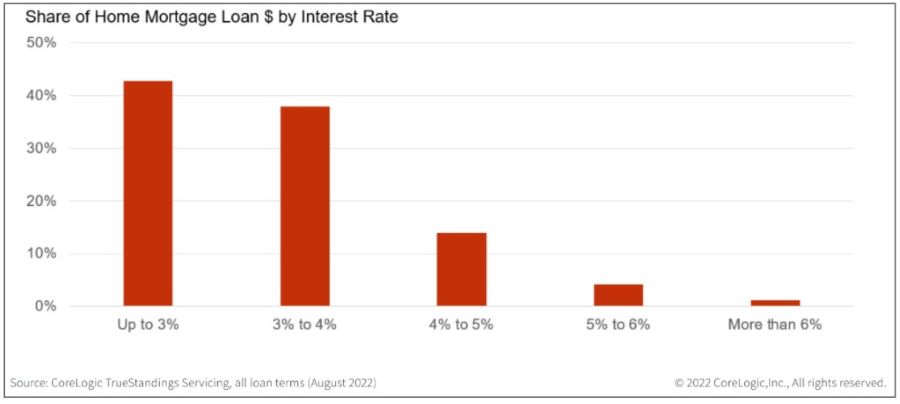

Home Equity Lines of Credit (HELOCs) are popular in today’s market for obvious reasons. After the refinance boom of 2020 and 2021, a large percentage of homeowners have first mortgages at historically low rates. Chart 2 summarizes mortgage debt outstanding by interest rate band.

Chart 2

Based on data from CoreLogic, approximately 80% of borrowers have mortgage rates of less than 4%. Borrowers who need cash are not going to obtain a Cash Out Refinance loan at today’s prevailing rates in the 6.5% range for 30-year fixed-rate loans. Instead, they are opting to keep their low rate first mortgage in place and obtain a HELOC or perhaps a closed end second mortgage with fixed repayment terms.

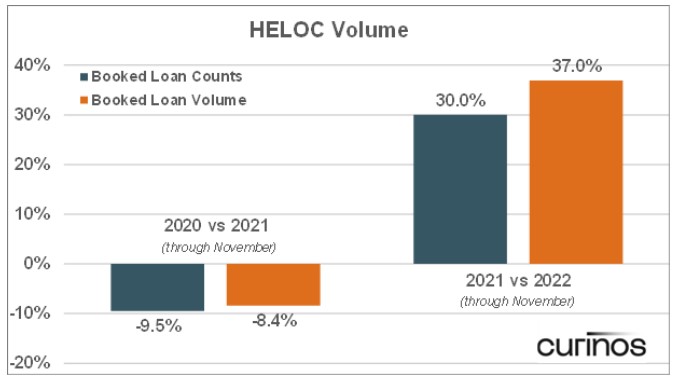

Chart 3 (source: Curinos) summarizes the rapid increase in HELOCs in 2022.

Chart 3

The demand for HELOCs is rapidly increasing and the product certainly makes sense for many borrowers.

So, who is in the best position to offer HELOCs, banks or non-banks? It is tough for non-banks to originate HELOCs profitably, as there are few if any investors who will buy funded product at a reasonable price. Therefore, many non-banks “broker” HELOCs out to financial institutions who then fund and close the loan in their name, which is not a meaningful revenue opportunity for the non-bank lender. Since the revenue potential is low, non-banks are not able to compensate their originators for more than a nominal amount, and thus originators are less inclined to seek out such opportunities. While profitability is not great, there are intangible benefits for non-banks that originate HELOCs. The key benefit is that non-bank originators can stay in front of their customer (another touchpoint), serve as a trusted financial advisor and provide their customers with a product that they truly need.

Banks, on the other hand, have a fighting chance of originating HELOCs profitably, but the key variable is the utilization of the line over the life of the loan. While the fee income generated at closing less the cost of origination (fulfillment and sales cost) may not result in a profitable transaction, the net interest spread earned by the bank (i.e., interest income on the loans less the interest expense on the liabilities used to fund the assets) may result in a profitable product over the long term.

HELOCs are hot right now and banks have a real advantage over non-banks. They have the liquidity to fund the loans and generate profits if utilization is sufficient.

As lenders look to replace lost volume in 2023, they may consider originating or increasing their origination of non-QM loans. Before we consider whether banks or non-banks have the advantage in this product segment, let’s define what we mean by non-QM. In short, a non-QM loan is a loan that does not meet agency documentation and credit requirements as outlined by the Consumer Financial Protection Bureau (CFPB). Common characteristics may include but are not limited to the following:

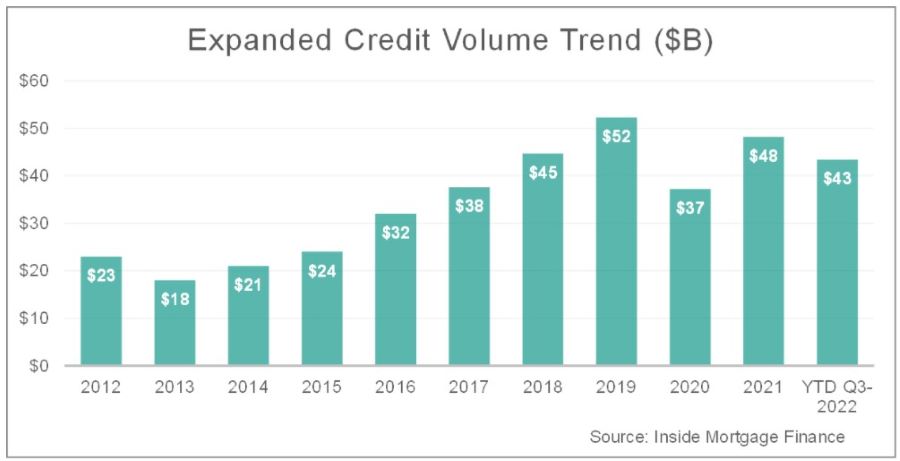

How big is the market for non-QM loans? To get the conversation started, Chart 4 summarizes Expanded Credit Volume trends from Inside Mortgage Finance (IMF).

Chart 4

IMF’s definition of Expanded Credit includes subprime, Alt A, Non-QM loans and other non-agency products not sold to Fannie Mae or Freddie Mac or insured by FHA, VA or USDA. Based on this definition, Expanded Credit volume has been roughly in the range of $30 to $50 billion since 2016. This would equate to about 1.5% to 2.5% of total industry volume based on a $2 trillion year, and less than 1.25% of volume in 2020 and 2021 when volumes were $4 trillion plus.

While we don’t know IMF’s methodology to estimate Expanded Credit volumes, it would appear to be very difficult to estimate non-QM loans originated by banks and credit unions such as interest-only ARMs, loans to foreign nationals, doctor loans, etc. Therefore, it is possible that the estimated volumes above are understated. But even if actual industry volumes are as much as twice what is reported by IMF, the non-QM segment would still only represent 3-5% of the total market.

Volatility and illiquidity are the key factors driving the non-QM market today. Non-banks are having trouble finding investors who would be willing to purchase the product at a reasonable price. Investor demand for private label securities backed by non-QM loans has been greatly reduced due to market volatility and uncertainty about the future direction of rates and the economy in general. So, unless they are backed by a deep-pocketed private equity investor with an appetite for the loans and an ability to manage risk, non-banks are at a real disadvantage. Non-banks have been burned by fickle investors who quickly exited the market (e.g., during the outset of the pandemic) and others who abruptly shut down, such as Sprout and FGMC.

Banks, on the other hand, are not held hostage by the whims of the secondary market. They can decide to originate loans that meet their credit risk parameters and fulfill the needs of bank customers or borrowers in their footprint. This may include Interest-Only loans, doctor/professional loans with higher DTI ratios and loans to foreign nationals. Banks do not typically purchase these loans from correspondent counterparties, thus very few outlets are available for non-banks.

While not a big percentage of the overall market, there is clearly consumer demand for non-QM loans as the gig economy increases the pool of prospective borrowers who have income that is harder to support using traditional methods. The question is, are banks or non-banks best positioned to meet the demand in today’s market? Because of the volatility and illiquidity in the secondary market, banks have a clear advantage.

For the purposes of this article, we are focused on one-time close construction-permanent (CP) loans. In good times, CP loans can provide a steady flow of purchase business on new home construction. In today’s market, with refinance transactions all but gone, lenders that focus on construction lending may have a real advantage.

Are banks or non-banks best positioned to compete in the CP space? Construction lending has long been the domain of banks because of their ability to fund draws during the construction period. A non-bank lender must secure financing from a third-party financial institution to fund draws which puts them at a disadvantage from a cost of funds perspective. In addition, non-bank lenders have less flexibility if problems occur. For example, during the pandemic, construction build times were elongated due to supply chain issues. The warehouse banks financing the construction draws made margin calls or reduced advances in some cases, putting severe liquidity pressures on their non-bank customers.

In addition to liquidity advantages, construction lending is a more natural fit for banks in other ways. Banks are more likely to have the systems and controls in place for draw administration, builder approvals and risk management. It is also a challenge to hedge the interest rate risk during the construction period, and banks are better able to absorb the loss if the hedge does not work as intended.

Recently, construction lending volumes have been down, as new home sales have declined due to higher interest rates, recent declines in home values and decreased consumer confidence. Consistent with purchase transactions in general, prospective homebuyers are in a “wait and see” mode and are not pulling the trigger on their home purchase. Foot traffic in model home centers has dropped precipitously which is not an encouraging sign.

Even though the construction lending market is a “shrinking pie” now, it is still the natural domain of banks, and in today’s market, they should be able to gain share versus non-banks.

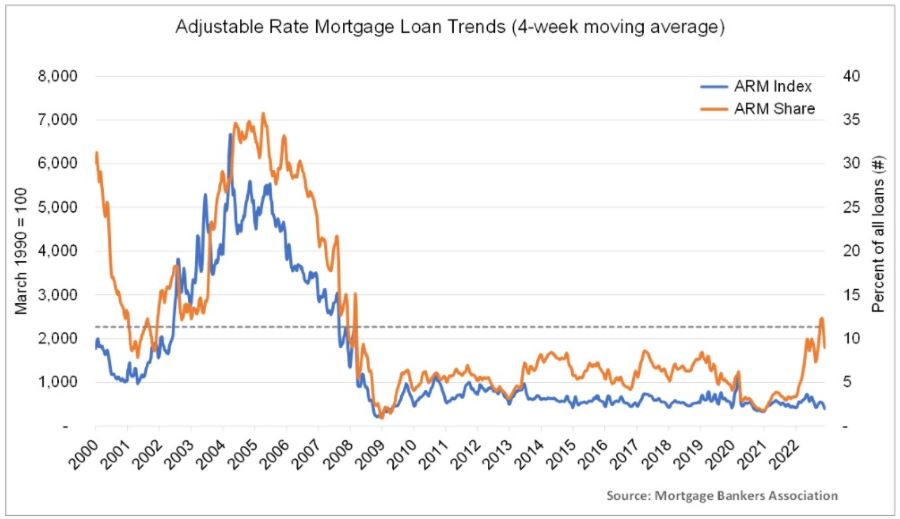

With the increase in 30-year fixed mortgage rates, adjustable-rate mortgages (ARMs) are on the rise. Chart 5 summarizes ARM share going back to 2000 based on data from the Mortgage Bankers Association.

Chart 5

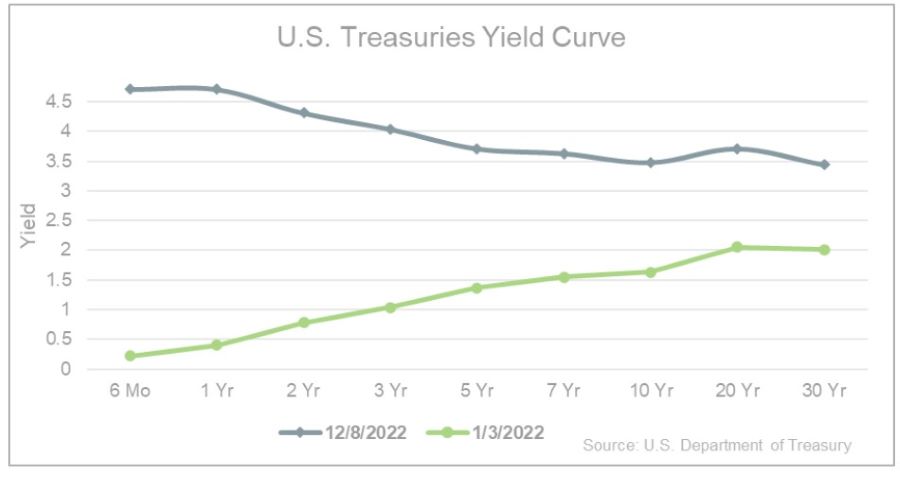

While the level of 30-year fixed-rate mortgages is a factor, the bigger driver is the shape of the yield curve. The yield curve represents the rates at different maturities for a given fixed income security. Normally, shorter term securities have lower rates than longer term securities given the market uncertainties over longer periods of time including inflation expectations. Chart 6 summarizes the yield curve for Treasury securities as of January 3, 2022, and December 8, 2022.

Chart 6

Note that the yield curve has moved from a gentle upward slope as of the beginning of 2022 to a downward (inverted) slope as of December 8. Shorter term rates drive the rates for ARM products, and 30-year fixed rates generally move in the same direction as the 10-year Treasury, with a credit spread which has historically been approximately 175 basis points. The spread is much higher now. We are not economists at STRATMOR and rely on mortgage industry economists like Mike Fratantoni at the MBA for guidance on the future shape of the yield curve. But as the yield curve returns to more of its historical norm for “steepness” we can expect an increase in ARM volumes.

Who has the advantage when it comes to ARM production? Banks are the clear winners in this arena because they can originate ARMs and hold them for investment. Non-banks must originate for sale to investors, and the number of ARM investors can vary from market to market. Right now, there are fewer outlets for ARM loans than most non-banks would like. Also, the prices paid for ARMs are less attractive than for fixed-rate products.

This one is straightforward — advantage to banks. While the inverted yield curve is limiting the current demand for ARMs, when the curve normalizes, it will translate into an even greater advantage for banks.

The Federal Housing Finance Agency (FHFA), the regulator that oversees Fannie Mae and Freddie Mac, sets the pricing policies for the agencies. Like any rational buyer and guarantor of assets, FHFA raises prices and adds overlays on asset classes for which they have diminished appetite. In general, FHFA wants fewer assets in non-core categories such as:

As a result, agency purchases of non-core loans have declined. For example, roughly 73% of the dollar volume of loans included in GSE MBS issued during 3Q22 were core products — the highest level since 2014. What do all these loan categories have in common? Banks can readily originate them to the extent that they have balance sheet capacity, and the product fits their risk parameters and yield requirements. Also, banks may desire to originate some of these products for customer relationship reasons. Importantly, banks are less likely to acquire these loans from non-bank correspondent counterparties.

When it comes to these non-core agency products, non-banks are in a pickle. They can’t sell these loans to the agencies at prices that correspond with competitive rates for consumers, and they struggle to sell loans in these categories because fewer aggregators will buy them.

We are in a historically bad market downturn. (See “What’s Different About this Downturn?” from our November Insights Report). In times like these, it is normal for lenders to look to additional product categories to find ways to increase loan production volume. When thinking about the different product choices out there, whether it is HELOCs, non-QM, Construction, ARMs or non-core non-agency loans, banks have real advantages over non-banks.

Does this mean that banks will suddenly overtake non-banks in market share? Not likely. But by leveraging their natural advantages in certain product segments, banks may be able to regain at least a modicum of lost market share from non-banks in the near term. Cameron

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.