There’s a café down the street from my home that is a local favorite — and for good reason. The cheery red awnings and bright flowers welcome you inside, just before the friendly staff greet you with a smile. The food is consistently delicious, served promptly, and for a fair price. The owners even have a small section of art and gifts for purchase and they have water bowls for your canine companions on the comfortable patio. Every time I leave, I find myself thinking of who I might ask to join me on my next visit.

I recently visited another café and had a vastly different experience. After waiting for the three hosts to finish their personal conversation and see fit to acknowledge us, we were seated at a small table and told to scan the QR code for the menu. No problem, until the QR code didn’t work for any of us. Menus finally arrived, meals were ordered, but when the food arrived, one of the meals was missing. When it finally arrived sometime later, it wasn’t even the right meal. I left wanting to vent my frustration to anyone who would listen.

Talk about two very different customer experiences! Now consider the simplicity of a restaurant experience, where success is marked by friendly, prompt service and tasty food provided at a fair price in the span of one or two hours, compared with securing a mortgage loan. A mortgage loan is the largest financial transaction of most people’s lives, with a high degree of complexity, multiple players involved, not to mention the disruptive and emotional life change of moving into a new home and neighborhood. The stakes are high and it’s a tricky process to get just right.

Search the phrase “mortgage customer experience” online and more than 178 million results pop up. No wonder “the customer experience” is seen as the critical differentiator, even though it is often missed or misunderstood. Defining, understanding, and improving the customer experience is the hot topic du jour for lenders, particularly as the signs of rising interest rates foreshadow the dawn of a renewed focus on purchase transactions. It’s time for lenders to unlearn the reactive muscle memory of the refinance market and prepare for the purchase driven climate ahead.

The good news is this: You are a customer experience expert already.

That’s right. We are all customers of many various businesses and services, including everything from cafés to financial services, and we surely know what a great customer experience is…and what it is not. The key is to change your vantage point and honestly look at your own customer experience from the outside in, rather than from the inside out as we normally and naturally do. In this article, we’ll unpack the importance of the customer experience, how to intentionally create, measure and track it, and the immediate steps lenders can take to level up their approach organization wide.

Customer Experience (CX) in many ways is quite simple. Much like any relationship, positive first impressions followed by good experiences form the foundation, and each interaction thereafter either builds or erodes satisfaction, trust, and propensity to repeat or refer business. “It’s about good communication, setting clear expectations, living up to them – and ideally, adding in a dash of delight,” says Mike Seminari, CX expert and director of STRATMOR’s customer experience program. “In an increasingly competitive mortgage market, which is rapidly moving toward a purchase environment, it’s critical.”

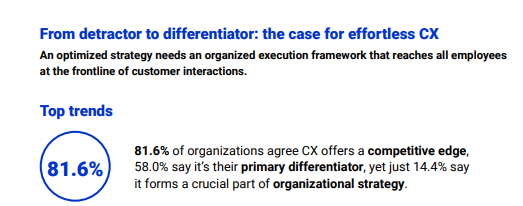

Interestingly, while 82% of organizations agree that CX offers a competitive edge and 58% say it’s their primary differentiator, only 14% are intentionally applying ongoing focus to CX as a crucial part of organizational strategy.

Source: NTT Ltd 2020 Global Customer Experience Benchmarking Report Executive Guide.

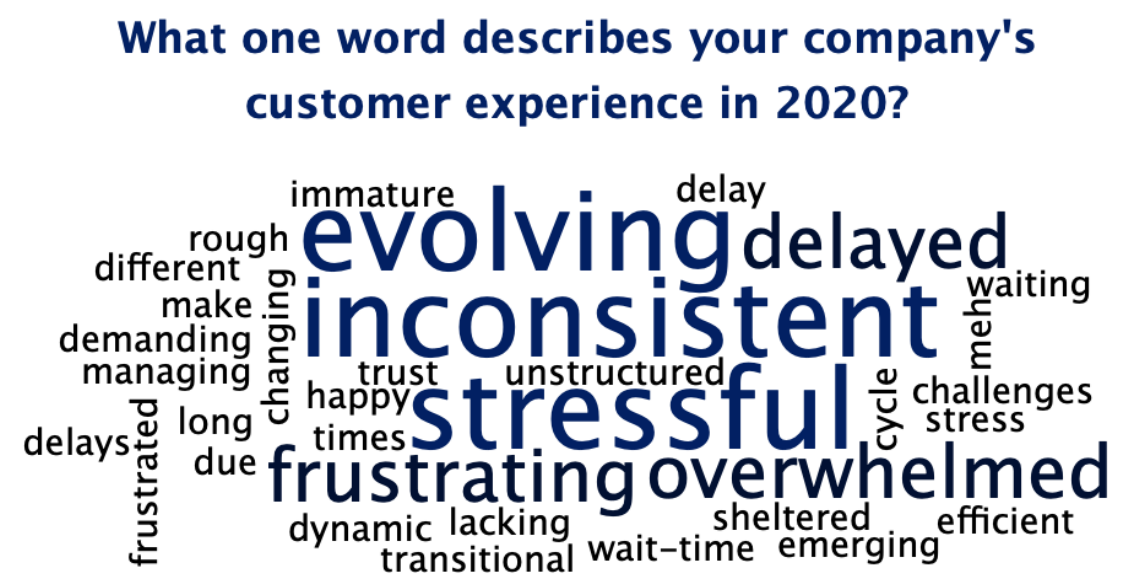

Source: NTT Ltd 2020 Global Customer Experience Benchmarking Report Executive Guide.While many lenders have adopted various digital technologies to help create an easier and more seamless digital process, there remain many gaps to be solved in the overall customer experience. A recent STRATMOR workshop uncovered that even incredibly successful lenders are using these words to describe their customer experience. Sound familiar?

© Copyright STRATMOR Group, 2021.

© Copyright STRATMOR Group, 2021.Technology is a part of the CX story, but digital technology is simply a tool in your arsenal. Technology on its own cannot create an optimal experience for your customers or employees. Your tech stack is there to help ensure the execution of your well-designed CX strategy.

“Your operating model must begin with a top-down, customer-centric strategy to drive everything else — including development of your business and IT roadmap, internal and external processes, and the required staffing and core capabilities required for execution,” says Lisa Springer, STRATMOR Group Senior Partner and CEO. “Your overarching strategy must be created by listening to the voice of your customer and utilizing data and metrics to know where you stand. Then, your execution and tactics must be consistently monitored, measured, and adjusted to ensure they are moving you toward your strategic goals, regardless of market conditions.”

In 1997 Steve Jobs said, “You have to begin with the customer experience in mind and work backwards.” Similarly, your CX strategy must begin with the end in mind — what goals are you looking to accomplish, what does success look like, and how will you know when you get there?

One of the best first steps you can take is to start tracking your customer satisfaction scores regularly on a company level, which will give you a solid baseline from which you can benchmark and set challenging yet reachable goals. There are many different methods by which you can gauge satisfaction, including CSAT (Customer Satisfaction) with a simple 1 – 5 ranking, the Net Promotor Score (NPS), or industry-specific surveys like the Mortgage Satisfaction Survey (MortgageSAT) provided by STRATMOR and CFI Group, which includes deep-dive analysis into which areas of the loan process have the greatest impact on repeat and referral business.

Recent CX trends, according to Mike Seminari, include higher satisfaction levels reported by refinance versus purchase borrowers, likely due to the very different customer personas on these two types of transactions. Another interesting trend was that retail continued to outperform the Consumer Direct channel, despite being forced to abandon face-to-face interactions during the pandemic. They quickly moved to video conversations, which helped them continue to deliver a personal touch,” says Seminari. “And perhaps a surprise, compared to 2018 and 2019, NPS was consistently better throughout 2020 thanks to the low rates, as extra money in the pocket apparently goes a long way towards helping borrowers feel satisfied with their transaction.”

Additional metrics that can be utilized for benchmarking include lead to application rates, application pull-through, retention of past customers, and referrals by source including past customers. While these metrics must always be adjusted against market conditions, knowing your metrics, and watching them on a regular basis will indicate where your efforts are paying dividends, and where more work may be needed.

Pay attention not only to what is being said but also to what is NOT being said — who is not responding to your surveys, and why — or why not? Track your response rates and follow best practices to improve them over time.

Seminari also notes that although less than half of lenders report achieving even 30 — 40% response rates, you should be striving for response rates over 50%. He says you can and should be able to achieve that by paying close attention to deliverability (short subject lines, short copy, limited use of graphics, avoiding acronyms are a few tips) as well as driving awareness through increased advance communication to customers about the survey, and even considering incentivizing responses. The more you know…!

Also, don’t forget to survey your team members and employees about the customer’s experience and their own experiences as an employee, which are generally directly related. It’s uncommon to have an exceptional customer experience and a miserably unhappy staff with a great deal of turnover, and vice versa. While internal surveys should be anonymous, it is often helpful to have them partitioned by department or role so that you can more easily see where problems may need your attention.

Metrics for employee satisfaction are not dissimilar from customer metrics and should include employee NPS (eNPS) that asks how likely they would be to recommend your company to a prospective employee, as well as overall churn or turnover rates. Creating a culture of satisfaction for both customers and employees are two sides of the same coin, and goal setting must closely follow your strategic decisions surrounding CX.

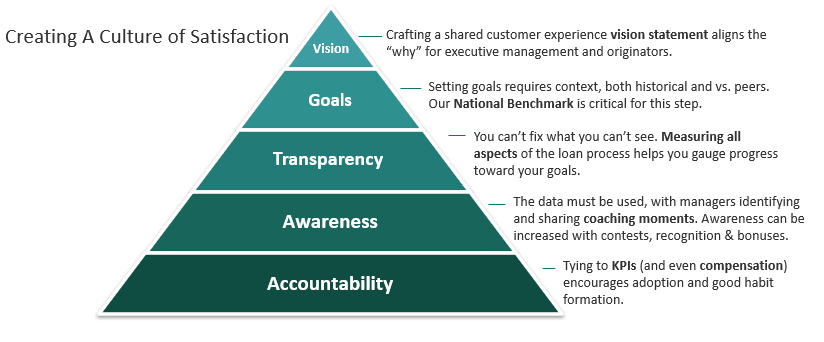

The following Target Operating Model illustrates the Customer Experience corporate strategy.

© Copyright STRATMOR Group, 2021.

© Copyright STRATMOR Group, 2021.Developing an understanding of the key personas (profiles of customers’ key traits, behaviors, motives, etc.) served is a must, but start at a high level. You can deepen and richen your personas and resulting experience maps over time, considering generational or regional demographics, preferred channels of communication, first time homebuyer vs experienced buyer and much more.

The purchase lead persona is certainly much different than the refinance persona, due to the different nature of the transaction and time sensitivity vs. rate sensitivity. While this is broadly known, there is a big difference between something you know at a cognitive level and how you default to behaving in real life, especially when you are busy. (Ask anyone who has tried to overcome a bad habit on this one.) Why is this important?

As we turn the corner from a refinance-centric market back to a purchase-focused one, we must be aware that despite our very best efforts, there is a lot of “muscle memory” at play from working with refinance customers. Purchase customers are different. And as noted by Seminari earlier, we did not do a great job of this during 2020, with purchase customer satisfaction falling far short of refinance customer satisfaction.

The purchase-focused, consumer centric journey has already been mapped out. Lisa Springer shared it in the May 2021 Insights Report. The technology exists to make this journey a positive one for the borrower.

This is where technology can help with execution, as strategy applied to the right tools will help support the right process with originators and operations staff. The lender that does not deploy it effectively will pay a heavy price.

Lenders, if you are in the early stages of mapping out your CX strategy, STRATMOR recommends starting with a few very simple personas, such as purchase lead / customer, buyer’s agent, listing agent, refinance lead / customer, past customer in database.

As with any change, the first step is to be realistic and transparent about the baseline. This can be accomplished by experience mapping exercises, surveys, and secret shopping (described below).

Experience mapping requires a cross functional internal team willing to be transparent and call out areas where the emperor may be unclothed. Create a “SWAT” team that includes team members from operations, production, marketing, and technology. Have the team:

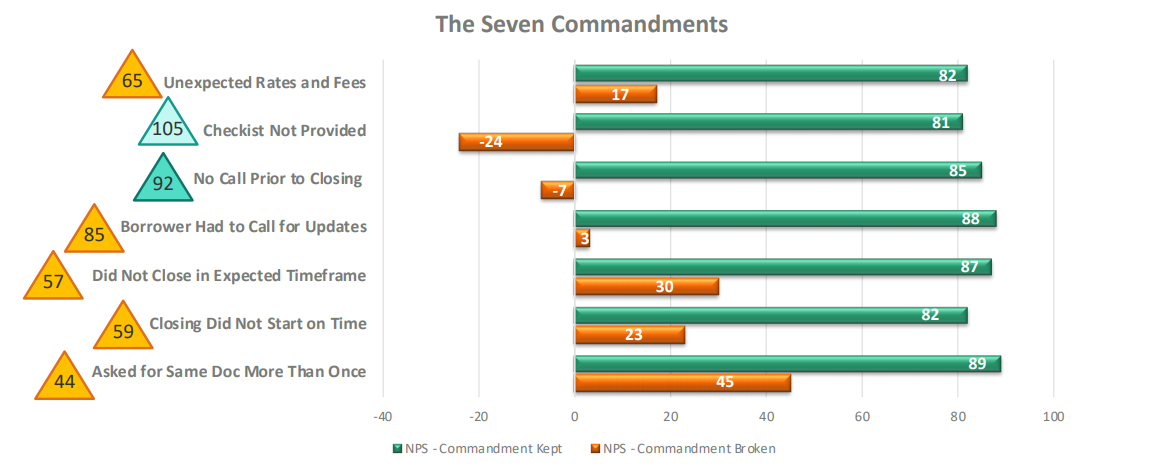

Surveys provide another incredible source of information to layer onto an experience map, and when asked, customers will generally tell you exactly where their areas of frustration can be found. At STRATMOR, we have pinpointed seven tactics — which we refer to as the Seven Satisfaction Commandments — that provide the greatest positive impact on a borrower’s likelihood to recommend you to friends and colleagues (as measured by Net Promoter Score); and, perhaps more importantly, these tactics can significantly reduce the number of highly dissatisfied borrowers who may poison a lender’s reputation via negative posts to social media and by “poor-mouthing” the lender to family and friends.

These commandments are based upon the seven most influential aspects of the loan process that can make or break a borrower’s likelihood to refer business your way. Most of the commandments can be addressed proactively by loan originators; a few require management response for damage mitigation. Note the large swings in NPS, with the green bar showing a commandment followed and orange showing a commandment broken.

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group.

Source: © MortgageSAT Borrower Satisfaction Program, 2021. MortgageSAT® is a service of STRATMOR Group and CFI Group. STRATMOR data shows that at least one of these commandments are broken on approximately 60% of loans. The impact on a lender’s bottom line can be devastating: according to data from the calculator found on the MortgageSAT webpage, the top line revenue impact to a company doing 25,000 loans per year could be as much as $9 million.

Finally, secret shopping can be another powerful source of information, as it allows a lender to evaluate CX in living color and in real time. While going through an entire mortgage process is not something easily secret shopped, many aspects of the customer experience can and should be. What happens when an online inquiry is placed? When the 800 number is called? When an application is abandoned? When an email is sent to that address in fine print at the bottom of your website? How long does it take to complete an action at each touchpoint, and is the message on point? What happens after that?

In 2019, I conducted an “Experience Experiment” where I asked four friends to inquire about a mortgage with three different lenders — one bank, one independent lender, and one lender primarily operating online. The instructions were to contact the lender through whatever channel they felt most comfortable, online, phone, email, etc. The results were nothing short of stunning, with ten of the twelve outreaches not receiving a reply within 24 hours, and five of the twelve outreaches never receiving a reply at all.

I won’t name names, but do you feel confident this could never happen in your business? Only one way to find out.

You already have a customer experience, that’s a fact. But whether you intentionally created an outstanding experience and are consistently working to up-level it is another question. Does your process have gaps? Is it consistent? Measurable? Does your team understand, embrace, and embody the strategy? Is your CX living up to the standards of excellence you want and expect for your customers?

If you aren’t satisfied with your answers, take action. Everything you need is at your fingertips to close the gaps and upgrade your customer experience. Start by focusing on Mike Seminari’s “Four Pillars of Operationalizing CX” below:

With the market shifting quickly from refinance to purchase, and competition set to become even more fierce by Q4, now is the time to focus on creating or strengthening your customer and employee experience. If you haven’t started yet, there’s no time like the present. As the Chinese proverb says, “The best time to plant a tree was twenty years ago. The second-best time is now.” If you need assistance with any part of your CX plan, STRATMOR has Best-in-Class CX experts who can help you put your borrowers on the happy path of the mortgage experience. Sue Woodard

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.