Back when I was a working loan officer (LO), some 30 years ago or more now, we had a saying: you get what you pay for.

This was usually the punchline for a cautionary tale about how someone got a great deal on something that turned out to be not so great. You paid a little and you got a little, or less.

The lesson is that if you want more, you’re going to have to pay more. But there is a limit to this kind of wisdom, and the mortgage industry is bumping up against that now.

The Mortgage Bankers Association (MBA) brought this into focus for many with its Quarterly Mortgage Banking Performance Report. The association reported that independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks experienced a net loss of $1,972 on each loan they originated in the first quarter of 2023, after having a reported loss of $2,812 per loan in the fourth quarter of 2022.

Lenders still have too much overhead to spread across far fewer loans, and even a “scorched earth” reduction in management and support positions doesn’t seem to be enough to turn the profitability tide.

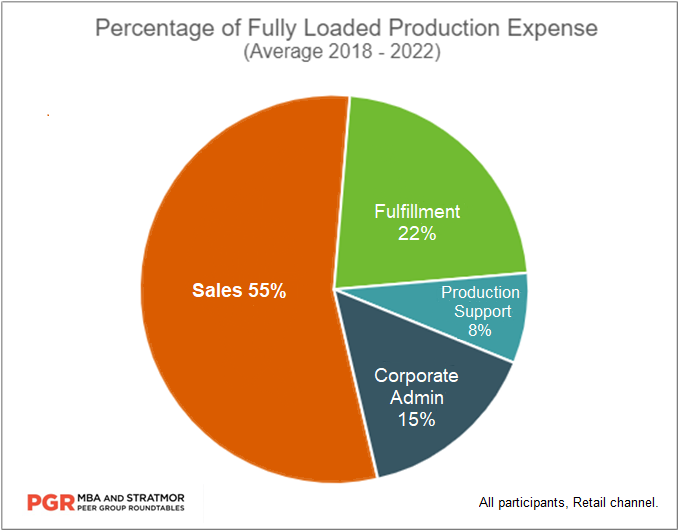

Based on data from the PGR: MBA and STRATMOR Peer Group Roundtables program, the average fully loaded cost to originate a loan through the Retail channel for all peer groups was $13,131 in 2022. Of course, we had some good years before that, and over the last five years (2018-2022) the average cost was $9,900.

So, where does the money go? Here is a percentage breakdown of cost by category from 2018-2022:

Chart 1

This drives the point home — sales represents more than half of the cost to originate. The conclusion is clear: origination costs are at an all-time high and sales costs are the biggest component by far.

Lately I’ve been leading discussions on the sales compensation topic at industry conferences and in lender meetings around the country. Invariably, the first thing I hear when the high cost to originate comes up is a promise to cut costs … in the back office.

As shown in Chart 1 above, loan fulfillment — processing, underwriting, closing and other direct costs to manufacture the loan — costs the average lender about 22% of their cost to originate, which is usually in the range of $2,000 to $2,500 per loan.

While mortgage bankers tend to look closely at fulfillment for cost savings, the opportunity is limited. Let’s say a lender somehow manages to cut fulfillment costs by 20%, which would be an excellent outcome. Yet this would equate to cost savings of $500 (based on $2,500 fulfillment cost) or only 5% assuming a total cost to originate of $10,000. Nonetheless, this is where the industry has traditionally gone to cut costs. Meanwhile, to reiterate, 55% of their expenses are on the sales side.

As Congress was considering the sweeping changes that would impact our industry under the banner of the Dodd-Frank Wall Street Reform and Consumer Protection Act, the industry got wind that the Act would make it illegal for the industry to base compensation on any term of the loan. The purpose of the rule was to correct past abuses that based the pay on how much the borrower paid — meaning if you charged more as an LO, you got paid more. But the original versions of this rule made payment based on ANY term of the loan not allowable. And any term included the loan amount.

This was considered an existential threat to the industry’s survival and caused consternation amongst industry executives. The primary concern was that the entire industry would have to change its compensation structures, including potentially paying commissions based on unit volumes.

In hindsight, paying by the unit would not have been the worst possible outcome. Ultimately, regulators capitulated and gave the industry a single loan term they could base their compensation plans on: the loan amount.

After the comp rule changes, most lenders migrated from revenue splits or profit based pay to commissions based on a percentage of the loan amount, or to a lesser extent, based on loan units. But here is the issue. Real estate inflation has far outpaced general and labor cost inflation, thus driving up sales compensation which was mostly based on loan amount. Chart 2 below illustrates the point.

Chart 2

If the industry was not able to compensate loan officers based on the loan balance, LO income would have likely been based on unit production. So, in 2010, the average LO commission was $1,672 per loan for retail lenders across all groups. Currently, it’s almost doubled to $3,194 per loan.

However, if we had agreed to pay the LO the $1,672 and then indexed that rate to inflation, the LOs would be receiving $2,048 per loan in 2022. Instead, we pay $1,146 more per loan (more than 50%).

Have salespeople gotten a “free ride” on dollars of commission simply due to the rapid rise in real estate values? If the common industry practice had changed to paying salespeople based on loan units, would costs be more manageable?

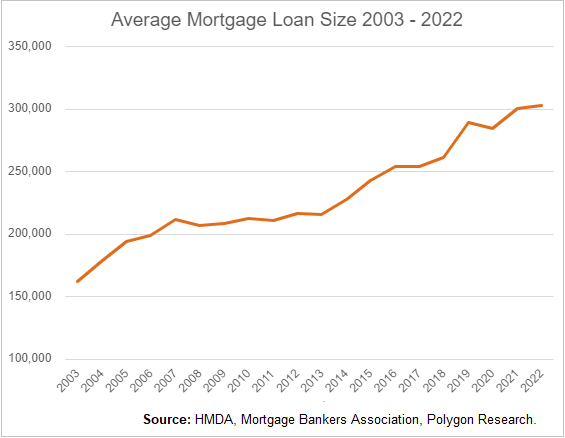

To answer this question, we need to dig a little deeper. With the rapid rise in real estate values, not surprisingly, average loan amounts have increased significantly as shown in Chart 3 below.

Chart 3

Loan balances have almost doubled since 2003, increasing from approximately $160,000 to over $300,000 in 2022. It is important to understand that most revenues are tied to the loan amount. Therefore, the increase in average loan sizes has driven an increase in both revenue and sales expenses. Of course, fully loaded costs and profits vary greatly across interest rate cycles.

While sales costs have gone up, they have stayed relatively consistent as a percentage of total origination costs.

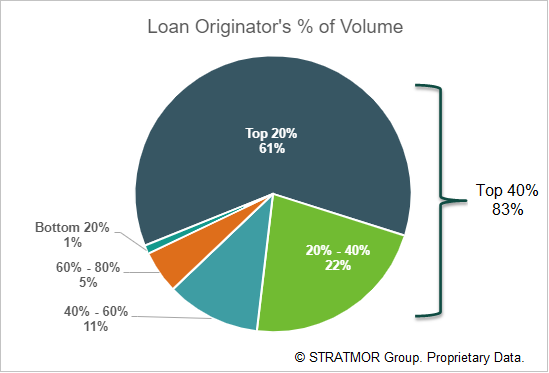

One mortgage banking truism is that there is a high demand and relatively low supply of high producing loan originators, especially with a purchase transaction focus. This is borne out year after year with data that shows the top 40% of loan officers originate roughly 80% of the volume, not to mention the ongoing intense recruiting efforts for the top people.

It is also true that retail mortgage loan officers often act and think like free agents. This is supported by annual turnover rates typically in the 30-45% range. While it is true that most turnover occurs in the bottom two quintiles, there is also a lot of recruiting effort and cost focused on the high producers as well.

Further, it is true that revenue has generally increased since 2003 for a variety of reasons, including:

As revenue has grown, many lenders have made the business decision to increase their investment in salespeople. Remember, high producing loan officers are in low supply and high demand and are often independent minded. Therefore, many lenders have invested some of the revenue gained from higher loan balances and increased margins into recruiting and retaining top salespeople.

It is clear that retail sales costs have grown and continues to be the largest component of the cost to produce. While we see some evidence that sales costs are dropping as revenues drop and margins have compressed, it is highly unlikely that the percentage of sales cost to total origination costs will change materially. Sales cost will continue to be the biggest component.

Given that sales cost will continue to be the largest component of retail origination costs, what can be done to manage this beast? How do we make the most out of our spend, to actually “get what we pay for?”

A sound compensation strategy always starts with a thorough understanding and alignment of a lender’s culture and objectives. Examples of different lender cultures and models include:

Once there is a complete understanding of culture and model, executives should consider the common structures and elements that can be used. According to STRATMOR’s Compensation Connection® Study, the most common compensation structures in place today is to pay basis points (bps) of the loan amount rather than a flat dollars per loan.

But is this really aligned with the company’s goals, and are there some other structures or elements to consider?

For example, what if you wanted to put in place a structure based on unit-based pay, with adjustments on top of that? You could put your compensation floor at a fixed rate, say $3,000 per loan, but then move that number up and down based on certain elements:

If the lender services loans and an LO keeps a borrower from churning out with a new loan or refinance, they get a bonus.

Many of these compensation structures are ignored in plans today because the only thing we focus on is the loan amount. How can we expect our sales professionals to give us what we need to grow stronger businesses if it’s not built into their comp plans?

We preach all the time about the things loan originators have to do right. See Mike Seminari’s excellent Seven Commandments for Optimizing the Customer Experience, for a perfect example. But compensation structures are not usually focused on these key areas.

But isn’t building a compensation plan based on so many factors difficult to create and administer? We create quality-focused compensation plans for our clients all the time, and STRATMOR can help your organization.

If the lender is free to take other factors into consideration, it naturally opens up a discussion of the lender’s overall costs. With profitability in the tank and volume down, this is the perfect time for that analysis.

Many of the lenders’ direct expenses are tied to time spent and the steps in the loan process, which depends a great deal on the team working the loan. When an inexperienced loan officer is on the team, they might take longer, and thus add to overall expenses. Ask the top ops managers — they know the strain of the low producer. And lenders are paying these higher prices for less actual production.

As discussed earlier, we know that 40% of loan originators generate 83% of the volume.

Chart 4

The top loan officers are generally long-term industry professionals. They understand the loan guidelines, sell the right products to borrowers and get approvals and rate locks. Their pull-through is high because they know how to guide the borrower through the process.

The bottom 60% — and this gets more extreme as you work your way to the bottom — may not have studied the loan programs or have the experience to answer the borrower’s questions and they probably won’t stay in the business long enough to get it. They can put enormous pressure on the underwriting and processing folks because every loan matters to them. Each loan is a huge part of their overall monthly compensation. Does it really make sense that the compensation for the groups described above is the same?

Lenders have two ways to deal with this: 1) fire the bottom 60%, or 2) change the compensation model so that lower performing loan officers will get paid less and perhaps push themselves out of the business. This is normally accomplished by using tiered commission structures in which higher producing originators earn higher bps and lower producing originators earn lower bps. This could also be accomplished by tiering unit-based compensation.

Good IMB owners don’t want to lose good people and they want their people to succeed. But in times like these, the owners are the ones watching their margins and profits fall, after they have put their own capital at risk. These are difficult decisions, but lenders can’t ignore their highest cost area when trying to claw their way back to profitability. They either have to somehow reduce sales compensation or find a better way to “get what they are paying for.”

It can be done. We’re already seeing this happen on the real estate sales side of the business. Real estate brokers have read the writing on the wall and reduced agent pay to allow them to continue to spend money on branding and marketing.

As you might imagine, I’ve had many conversations with lenders about sales compensation. It’s directly tied to a source of pain they are feeling right now. They understand the need and many, if not most, of the possible options. But when it comes to taking action, they tell me:

“Yes, I’m willing to make changes, as long as I’m not the first.”

No one wants to lose their top performers because of changes to their compensation plans. Yet I’m not sure that would, happen, especially if the lender took a thoughtful approach to the change and included compensation incentives that motivate your performers to achieve certain metrics. But it takes a great deal of intestinal fortitude to even contemplate it. This is especially true in a highly competitive environment.

But the reasons to make certain changes are compelling. If you’re running a bank, for instance, and your executives are constantly trying to convince regulators that you are all about fair lending when you know your current LO comp plan pays originators based on the size of the loans they originate, you may want to consider a unit-based compensation structure, more aggressive use of floors and caps, or a hybrid of dollar and unit volume tiers.

And, if you’re going to change your compensation plan, there will not be a better time to change than now.

With volumes down by half, the industry is already laying people off to match staffing to demand. On the expense side, every lender is burning their furniture to stay warm. This is already poised to be a less than stellar year. Now is the time to think about the future.

When I talk about changing sales compensation, most lenders think I’m talking about taking pay away from their top performers. That’s not necessarily what I’m saying.

A new comp plan is a new way to pay, but it doesn’t mean you have to start cutting the pay of your top producers — the pay would just be structured differently to complement corporate goals. You also may be paying fewer LOs, because you can keep your best LOs and release the ones that are currently costing you too much.

It’s okay to pay more if you’re not getting less. You just have to make sure that you’re getting what you pay for.

The important takeaway from all of this is to make your changes now and make sure they benefit your institution over the long haul by paying for behaviors you want to see out of your professional sales staff.

We work with lenders every day, helping them craft compensation plans tailored to their actual needs, their real costs and around what drives profitability. Here are two approaches that work well.

Start with the Channel

If you must make a company-wide change, it’s always good to start in an area that will have the smallest impact, or an impact on the smallest group of people. In the case of LO compensation, maybe that place is the Consumer Direct channel.

Many of our newer LO comp engagements are happening here because Consumer Direct is a great place to start. Although very valuable, a Consumer Direct loan officer does not make the same contribution to the enterprise as an originator who can source their own business.

In addition, this department typically analyzes their expenses by cost per unit, and loan sizes tend to be more consistent than in traditional retail. They don’t obsess over basis points, like other lenders do. Instead, they are all about reducing the total marketing cost per unit.

Their business is down so much in this environment that any changes they make would almost go unnoticed but have a huge impact on their business when the market comes back. Also, LOs in this channel are less likely to leave for another job in the business because no one is currently hiring Consumer Direct LOs.

Start with New LOs

A lender could also start by leaving their veteran originators on their existing comp plan and change it for the new rookies that come into the business. As the older generation ages out, they can pass their wisdom along to the younger LOs, who can then carry on under the new comp plan.

As soon as the veterans hear about comp plan changes and begin to search the job listings, let them know that the changes won’t impact them. This is all about bringing in the next generation of loan officers and preparing the institution to succeed in the future.

Once the experienced LOs realize that they can work through to retirement, which is very close for many, without a disruption to their income, they will be more likely to help bring the new LOs up to speed, especially if lenders build that into their comp plans.

If you look at the purpose of our industry — the mortgage banking business — it’s to help FAMILIES get a new home (purchase!) or better manage their monthly mortgage expense (refinance). We talk about how important each of these families are to our business, and we try to ensure our staff is trained to focus on helping families with such a major life choice. Yet, our compensation structures tend to reward high dollar amount loans not associated with getting working families into homes.

Shouldn’t our compensation be more aligned with the actual objective, and not solely the mortgage amount? Introducing at least some elements of unit-based compensation may be a catalyst to change the culture of the company.

In determining what changes might be appropriate, it will be important for lenders to run projections on how any changes might impact overall average profit margins not only today, but in a variety of rate and volume scenarios in the future.

How lenders handle this will vary, and most of them will NOT make major changes to sales compensation such as a switch to a unit-based calculation. To paraphrase John Lennon, maybe I am a dreamer, but I’m not the only one (or am I?).

I do think that lenders who hope to stay in the game over the long term, and to be wildly more successful when the cycle turns and the business comes back, should be working on sales compensation structures now. Many will hire outside consultants who have years of experience in this area and can offer valuable guidance.

Just remember, you get what you pay for. Garth Graham

STRATMOR works with bank-owned, independent and credit union mortgage lenders, and their industry vendors, on strategies to solve complex challenges, streamline operations, improve profitability and accelerate growth. To discuss your mortgage business needs, please Contact Us.

Feel free to reach out with any questions or needs we might be able to help with.